Consumer Healthcare

Pharmaceutical and Consumer Goods Companies are Mobilizing for Action in the Consumer Healthcare Market

-

Pharmaceutical and Consumer Goods Companies are Mobilizing for Action in the Consumer Healthcare Market. © fotoknips - Fotolia.com

Pharmaceutical and Consumer Goods Companies are Mobilizing for Action in the Consumer Healthcare Market. © fotoknips - Fotolia.com -

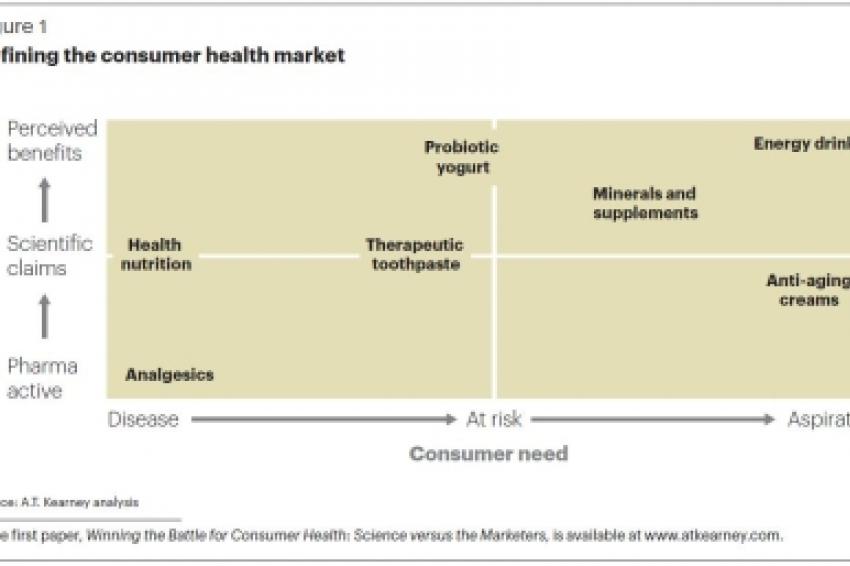

Defining Consumer Health The consumer health market covers a wide range of categories and products, all of which claim to improve some aspect of health or wellbeing and are not generally reimbursed by healthcare systems. Product characteristics vary widely, with the two most essential dimensions being the consumer needs they address and the strength of the claims they make (Fig. 1). Source: A.T. Kearney analysis

Defining Consumer Health The consumer health market covers a wide range of categories and products, all of which claim to improve some aspect of health or wellbeing and are not generally reimbursed by healthcare systems. Product characteristics vary widely, with the two most essential dimensions being the consumer needs they address and the strength of the claims they make (Fig. 1). Source: A.T. Kearney analysis -

