C3X Survey 2013: From Collaboration to Excellence in Chemicals

Survey Identifies Game Changers that Enable Chemical Companies to Outperform Peers in a Volatile Market

-

© fotogeng - Fotolia.com

© fotogeng - Fotolia.com -

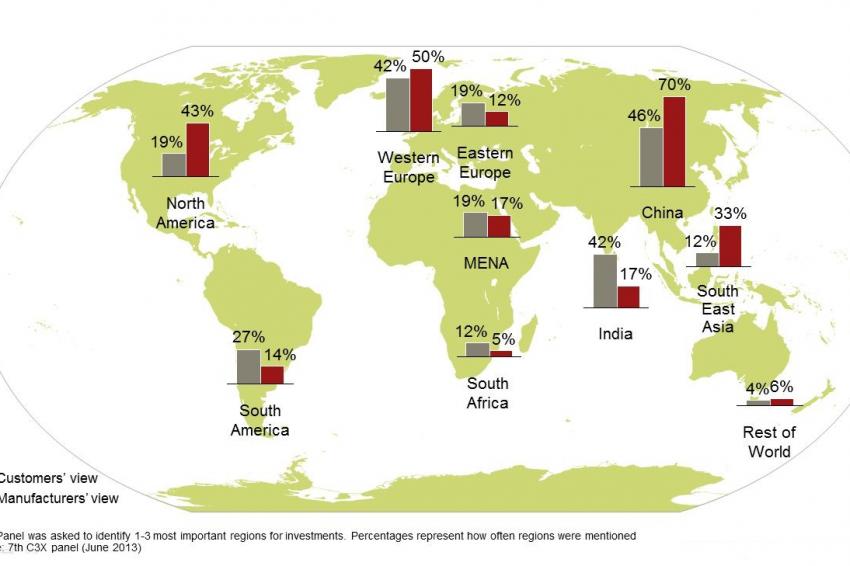

Figure 5: Where investments are going

Figure 5: Where investments are going -

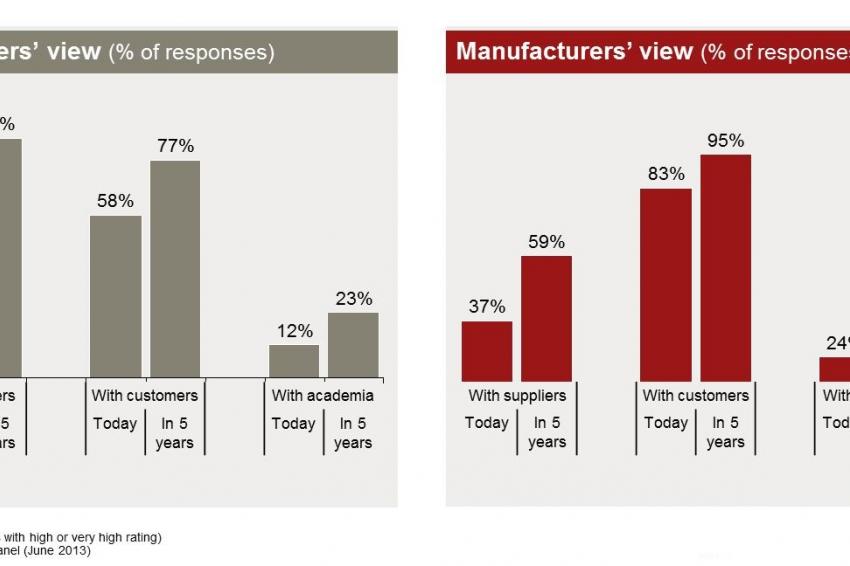

Figure 4: Degree of collaboration in the value chain

Figure 4: Degree of collaboration in the value chain -

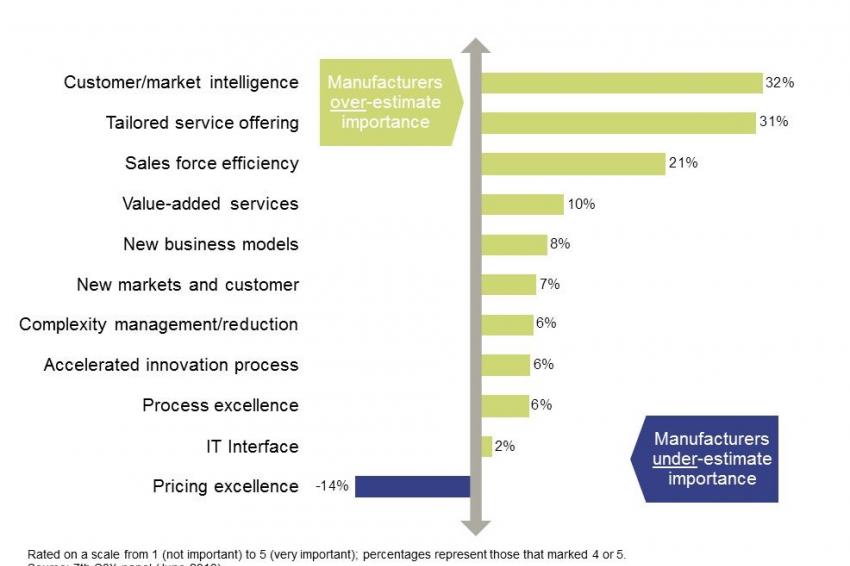

Figure 3: Perceptions about how to improve collaboration

Figure 3: Perceptions about how to improve collaboration -

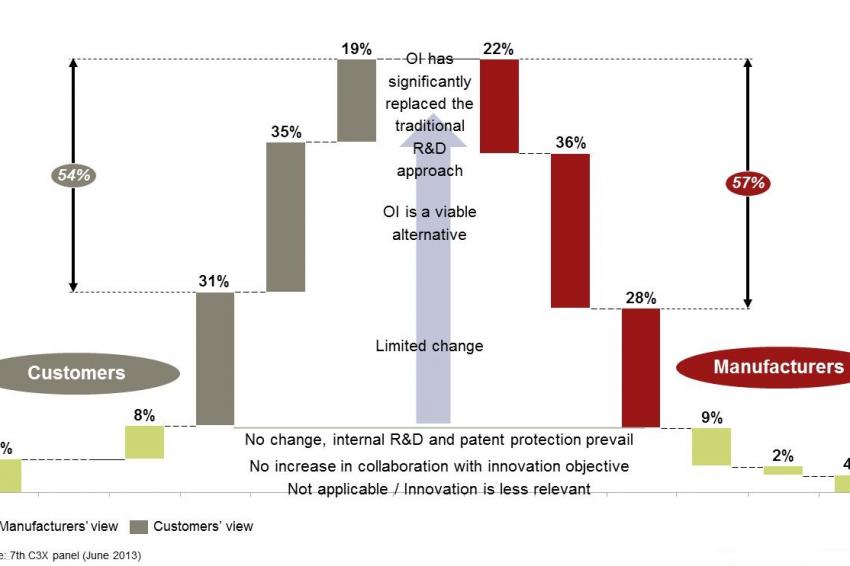

Figure 2: Influence of collaboration on ways to innovate

Figure 2: Influence of collaboration on ways to innovate -

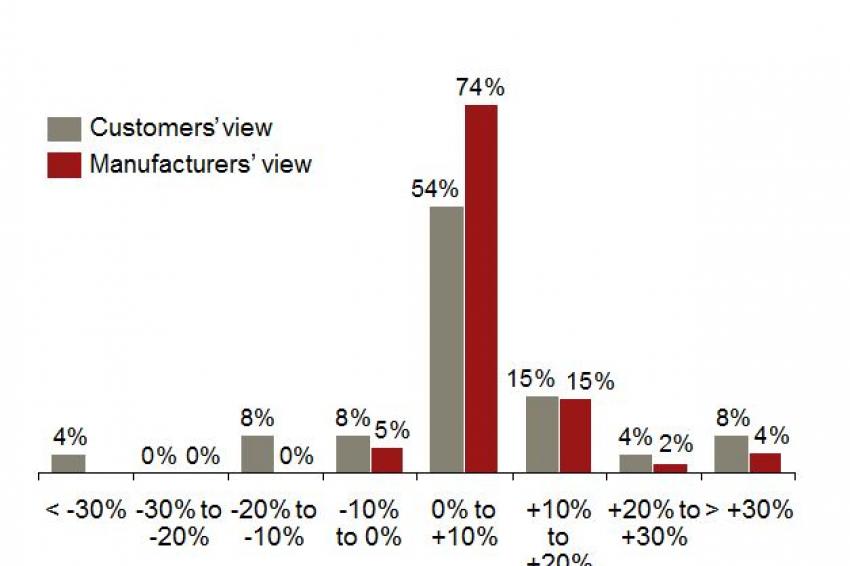

Figure 1: Demand development expectation for the next 12 months

Figure 1: Demand development expectation for the next 12 months -

Robert Renard, senior consultant in the Chemicals and Oil Practice, A.T. Kearney

Robert Renard, senior consultant in the Chemicals and Oil Practice, A.T. Kearney -

Dr. Tobias Lewe, partner in the Chemicals and Oil Practice, A.T. Kearney

Dr. Tobias Lewe, partner in the Chemicals and Oil Practice, A.T. Kearney

In recent years, chemical players have managed their businesses with little clear direction in the light of continuing volatile markets. They aimed to address the key strategic tasks by aligning strategies, increasing portfolio effectiveness or improving their operational fitness. Recently, the market has been lacking significant new impulses - some players have observed unexpected decreases in earnings, while others have benefited from more or less lateral development in their specific segments.

