The Shale Gas Game

Part 1: Shale Gas Resources and Development Trends in Major Economies

-

© Gina Sanders - Fotolia.com

© Gina Sanders - Fotolia.com -

Dr. Sven Bugarski Stratley

Dr. Sven Bugarski Stratley -

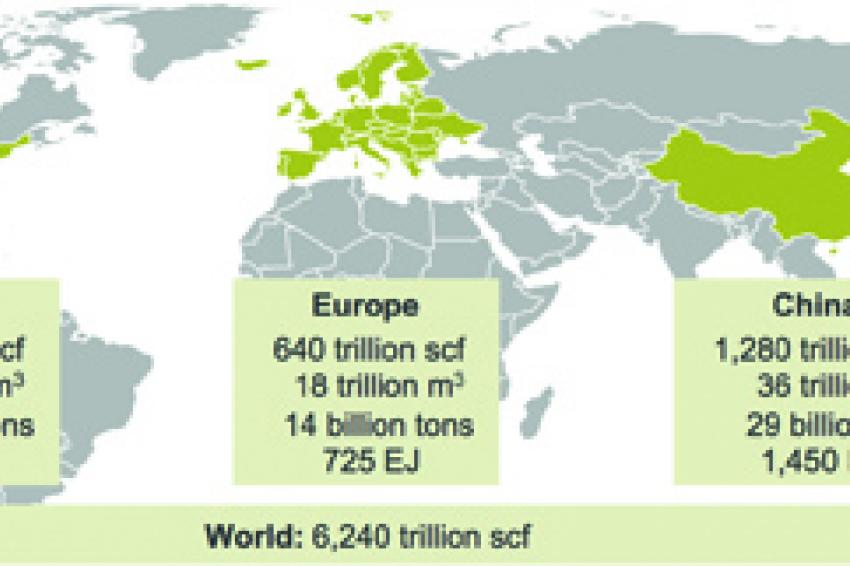

Figure 1: Global discovered technically recoverable shale gas resources Source: EIA; Stratley analysis. Note: Europe excludes Russia; mass estimation in tons by using average shale gas mass density of ≈ 0.8kg/m3; average energy value of shale gas: 1 scf ≈ 1.13 million J. As wet shale gas is assumed for average value calculations, mass and energy values can be seen as upper limits.

Figure 1: Global discovered technically recoverable shale gas resources Source: EIA; Stratley analysis. Note: Europe excludes Russia; mass estimation in tons by using average shale gas mass density of ≈ 0.8kg/m3; average energy value of shale gas: 1 scf ≈ 1.13 million J. As wet shale gas is assumed for average value calculations, mass and energy values can be seen as upper limits. -

Figure 2: Energy content of global fossil deposits as of 2011 Source: DERA; EIA; Stratley analysis. Note: The shale gas reserves figure is a very rough estimate as of Q1/2013 and is an upper limit for the time being.

Figure 2: Energy content of global fossil deposits as of 2011 Source: DERA; EIA; Stratley analysis. Note: The shale gas reserves figure is a very rough estimate as of Q1/2013 and is an upper limit for the time being. -

Figure 3: Range of methane and ethane supply from shale in the US Source: EIA; Oil & Gas Journal; Stratley analysis. Note: Methane density = 0.68kg/m3 and ethane density = 1.28kg/m3. It is assumed that US shale gas (total resources: 500 tcf) contains 85 ± 5% methane and 6 ± 2% ethane on average, both very rough estimates.

Figure 3: Range of methane and ethane supply from shale in the US Source: EIA; Oil & Gas Journal; Stratley analysis. Note: Methane density = 0.68kg/m3 and ethane density = 1.28kg/m3. It is assumed that US shale gas (total resources: 500 tcf) contains 85 ± 5% methane and 6 ± 2% ethane on average, both very rough estimates.

Headlines frequently state that shale gas is a "game changer". A game usually implies that there are winners and losers among its participants. However, the shale gas game is not limited to its active players such as upstream and midstream companies, but also affects downstream players in a world with an increasingly competitive and volatile raw materials landscape. Understanding global shale gas developments and anticipating downstream threats and opportunities is not just an interesting academic exercise, rather, it is a necessity for numerous strategic investments and raw material sourcing issues.