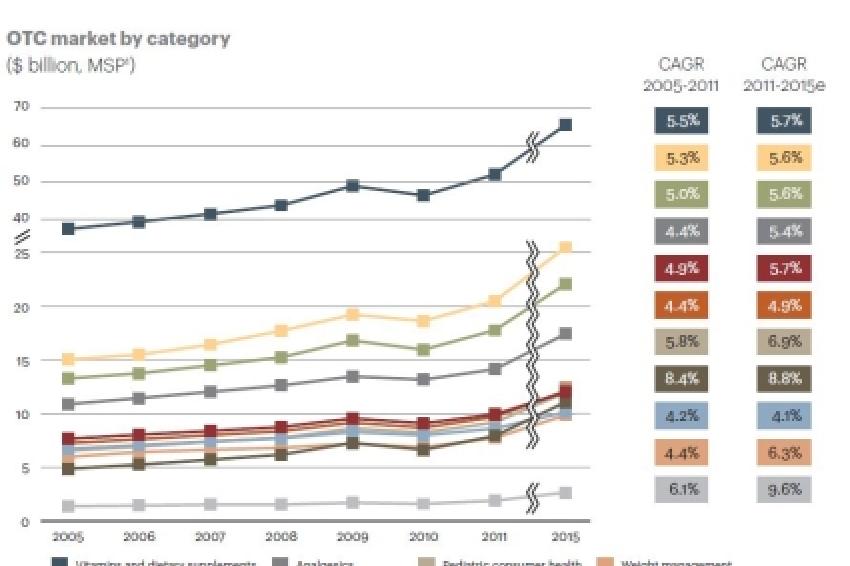

Market Growth A look at historical growth rates reveals that the relatively new lifestyle categories, such as food supplements and energy drinks, are driving market growth, signaling a shift from illness to wellness as the new consumer motivator (Fig. 2). Note: OTC = over-the-counter; MSP = manufacturer's selling price 1) Sales data: retail value MSP/$ billion, historic constant 2011 prices, forecast constant 2011 prices, historic fixed 2011 exchange rates, forecast fixed 2011 exchange rates 2) Includes calming and sleeping, wound care, ear care, eye care, smoking cessation using nicotine replacement therapy, emergency contraception, OTC triptans, and adult mouth care. Sources: Euromonitor, 2010: Consumer Health, Passport database; A.T. Kearney analysis

Market Growth A look at historical growth rates reveals that the relatively new lifestyle categories, such as food supplements and energy drinks, are driving market growth, signaling a shift from illness to wellness as the new consumer motivator (Fig. 2). Note: OTC = over-the-counter; MSP = manufacturer's selling price 1) Sales data: retail value MSP/$ billion, historic constant 2011 prices, forecast constant 2011 prices, historic fixed 2011 exchange rates, forecast fixed 2011 exchange rates 2) Includes calming and sleeping, wound care, ear care, eye care, smoking cessation using nicotine replacement therapy, emergency contraception, OTC triptans, and adult mouth care. Sources: Euromonitor, 2010: Consumer Health, Passport database; A.T. Kearney analysis

Growth Opportunities - A new market of consumer-focused healthcare products is emerging to occupy the space between consumer goods and pharmaceuticals-and becoming a battleground that giants in both industries are gearing up to dominate.

Many factors-consumer awareness of health issues, higher personal incomes, more focus on fitness, and the urbanization of emerging economies, just to name a few-have combined to create a new market for healthcare products. And the world's leading pharmaceutical and consumer goods companies are eager to do battle for this new market's seemingly unlimited potential.

On one side, the pharma industry is addressing explicit health needs with scientifically proven products, and learning how to market these products more effectively. On the other side, the consumer packaged goods industry is using compelling marketing stories about how quality of life can be improved, and learning to back up those claims with scientific evidence.

Choosing the Battlefield

With a wide range of product categories to choose from (c.f. Fig. 1), the question becomes which battle to fight-and where? Which categories are hot? Which markets are driving the most growth? Given the rise of chronic diseases, higher household incomes, and more consumer knowledge and awareness about health, one would expect the consumer health market to be growing by leaps and bounds everywhere. This is not the case.

Globally, consumer health markets are growing at an average of 5.7% but are lagging overall GDP growth. Compared to other categories, consumer health grows at a snail's pace, particularly when times are good. For example, between 2005 and 2012, consumer health categories in India grew by less than 13% a year, but the cosmetics market grew more than 27% per year. There is also a common belief that the market is being driven by consumers bearing an increasing burden of health costs. Not so: The proportion is actually falling, and consumer health spending generally lags overall health spending.

Several things are responsible for this relatively slow growth. First, getting people to become more health conscious is not easy. Second, the market faces a real innovation deficit. Portfolios of leading consumer health companies feature products that are an average of 30 to 50 years old. The OTC market has historically been driven by so-called Rx-to-OTC switches, where drugs containing certain pharmaceutical ingredients and available only with a prescription are licensed for sale over the counter once their safety profile is well established (and, typically, once the product has lost its patent protection). However, only a handful of active ingredients have achieved OTC-switch status in the United States over the past five years. Meanwhile, the pipeline of new pharmaceutical ingredients coming off patent is drying up, and the few that do exist, such as anti-psychotics and biopharmaceuticals, are unlikely to be suitable for purchase over the counter. In this market, innovation has been basically limited to marketing and product variants rather than scientific efforts.

This isn't to say the market lacks sweet spots of significant growth opportunities. A look at historical growth rates reveals that the relatively new lifestyle categories, such as food supplements and energy drinks, are driving market growth, signaling a shift from illness to wellness as the new consumer motivator.