The 7th edition of the Chemical Customer Connectivity Index (C3X), a top survey conducted by A.T. Kearney, CHEManager Europe and the Institute of Business Administration at the Department of Chemistry and Pharmacy of Westfälische Wilhelms University Münster, Germany zoomed into top management views on these developments to determine the strategies to be followed to achieve excellence in chemicals.

Still, there is no silver bullet for future success, but the survey has identified a number of game changers that enable companies to outperform peers in a volatile market - provided they are addressed appropriately.

Sustaining profitability in a continuing volatile market environment

Over the past 12 months, chemical manufacturers continued on their growth path: 60% of all C3X panel participants experienced revenue growth of up to ten%. This growth was mainly achieved by passing on raw material cost increases.

However, one in four manufacturers - a comparably larger share than 12 months ago - saw their revenues decline.

Expectations going forward are brighter: In contrast to second quarter backdrops for some market players who were exposed to building blocks such as butadiene, the majority of panel participants expect their business to grow and to compensate the impact of raw material costs.

This is in line with recent economic outlooks published by the OECD or the World Bank for North America, China and selected European economies.

The majority of survey participants from the chemical industry - three out of four - envision growth of up to 10%, with the remainder even more positive, expecting 10% and more. Customers generally support this positive outlook, however, there is a relevant 20% of the panel who expect a decline.

All of the participants are well aware of the fact that the market is volatile. Further intensified efforts to become lean and increase operational efficiency need to be balanced in the light of increasing business system flexibility and the strengthening of core capabilities.

Dr. Tobias Lewe, Partner in the Chemicals and Oil Practice at A.T. Kearney explains: "Further analysis showed that few players are employing standardized pro-active crisis management tools in their management systems. Those that do use these tools expect themselves to be better prepared to secure profitability and financial liquidity in case of larger fluctuations."

Benefiting from an easing of raw material prices

Raw material availability and prices have flattened out since our last survey, with the relative importance attributed by panel members to the availability of supplies and alternative raw materials declining. For example, the price of US crude oil is projected by the World Bank to be flat to slightly declining and prices for gas-based derivatives have eased in the light of shale gas development.

Robert Renard, Manager in the Chemicals and Oil Practice at A.T. Kearney explains: "Manufacturers find themselves in a situation where market liquidity for most basic molecules has increased. This means the need to secure strategic raw materials has moved towards a need to be supplied with cost competitive materials, including in most strategic categories."

Going forward, excellence in supply management remains a major differentiator with regard to competition for chemical players' spend on direct material supplies often reaches 50 to 60% of their total cost, requiring leading-edge capabilities to manage it.

Supply management is expected to become even more integrated along the supply chain. This is being addressed by chemical manufacturers with a growing focus on the supplier (to realize common value improvements) as well as on the customer interface (e.g. collaborative innovation).

Reassessing the value of innovation in commoditizing markets

Before the credit crunch and economic crisis of 2008/09, most manufacturers saw the need for continued innovation and were undertaking significant efforts to place their bets on mid- to long-term developments.

Even during the crisis, manufacturers stated that they wanted to continue investment in innovation.

Since then, manufacturers have continued to focus innovation efforts on new product features (80%) and further strive to be perceived as innovation leaders (75%). These have been top priorities among C3X panel participants for the last five years.

On the customer side, a number of aspects have changed with regard to their ranking. Customers had already wanted to perceive their suppliers as innovation leaders in the previous years, but this now tops the list (81%).

Customers and manufacturers mutually agree that new applications/product features would appear to be more relevant than innovative business or service models.

The share of revenues that panel participants spend on innovation has remained stable over the last five years. Now, our participants are tending to be more critical about their innovation spend: For instance the share of customers that spend 2% or less has doubled in size, reaching 40% now.

For decades now, the chemical industry has been lacking real game-changing innovations driving additional growth. Maintaining market share and competitive positioning via incremental innovation is crucial.

Lewe explains: "For some segments the focus has shifted more and more toward engineering and technology investments aimed at further improving asset efficiency and scale."

Roughly half of the participants recognize that increased collaboration with their customers has changed their R&D approach toward open innovation.

Today already, one third of manufacturers are able to achieve price premiums through collaborating with customers on innovation.

