Green Chemistry and Smart Chemistry

The Chemical Industry Drives Innovation in Austria

-

(c) Pressmaster/Shutterstock

(c) Pressmaster/Shutterstock -

Hubert Culik, Association of the Austrian Chemical Industry (FCIO)

Hubert Culik, Association of the Austrian Chemical Industry (FCIO) -

Figure 1

Figure 1 -

Figure 2

Figure 2 -

Figure 3

Figure 3

As Austria’s second largest sector, the chemical industry is also among its most important. Spending on chemical research and innovation also surpasses that of other sectors. At present, it represents around 11% of all investments made in research and development within Austrian industry.

An ad hoc survey of senior managers at member companies of the FCIO (Association of the Austrian Chemical Industry) also showed that companies in the chemical industry drive innovation, promoting Austria as a business location. According to the survey, around 82% of innovations were granted the “highest” and “high” priority levels. Around one in four companies generate over 30% of their turnover from products or solutions that have been on the market for less than five years.

Yet three-quarters of those surveyed also feel that there is a need for political action. For about half of respondents, the factor inhibiting innovation the most was excessive bureaucracy. For 44%, insufficient resources were a hindrance. Many companies also feel that innovation culture in Austria is woefully lacking.

Chemistry 4.0: The Research Priority

Two distinct trends are emerging as research priorities, which we summarise below under the term Chemie 4.0 [Chemistry 4.0]: Green chemistry involves replacing crude oil-based raw materials with what are known as biogenic substances. Examples of these include solvents based on fermentation, or high-quality fibres made from recycled materials. Smart chemistry is about developing smart products and materials. With their special functional properties, they can offer innovative applications with increased benefit – personalised medical care is a classic example, as are the first anti-allergenic surgical gloves, which won an award at the European EARTO Innovation Awards.

A Sector Marked by Strong Exports

Austria’s chemical industry has close international ties: over two-thirds of production is for export, with the majority remaining in the EU.

Numerous companies have foreign subsidiaries worldwide, or are the subsidiaries of multinationals operating as headquarters for Central and Eastern Europe.

The chemical sector in Austria mainly consists of SMEs. This structure and the small number of (research-relevant) corporate head offices are detrimental to research, and must be compensated for in other ways. That is why Austria needs framework conditions and a funding system to gain the edge over larger countries. Thanks to low labour costs and a wealth of raw materials, Asia, the Middle East and Eastern Europe offer a more cost-effective starting position for competing on the global market.

Emerging countries are no longer thought of purely as cheap production sites for the industry, but are now gaining ground as important centres of innovation. Their domestic markets are also growing considerably faster than the European markets.

Investment Incentives are Vital

Investment incentives must be put in place to secure Austria’s future as a viable location for industry. The Austrian system, which indirectly funds research through tax initiatives and directly funds specific projects, is therefore a crucial means of supporting industry research. The chemical industry views direct and indirect research funding as complementary in nature: while indirect research funding is based on location, direct funding is concerned with the specific technology being researched. Austria has a need for both.

Planning Security is Crucial

Planning security is essential if companies are to minimise investment risk. It is affected by restrictions on raw material availability due to chemical legislation, as well as short-sighted climate policy that creates huge uncertainty in Austria as an industry location and stifles investment efforts before they get off the ground. That is why we are campaigning for transparent, comprehensible and far-sighted legislation.

Legislation Threatens Competitiveness

The results of a cumulative cost assessment clearly demonstrated that the chemical industry is suffering under the overwhelming financial impact of chemical legislation. This calls for urgent, policy-based action. It can only be hoped that political decision-makers will consider the results of the study. Given the structure of the circular economy and the upcoming REACH Review, measures need to be taken to minimize the administrative burden companies face due to legislation. Otherwise, the competitiveness and innovative power of European companies in the chemical industry will be jeopardized.

The Austrian Chemical Industry in Figures

Austria’s chemical industry generates a total of EUR 14.8 billion in production value (2016). The plastics processing industry, which in Austria is also monitored by the FCIO, contributes over one-third of this figure (36.6% in 2016). Some distance behind is the pharmaceutical sector, contributing 14.5%, and plastics production at 13.2%. Chemical production also contributes a double-digit percentage to the chemical industry’s overall turnover. Synthetic fibers come in at fifth place (6.1%) (tab. 1).

Around 44,500 people work in Austria’s 247 chemical industry companies. This figure has increased by 0.3% on the previous year. The sector is shaped by SMEs that have an average of 150 employees. Almost one in three employees in the chemical industry works for an SME. Of the 247 companies, only about 50 organizations employ more than 250 people.

Economic Situation: The Beginnings of an Upturn

For the previous five years, there had been no real movement in turnover in Austria’s chemical industry. However, as of this year there has been a noticeable upturn and the sector is looking to the future with confidence. In the first half-year, turnover increased by 2.5% to EUR 7.7 billion. Synthetic fibers performed particularly well, with growth of 10.4%, as did pharmaceuticals (up 5.9%) and rubber products (up 5.6%). Other sectors also showed slight signs of improvement. Only organic and inorganic chemicals, agrochemicals and plastic raw materials continued to lag behind relative to the previous year’s results.

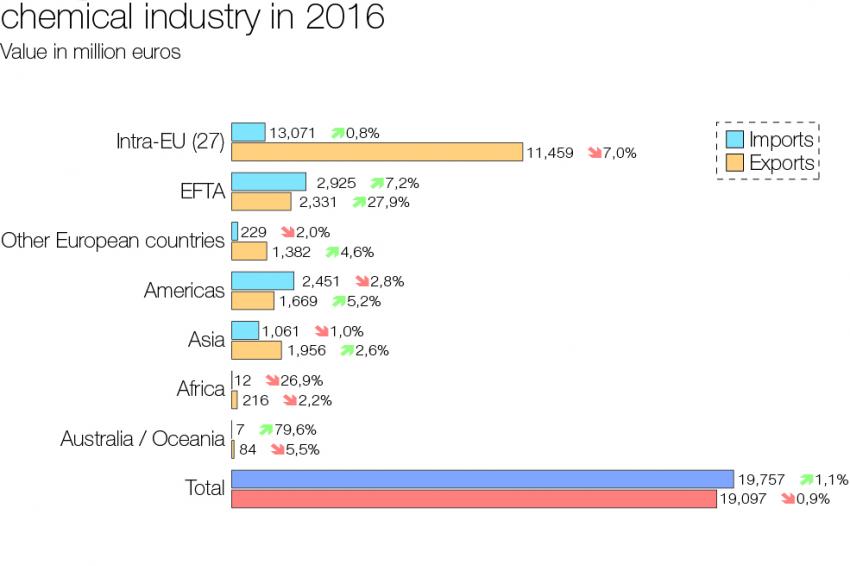

The balance of trade in the Austrian chemical industry was very even in 2016, with only marginally more imports than exports. Around two-thirds of exports remain within the EU (tab. 2). Globally, Germany is Austria’s most significant trade partner, receiving 21% of total export volume. In second place is Switzerland, with the USA, France and Italy some way behind.