Camelot’s Pharma Management Radar

Effectively Addressing Today’s VUCA Challenges: LEAN Supply Chain Planning for the Pharmaceutical Industry

-

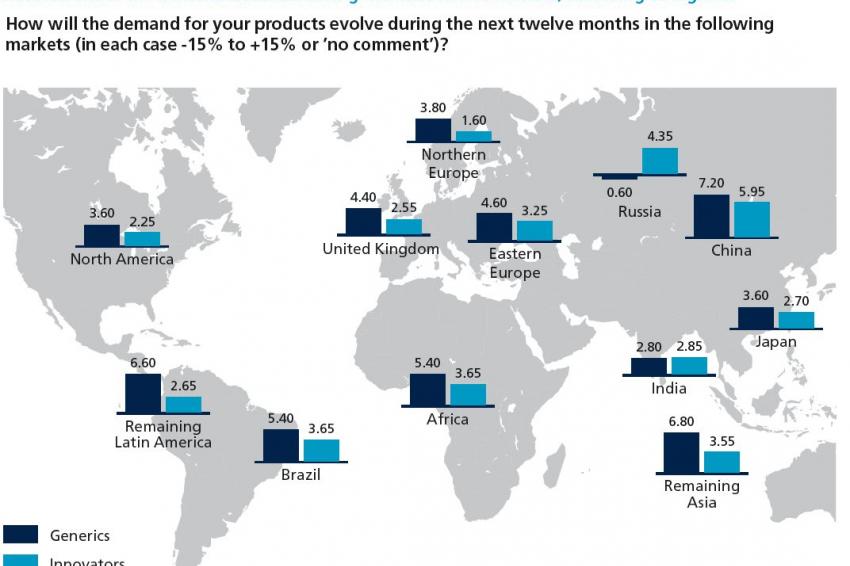

Assessment of the demand situation during the next twelve months, according to regions. Copyright: Camelot Management Consultants

Assessment of the demand situation during the next twelve months, according to regions. Copyright: Camelot Management Consultants -

Assessment of business risks in the pharmaceutical industry. Copyright: Camelot Management Consultants

Assessment of business risks in the pharmaceutical industry. Copyright: Camelot Management Consultants -

Most promising countermeasures against VUCA challenges in Supply Chain planning. Copyright: Camelot Management Consultants

Most promising countermeasures against VUCA challenges in Supply Chain planning. Copyright: Camelot Management Consultants -

Dr. Josef Packowski, managing partner, Camelot Management Consultants

Dr. Josef Packowski, managing partner, Camelot Management Consultants -

Michael Jarosch, head of industry segment pharmaceuticals and life sciences, Camelot Management Consultants

Michael Jarosch, head of industry segment pharmaceuticals and life sciences, Camelot Management Consultants -

Ronald W. Bohl, senior director supply chain, Eli Lilly

Ronald W. Bohl, senior director supply chain, Eli Lilly

Power Of The Unknown - Despite a generally positive estimation of the current business climate, global pharmaceutical companies face challenges that endanger their business development.

Many of these challenges can be summarized under the term VUCA, an acronym for "volatility, uncertainty, complexity and ambiguity," that describes precisely the conditions of increasing variability and uncertainty of demand, and the complexity and ambiguity of product portfolios and supply-chain networks in which companies are forced to operate today. Nearly all of them consider themselves affected strongly or even very strongly by VUCA challenges.

At the same time, many industry players are hesitant to take appropriate action in the field of supply-chain planning - although most of them have a clear vision of what the right countermeasures against countermeasures should be.

This is the picture that emerges from the third Camelot Management Consultants Pharma Management Radar, a biannual survey among an expert panel consisting of almost 100 executives from leading globally active pharmaceutical companies based in 16 countries and spread over four continents. Survey participants represent almost two-thirds of the global Top 20 pharmaceutical companies. The focus topic of the third Pharma Management Radar is supply-chain planning in a VUCA world.

Lowered growth expectations for emerging markets

Although the pharmaceutical industry is still suffering from the Euro zone crisis in various regions, it is no longer as extremely focused on emerging markets. The tremendous growth expectations registered last September for countries and regions such as Eastern Europe (8.5%), Russia (9.5%) or Brazil (9.6%), have cooled down to an almost disillusioned level of around or below 4%. Some respondents are particularly pessimistic with regard to Russia, which has politically veered away from the West during the past months: It is the only region in the world in which even generics expect decreasing demand in the next 12 months.