Leveraging the supplier as well as the customer interface better

Participants have confirmed their view that future value generation is expected at the supplier as well as the customer interface: Excelling in pricing (77%), accelerating time-to-profit for innovations (65%) and process excellence (62%) are the main improvement levers.

Nearly 90% of customers meet their suppliers regularly. Two years ago, this was the case for only two thirds of all participants. The share of manufacturers that meet their customers' customers remained unchanged at 45%.

"We observed that participants have become more used to driving collaboration in a more professional and targeted way", says Lewe.

Although manufacturers still overestimate the value of generating market intelligence for 'internal use', customers benefit from the results of manufacturers' activities that drive collaboration more intensively (from 74 to 84%). Ultimately, customers confirm that this has increased strongly.

It is even assumed that this level will be able to be increased further to 95% over the coming five years.

In Europe's €650 billion chemical industry alone, the top line and cost benefit from intensified collaboration expected by manufacturers amounts to almost €30 billion.

In spite of the commonly agreed importance of collaboration, though, there are still obstacles to its implementation. Participants consider the lack of 'right' people and capabilities (48%) and the lack of trust shown to external parties (46%) to be the most important challenges.

Furthermore, there is a gap in terms of the importance of offering customized services. Nearly two thirds of manufacturers are working on improving their performance in this respect, while this is actually relevant to only 42% of their customers.

Demystifying sustainability

Overall, the relevance of sustainability-related aspects has declined, and the latest survey reveals the lowest values we have observed in recent years. Customers and manufacturers alike share this view, except with respect to the importance of waste disposal, which increased among customers. The latter also shows the greatest misperception between manufacturers and customers (32% of manufacturers, but 50% of customers now regard it as a priority). In the years before, customers rated it significantly lower, but it has now grown significantly.

Lewe says: "There is one interesting trend and question associated with it: Is sustainability really fading? The answers given illustrate that manufacturers in Germany, for example, still consider sustainability a little bit more important than their counterparts in other countries do. At the same time, we know that the economic situation in these countries is more problematic. Potentially, sustainability is a topic that is given less attention when the financials are really tight."

A second observation: Environmental sustainability issues, such as waste disposal or reusability, are much more of a concern for customers outside of Europe. Keeping in mind that environmental sustainability has been primarily a European notion, this might indicate that a certain level of satisfaction has been achieved in Europe and that industry in non-European countries is now beginning to see the light.

Leveraging distributors to reduce portfolio complexity

Managing complexity has been a major focus for many manufacturers for quite some years now. In parallel and in line with a continued streamlining of portfolios, the role and importance of distributors has increased globally.

Panel participants have named distributors and resellers as one if not the most important collaboration partners going forward.

Renard explains: "Distributors are seen as instrumental to enabling one to focus one's own activities on key accounts, markets and regions. They are also being increasingly deployed to realize selected value added in terms of formulation, logistics services, speed to customer, enablement of lean back offices or even by offering complementary products. At the same time, expectations with respect to distributor performance and capabilities have increased in line with the need to collaborate better along the value chain."

This emerging trend is actually mutual: While distributors and resellers are repositioning themselves as partners, manufacturers are also increasingly recognizing the movement toward and benefits of engaging with one another on an equal footing.

Other partners highlighted by the participants include major customer groups served by manufacturers: Chemicals, plastics and rubber (14%), automotive and automotive parts (13%), construction, building and materials (11%) and consumer goods (7%).

Placing the right regional bets for growth

New energy sources have not, at least not yet, had any significant impact on companies' investment decisions. Nearly a third of manufacturers and customers stated that these new sources had no impact at all.

The impact on the related supply and demand balances was marginal, also. Nearly one in two manufacturers and three quarters of customers experienced no or minimal changes.

Participants will continue to focus their near-term investments (over the next three years) on building up manufacturing capacity in China. 70% of manufacturers and 46% of customers rank China as the focus region.

For manufacturers, Western Europe (50%) and North America (43%) follow as the next most important regions. Compared to recent panels, North America has seen a significant improvement as a potential location for near-term investments: For example, in the 2011 C3X, only 8% of manufacturers saw North America as a target for investment at all.

Customers, on the other hand, have indicated much stronger investments in India and South America, with 42% and 27%, respectively, naming them as top regions.

About C3X

The objective of C3X is to analyze the chemical industry from the vantage points of chemical companies and their customers. The survey captures the views of senior executives from leading European chemical companies and of decision-makers in customer industries working at the interface to their suppliers. Participants in this seventh C3X survey, which was conducted in June and July 2013, included executives from 10 European countries as well as from the US, India, South Korea and China, representing chemicals firms and client companies - a total of about 150 executives in all. The customer industries cover a variety of different sectors, ranging from the automotive and food industries to the cosmetics sector.