The Future of Pharma

The Deconstruction of the Pharma Value Chain May Not Be a One-Size-Fits-All Recipe for Big Pharma

-

© Guido Vrola - Fotolia.com

© Guido Vrola - Fotolia.com -

Andrew Badrot, CMS Pharma

Andrew Badrot, CMS Pharma -

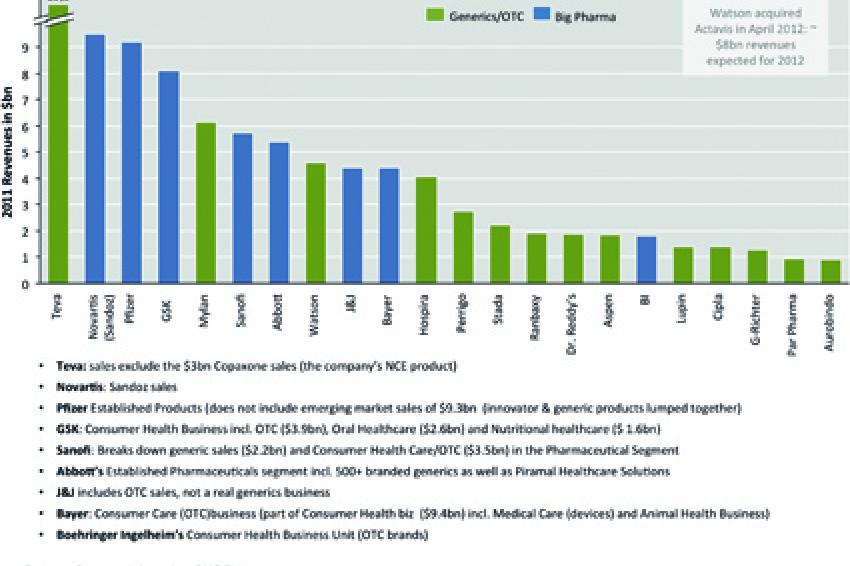

Fig 1

Fig 1 -

Fig 2

Fig 2

The Rise Of Generics - In 2011, CMS Pharma was invited to take part in a conference in Mumbai to discuss the emergence of "supergenerics," a new form of generic drugs with improved properties such as safety, efficacy, stability or improved commercial attractiveness such as taste or route of administration. Those drugs are most often based on an incremental reformulation of a generic API (active pharmaceutical ingredient) or the combination of multiple generic APIs.

Leaving the conference, we were convinced supergenerics had a role to play in the future of the pharmaceutical industry. The main Indian players, Cipla, Ranbaxy, Dr. Reddy, Lupin, Zydus, Sun and others were all vying for a piece of the action.

The benefits of supergenerics seem compelling. Development costs tend to be limited with investments in the range of $50 million, which in the pharmaceutical world is considered to be a rather small ticket. Development timeframes are also short, ranging from three to four years, significantly less than the 12-year average needed to commercialize new molecular entities. A successful outcome could yield a combination drug, a new formulation or a new route of administration, with three to five years of exclusivity in the USA under USFDA 505(b)(2).

But beyond the short-term financial benefits to the various players in the marketplace, it was still unclear to us how big of a game changer supergenerics would be longer-term. With the pervasive myth that generic drugs are not really profitable, one could reasonably question the effect of those drugs in shaping the industry's future.

But facts speak otherwise. CMS Pharma compared the financial performance of the top 14 generic companies vs. the top 14 Big Pharma companies. The results clearly demonstrate the power of generics: Over the five years spanning 2007 to 2011, generic companies achieved an average EBIT margin of 18.5% while Big Pharma had 25.5%. That profitability gap of 7 percentage points is certainly noticeable but in no way can dismiss generics to be a "non-profitable" product class. By measuring corporate performance through return on assets (RoA), in 2010, generics achieved a RoA of 7.3% vs. 8.0% for Big Pharma, a near par. In fact, this set of generic companies trades at 30% higher valuations compared with its Big Pharma peers, with a TEV-to-EBIT ratio of 12.6 times vs. 9.4 times for Big Pharma in 2011.

In addition, looking at the topline growth of the pharmaceutical business beyond 2016, IMS estimates nearly $1.4 trillion in pharmaceutical drug sales by 2020. Two-thirds of the growth between 2012 and 2020 is forecasted to come from emerging countries, including BRIC, where generic drugs dominate the market. We estimate that approximately 50% of future global pharmaceutical drug market growth will come from generics.

So Why Does It Matter?