However, a glance at the pharmacy and supermarket shelf shows that consumer health companies seem satisfied promoting trendy health supplements to young people who do not need them, rather than providing solutions to the very real health problems older people face.

The Winning Model

Given their respective histories, one would expect our two protagonists to approach the market battle with very different mindsets. Consumer goods companies would try to build global brands and use marketing muscle to win supermarket shelf space. Pharma, on the other hand, would use Rx-to-OTC switches as a source of innovation, maintaining their grip on pharmacy and specialist channels and building a portfolio of local assets. Indeed, this is pretty much what we found: Players apply the tactics they are most comfortable with and apply much the same approach across the portfolio.

It is difficult to say which is the winning model. In fact, we aren't convinced that either approach is inherently superior. The best tactics will depend on the category and the geography and the type of company you want to be. The two most important decisions will be the brand's role and the distribution channels.

Brand versus Category

Consumer goods and pharma companies define "brand" quite differently. To a consumer goods company, a brand is the articulation of a relationship with a consumer, encompassing personal aspirations, trust, and promises of performance. To a pharmaceutical company, a brand is a molecule-and the value of some of these molecules is enormous.

Unfortunately, it is hard to find any consumer health category where global brands under either definition have made any significant impact. A look at top brands across categories shows that global brands rarely achieve more than a few%age points of market share.

This does not mean that trying to build global brands is a pointless strategy. Big brands are a proven way to access growing mass-market channels. Global brands are also a good strategy for genuinely innovative products-though as we have mentioned, product innovation is sadly lacking in the consumer health industry.

However, the reality is that in most markets, consumer health companies will have to build on existing local brands that embody trusted relationships and are tailored to local needs. For this reason, it is probably more productive to pursue category leadership than building global brands.

We believe that if consumer health is to achieve its full potential, it needs to grow beyond Rx-to-OTC switches and clever marketing. It needs to develop science that truly addresses the health needs of the aging and chronically ill and build the expertise to reach out to consumers and help them embrace their own health needs. It needs to convince consumers and health professionals alike that its products are safe and effective, and generate the evidence to prove it.

It is enlightening to look at the evolution of the food industry, where many companies are adopting the category platform model. Innovation, technology, product concepts, and formats are shared across countries, while the brands with very strong local consumer loyalty are maintained.

Specialist versus Mass-Market Channels

Nothing illustrates the battle for consumer healthcare more clearly than the choice of distribution channels. Historically, pharmacies have been the dominant consumer health channel, protected by both tough regulation and customer expectations of where health products should be sold. However, there is a trend for deregulation, supermarkets are becoming more credible for health and beauty products, and much of the growth is coming from lifestyle products. Also, while developing countries are seeing an expansion of pharmacies, pharmacy floor area in most developed markets - and even in Russia and Brazil - is declining, according to Datamonitor.

Overall, this means that most of the growth in consumer health sales, even OTC medicines, is occurring in mass-market channels.

Do pharmacies and specialist channels matter anymore? Absolutely! First, pharmacy deregulation has proved to be incredibly slow in most markets, so pharmacies remain the only route to market for many products. Second, margins generated in pharmacies and specialist channels are generally far higher than in supermarkets. Finally, specialist channels such as pharmacies and dentists provide the expert endorsements that justify premium pricing, which can carry over to the supermarket shelf.

The key for the successful consumer health company is to use specialist channels to maintain clinical credibility while using mass-market channels to achieve wide distribution-easier said than done, to be sure.

Who will be the Winners?

The fight for the consumer health market is a war with multiple fronts, and participants will have to organize effectively, move swiftly, and know which battles they must take on and which tactics will ensure victory.

As in all types of evolution, the winners will be those that adapt best to their rapidly changing environment. The winners in consumer health will be an entirely new species, but it is far from clear which gene set will prevail.

We believe, however, that the consumer health company of the future will be an amalgam of the two industries, able to engage consumers and prove the clinical effectiveness of their products and as adept at dealing with medical professionals as negotiating supermarket shelf space. Even more important, such a company will have the ability to identify unmet consumer needs and develop innovative ways to unlock true value in the marketplace.