In accordance with their lowered growth expectations for the emerging markets, the pharmaceutical companies are returning to the established markets with their regional investment plans for the next 12 months. Compared to the last survey, Northern Europe and North America have gained considerably with regard to investment attractiveness. This trend is particularly strong among generics respondents, who are all planning to invest in Northern Europe (including Germany) in the next 12 months.

All in all, investment plans reflect the optimism of the positive general business climate: The share of respondents who do not plan any regional investments at all has further decreased since the last survey.

VUCA Challenges Affect the Whole Industry

Asked for the greatest risks for their companies' business development during the next 12 months, many participants name complexity, rising volatility and uncertainty - factors generally subsumed under the term VUCA. The latter also plays a role in the most important industry trends. "Countermeasures against rising complexity" as well as "countermeasures against rising volatility and uncertainty" rank relatively high. When looking at the two predominant business models separately, "concentration on emerging markets" is - alongside the two VUCA countermeasures - among the top three trends for the generics sector. This is due to the growth potential the generics see in these regions.

When asked directly about the influence of VUCA challenges on the companies' business success, the respondents virtually speak with one voice: Nearly 90% consider their business to be affected "strongly" or even "very strongly" by VUCA challenges. None of them thinks that VUCA challenges have no effect at all.

VUCA awareness is particularly strong within the generics segment, with all respondents feeling affected by these challenges at least strongly. Among the innovators, only a small minority considers business to be hardly affected by VUCA challenges. According to the industry executives, supply chain and production stand out as the business functions affected most by these challenges.

With regard to the biggest threats caused to the supply chain by VUCA challenges, "high volatility in demand and supply" is indisputably considered the main problem, while opinions differ with regard to other possible threats. It is striking, for instance, that innovators attach far less importance to the threats of "increased risk of stock outs" (37% vs. 60%) and "need for high safety stocks/inventories" (32% vs. 60%).

This may be traced back to the fact that innovators are used to having comparably high inventories to avoid stock outs - which is, however, not efficient under the cost aspect. As a consequence, the answers imply that many innovators do not make much progress on their way toward modern supply-chain planning.

Countermeasures Against VUCA Challenges

When it comes to countermeasures against VUCA challenges, some highly interesting discrepancies between current action, planned action and wishes can be observed: Currently, the pharmaceutical companies mainly focus on "improved forecast accuracy" and "demand-driven supply-chain planning." Concerning the countermeasures that the pharmaceutical industry's executives personally consider most promising for the future, "leveled production and utilization" plays a considerably stronger role.

The discrepancy between personal assessment and actual planning is further illustrated when asking which countermeasures against VUCA challenges in supply-chain planning the various companies have planned for the near future. Regarding the top answer, there is a much higher share of respondents wishing to apply demand-driven supply-chain planning than of respondents whose companies have planned to actually do so.

This discrepancy can also be found with regard to "leveled production and utilization," which one-third of respondents consider promising but only one-fourth have planned for the near future.

Taking a closer look at innovators, this phenomenon can also be observed when it comes to increased flexibility in production patterns (wish: 37%, plan: 21%). In addition, there seems to be a considerable need for action concerning leveled production (wish: 26%, plan: 16%) in this segment.

To find out why the various players in the pharmaceutical industry do not do as they wish with regard to VUCA countermeasures, it is helpful to realize what they consider the biggest hurdles for successful implementation of such measures. The participants' answers show that conceptual, organizational and IT-related issues are perceived as the main hurdles.

This in turn allows for the conclusion that the VUCA challenges must be addressed with an integrated conceptual approach in order to fight them effectively - comprising strategy, organization and processes, and IT systems. And it seems that the VUCA challenge is perceived to be too big for further single initiatives, as a truly integrated approach implies a major transformation of the global supply chain, including the necessary change-management program and board sponsorship.

Given all these hurdles it shows that the most promising countermeasure against the challenges of today's VUCA world lies in a process-oriented cross-functional and fully integrated end-to-end LEAN supply-chain planning concept. The latter can be found in Camelot Management Consultants' concept of LEAN supply-chain management, which has specifically been developed to address today's VUCA challenges most effectively.

To participate in the next Pharma Management Radar survey please register here!

Contact

Camelot Management Consultants AG

Theodor-Heuss-Anlage 12

68165 Mannheim

+49 621 86298 0

+49 621 86298 250