At the J.P. Morgan Healthcare Conference 2013, Jeremy Levin, Teva's CEO, discussed at length his "fusion" of R&D and the new strategy for the development of NTEs (new therapeutic entity), an acronym coined by Teva to describe its strategy for combining APIs, reformulating them or developing new delivery mechanisms. Whether labeled NTEs or supergenerics, the perspective painted by Teva for the future of medicines is powerful and compelling.

Through its vision, scale and focus, Teva is bringing supergenerics/NTEs to the industry forefront and is using it as a transformational driver over the coming 10 years.

As a fully integrated pharma company with one of the broadest portfolios of drugs marketed globally, integrated capabilities in API and formulation development, production in 74 factories globally, and nearly $1.2 billion in R&D spending, Teva is refocusing its core growth strategy around NTEs. And if anyone can deliver that vision, Teva is ideally positioned to do so. Why? We see three reasons that set it apart from its peers:

- Teva is focused on generics like no other company of its scale is.

- Teva is by far the largest generics company, supplying one in six prescription drugs in the USA and 71 billion tablets worldwide. It has the largest portfolio of generic drugs with more than 1,300 molecules.

- With its broad and cost-effective manufacturing base and supplier network, Teva can deliver well-priced solutions to the market, quickly and reliably.

In addition, Teva can play eye-to-eye with its innovator peers on the following points:

- Teva also has new chemical entity (NCE) development capabilities: Copaxone is its leading treatment for multiple sclerosis with $3 billion in sales in 2011 accounting for one-third of the MS market. Additionally the company has 15 drugs in late-stage development and another 13 programs in mid-stage trials. It has added innovator biotech expertise following the acquisition of Cephalon two years ago.

- It has the R&D know-how both on the generics and NCE side, and thus can create cross-pollinated teams with advanced technical skillsets in both areas. This in turn speeds up the R&D discovery process and increases chances of creating effective combination drugs.

- Finally, with its extensive regulatory expertise, Teva is well suited to work hand-in-hand with regulatory agencies to review and frame the approval processes for those NTEs.

What Could it Mean to Big Pharma?

If the "fusion" of NCE and generic R&D delivers its promise, if Teva succeeds in delivering above-average returns to the industry, where will it leave the rest of its Big Pharma peers?

Some Big Pharma may enter the "fusion" fray. Novartis (through Sandoz) has a substantial generics business. GSK, Sanofi, J&J and Bayer also have strong franchises with a combination of generics and OTCs while Boehringer Ingelheim has a large OTC portfolio. They all have the R&D strength to pursue such an approach. Abbott decided to go down an opposite path and split its generics and NCE business. Abbott retained the established pharma product group together with medical devices, diagnostics and nutrition while the newly established Abbvie held the innovator business. Pfizer, another behemoth in generics, is rumored to consider a split, too.

The divestment strategy from manufacturing pursued by some Big Pharma in order to refocus on the R&D and marketing components of the pharmaceutical value chain could be problematic: while this strategy may lead to a financial payoff in the midterm, we believe it will also lead to a loss in technology know-how that will indisputably penalize the pharmaceutical companies' long-term outlook. Pharma being an innovation-driven business, manufacturing needs to remain a core competency, which in itself drives and generates a significant amount of R&D. McKinsey's latest report ("Manufacturing the Future: The Next Era of Global Growth and Innovation", November 2012) estimates up to 90% of global private R&D spending is driven by manufacturing.

What Could the Future for Big Pharma Look Like?

Venturing to look into the future, Big Pharma in 2025 could be a streamlined organization that develops, manufactures and markets drugs worldwide, a back-to-the-future scenario defying some of the current wisdom circling some executive suites:

- R&D along the "fusion" model from Teva is a very attractive contention and could likely over-perform the "split" model pursued by Abbott and possibly others.

- Manufacturing will be based on core knowledge held by the company combined with outsourcing intended to manage capex, enhance risk-mitigation linked to supply chain events and load-balancing of the manufacturing footprint.

- Marketing will no longer differentiate between innovator drugs and branded generic drugs. All will be marketed through similar channels under the same company brand. Indeed, why ignore the mass-market power of generics and limit the brand awareness? All drugs, OTCs included, will become sought-after vehicles putting the brand on patient tables and bathroom mirror medicine cabinets. Expecting patients to value an NCE and a generic drug differently is like expecting a car driver to value a spark plug from Bosch differently from NGK. They won't.

___________________________________________________________

This article is co-published in Contract Pharma.

Contact

CMS Advisors GmbH & Co. KG

Rheinstr. 194b

55218 Ingelheim

Germany

+49 6132 43678 20

+49 6132 43678 50