Hence, the question for a large number of global chemical companies is not whether they want to join the game, but more how to play it as involved participants.

Before considering implications for downstream players, it is important to critically review the potential of shale gas both in terms of resources and production. Part 1 of this article focuses on assessing the sustainability of shale gas supply and provides an outlook on the developments in the two major economies of China and Europe. Part 2 (in CHEManager Europe's May issue) will focus on the implications of shale gas for downstream players.

Is Shale Gas a Long-Term Resource?

As indicated by the Energy Information Administration (EIA) and various other sources, shale gas is available on all inhabited continents in large amounts and much more widely distributed than conventional oil and gas resources. This makes it a truly global resource with current estimates of around 140 billion tons (7,000 EJ) of discovered technically recoverable shale gas. Available exploration data is currently limited - especially outside the US - thus, this figure is likely to increase in the coming years. Fig. 1 shows the figures currently circulating in the gas business for technically recoverable resources in three major economic regions in various units.

While these large numbers seem to be impressive, they are difficult to interpret in terms of impact. By comparing them with conventional resources and consumption rates, they can be put into better perspective.

A quick look at shale gas and appropriate conventional resources reveals that the energy content of shale gas is comparatively small. The same applies to the reserves that are defined as resources that are economically recoverable. Even if technological progress or increasing gas prices result in significantly higher reserves, shale gas is not the globally dominant raw material in terms of deposits.

This is even more understandable if one considers that there are various other energy and feedstock sources in addition to those mentioned in Fig. 2, e.g. nuclear energy, shale oil, coal bed methane, etc. Nevertheless, in areas rich of shale gas, it can become a major source of energy and feedstock, as can be seen in the Marcellus area in the US, for example.

More than a Temporary Hype in the US

An analysis of shale gas consumption requires a more differentiated view of shale gas. Shale gas is generally a mix of alkanes: methane and natural gas liquids, with its main components being ethane, propane, butanes and natural gasoline. Fig. 3 shows how long the two dominant constituents of shale gas in terms of volume - methane and ethane - can meet future US demand. To calculate the range figure in years for methane, estimated US shale gas production rates are used. For the range figure in years for ethane, US ethane cracker capacity for ethane from shale is used. In the calculations it is assumed that half of the total US cracker capacity as of 2017 for ethane can be covered by conventional gas or from sources other than shale and the other half is covered by ethane from shale.

Reserves are likely to significantly increase in the next years, thus today's resources are used for the estimations and the resulting time values are clearly upper thresholds. The actual time values are somewhat lower, but still might be a few decades. Based on today's available data, our rough analysis above leads us to the following answer to the question above: Shale gas in the US is definitely more than a subject of temporary hype. It has the potential to meet gas demand for the next decades. However, it will only be one energy and feedstock supplier among other sources and cannot be seen as the long-term solution to meet society's current high energy and feedstock demands.

Will there also be a shale gas boom in China and Europe? Considering the large estimated shale gas resources in China (29 billion tons) and in Europe (14 billion tons) and stagnating conventional gas production rates, this question appears to be reasonable. The conditions and drivers in China and Europe are different, hence the two regions have to be evaluated separately with respect to their shale gas development potential.

Can China Meet or Beat the 2020 Target?

The Chinese government has recognized its huge shale gas deposits as a valuable resource. By offering subsidies and by defining a clear production target for 2020 (12-24 million tons/year), the government is highly supportive and clearly aims to increase its raw material autarky. Environmental issues are rather treated as challenges to be addressed than as threatening obstacles. Is a game-changing shale gas boom thus expected to occur in China as it has done in the US?

One obstacle frequently stated in the shale gas community is the oligopolistic market. 80% or more of the known shale gas resources are under the control of China's two largest oil and gas players, Sinopec and PetroChina. Under current conditions, small and medium-sized Chinese enterprises, as well as international upstream companies, can hardly acquire access to the resources. While this market is certainly different to the market in the US, we would not draw the conclusion that the market conditions in China are either more or less favorable than in the US.

Instead, we focus on shale gas extraction costs and technology. There are strong indications that Chinese shale gas is, on average, located in shale plays 3-4 km below the surface, in often hilly and/or remote locations in the Sichuan and Tarim basins. Up to half of the total Chinese shale gas resources are in the arid and remote Tarim basin, where the extraordinarily high water supply and infrastructure costs impede development. The Sichuan basin has more favorable conditions and belongs to the basins where the most exploration activity is taking place. Shale gas production costs there are currently well above $10/MMBtu (≈$500/t) and even with learning curve effects, the production costs are not expected to compete with US production costs of $4-6/MMBtu (≈$200-300/t). Furthermore, Chinese shale gas is believed to be mostly methane, lacking the additional revenue of higher-valued natural gas liquids.

However, China has a very large domestic gas demand and gas import costs are high enough to justify investments into domestic shale gas development. The question is not if, but rather how fast China will develop its shale gas business. For this, they need technology, which has to be customized to the local topographic, geological and infrastructure conditions. Gas handling and transport facilities also have to be built. Catching up with technology and infrastructure may take a decade, but then a large-scale increase in shale gas production seems to be feasible.

Can Europe Remove the Obstacles?

Excluding Russia, with its enormous conventional gas resources, Poland (187 tcf, EIA), France (180 tcf, EIA), Germany (46 tcf, BGR), Ukraine (42 tcf, EIA) and the UK (20 tcf, EIA)* have so far been the main countries identified as having large shale gas resources and development potential. Although drilling and fracking technologies have become more efficient and environmental impacts have been reduced, the governments in Germany and France remain very restrictive about shale gas due to environmental concerns, impeding any investments that might lead to commercial projects. The governments of Poland, Ukraine and the UK see shale gas as a potential new contribution mainly to their own energy needs and possibly also as a chemical feedstock source.

Exploration of basins and shale gas production cost evaluations have already started in Poland and the UK and will presumably start in Ukraine soon. While in Poland enthusiasm has been somewhat dampened by test well yields being below expectations, the UK has obtained promising exploration data, e.g. in Lancashire and southern Scotland. Even in the more shale-gas-supportive countries in Europe, the regulation framework has yet to be finalized and widespread exploration remains to be done before large-scale commercial projects can become possible.No Shale Gas Boom in China and Europe Before 2020

Based on our assessment of the two regions, and also taking various expert interviews in both China and Europe into account, we believe that there will be no shale gas boom similar to the current boom in the US in China and Europe before 2020. China may reach a production rate of up to 24 million tons/year by 2020, while Europe will remain largely explorative, with local projects in the UK, Ukraine and Poland. A prediction beyond 2020 is difficult, as this highly depends on governmental decisions and trends in the energy sector. However, current data and trends indicate that China could eventually trigger off large-scale commercial shale gas production projects that contribute to the domestic hydrocarbon supply mix. In Europe, large-scale commercial production may occur in selected countries such as the UK, Ukraine and Poland in the mid- to long-term.

The answers to the questions lead to the conclusion that the US shale gas boom is substantial and that China and Europe will not experience a similar boom in the next years. Hence, US prices for methane and ethane are expected to remain significantly below the respective prices in China and Europe. In the subsequent second part of this article "Changes in Global Alkene Supply and Strategic Implications Beyond the Obvious" to be published in CHEManager Europe's May issue, we will elaborate on the effects of this US energy and feedstock cost advantage for the chemical industry and create awareness of opportunities and threats beyond the obvious.

Sources: Bundesanstalt für Geowissenschaften und Rohstoffe (BGR), Deutsche Rohstoffagentur (DERA, part of BGR), Energy information administration (EIA), Expert discussions on shale gas conferences, Oil & Gas Journal, Stratley China office, Stratley experts in Germany, Stratley project experience.

Contact

Stratley AG

Spichernhöfe Spichernstraße 6A

50672 Köln

Germany

+49 221 977 655 0