Current and Future Trends for Pharmaceutical Logistics

Pharma Management Radar Survey Finds Optimism but also Expectations To Cut Costs

-

Dr. Josef Packowski, Camelot Management Consultants: “Logistics will play an increasingly important role for coping with future challenges in the global pharmaceutical value chain.”

Dr. Josef Packowski, Camelot Management Consultants: “Logistics will play an increasingly important role for coping with future challenges in the global pharmaceutical value chain.” -

Andreas Gmür, Camelot Management Consultants “We have seen already a shift in the organization of logistics: from a local approach to a regional/global one.”

Andreas Gmür, Camelot Management Consultants “We have seen already a shift in the organization of logistics: from a local approach to a regional/global one.” -

Illustration 1

Illustration 1 -

Illustration 2

Illustration 2 -

Illustration 3

Illustration 3 -

Illustration 4

Illustration 4 -

Illustration 5

Illustration 5

A wind of change is in the air when it comes to logistics in the pharmaceutical industry. Although most companies are still quite optimistic with regard to the current business climate, there seems to be a rising awareness of the important role logistics might play in current and future challenges such as price pressure. And new service offerings "beyond the pill" also could affect logistics substantially: The majority of industry players are currently executing focus initiatives in various fields of logistics, including organization, process and network setup. At the same time, however, there is still some room for optimization with regard to various strategic changes in logistics to further increase competitiveness.

This is the picture that emerges from the fifth Camelot Management Consultants Pharma Management Radar survey, a biannual survey that examines the general climate in the pharmaceutical industry and takes an in-depth look at a varying current management topic. In a one-week period between January and February, more than 20 executives from globally active pharmaceutical companies based in 16 countries and spread over four continents participated in the online survey. Companies with a business model predominantly characterized by developing and/or commercializing innovative medicines ("Innovators") comprised the majority of respondents; roughly one-fifth were participants from companies predominantly active in the generics segment ("Generics"). Panel participants represent almost two-thirds of the global Top 20 pharmaceutical companies. The focus topic of the fifth Pharma Management Radar is pharma logistics.

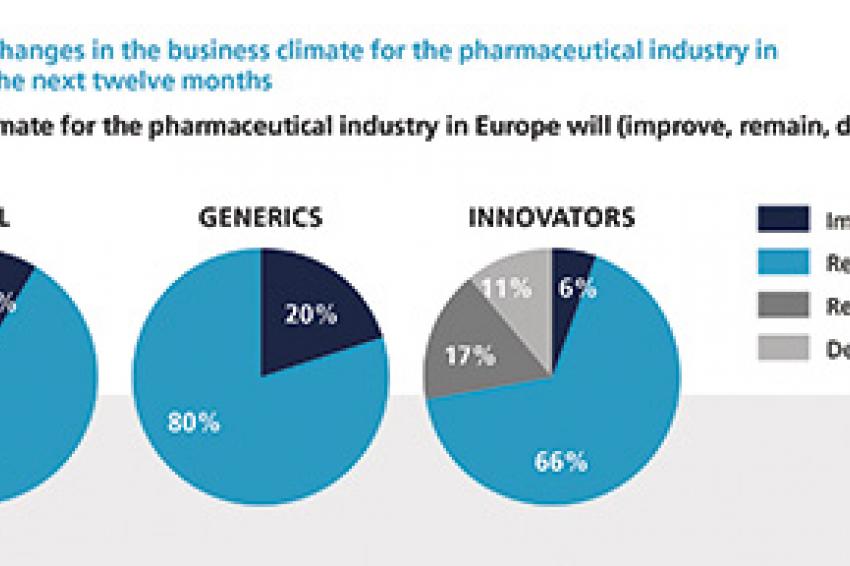

The executives' view of the business climate for the pharmaceutical industry has essentially remained as positive as it had been in the Pharma Management Radar Survey conducted one year earlier. This particularly applies to the Generics executives, all of whom rate the business climate as "good" or at least "mostly good," whereas the share of pessimistic Innovators has slightly increased year-over-year.

These mood differences are also reflected in the outlook on the economic developments during the next 12 months: While all participating Generics are optimistic, more than one in four Innovators fear that the business climate will "remain just as bad" or "deteriorate." This type of pessimism has gained relevance over the last 12 months, which might be seen as a sign of still-growing competitive pressure on some Innovators due to expiring patents and increasing regulatory requirements.

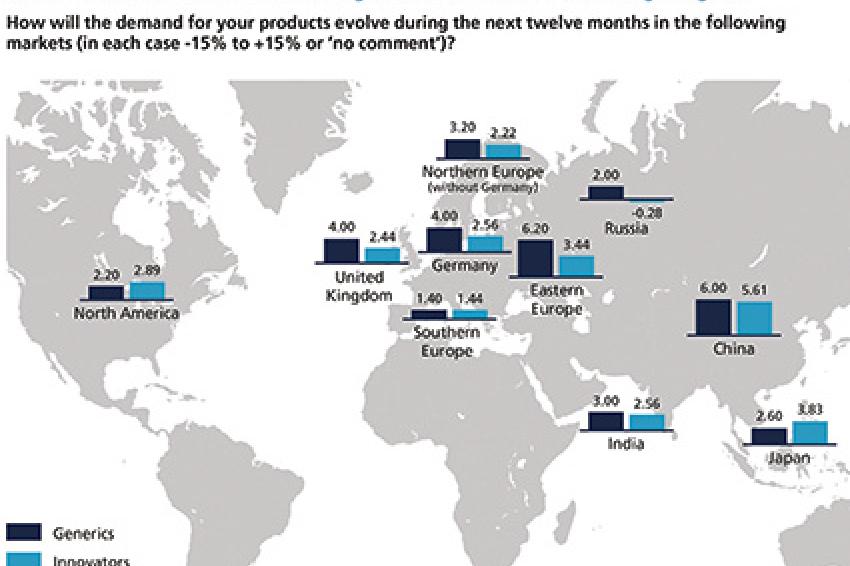

In accordance with their general industry outlook, most respondents are optimistic with regard to their own business development. More than 90% expect their sales performance to improve while 96% are confident of being able to raise EBIT (earnings before interest and taxes) in 2015. When it comes to where this growth is expected, both the European debt crisis and the military conflict in the Ukraine are clearly reflected in the pharmaceutical industry's demand expectations: Russia and Southern Europe perform extremely poorly in this respect. In contrast, expectations have further brightened up for various emerging markets - especially China and Eastern Europe. In the mature markets of Germany and the UK, the Generics see a considerably better perspective for themselves than the Innovators, which may be due to the rising cost pressure in these countries' health-care systems.

These expectations are also reflected in many of the pharmaceutical industry's regional investment plans for the next 12 months. China is clearly considered the most important market while Russia has dropped dramatically in terms of investment attractiveness (from 50% to 17%) since last year. For Southern Europe, the situation looks equally bad - it has not improved during the last 12 months.

Quite interestingly, the will to invest and the general economic optimism are not accompanied by growth in employment figures. On the contrary, nearly half of all respondents are planning to decrease their number of employees, and a third expect their staff to remain constant. One year earlier, more than a third of respondents had been willing to increase employment figures. As a logical consequence of the cautious employment strategies, the external sourcing trend remains on a very high level, with more than two-thirds of respondents planning to make use of external support during the next 12 months. Just like in 2014, this trend is particularly strong in the Generics segment, where none of the respondents has plans to decrease external outsourcing in 2015.

As far as the greatest risks for the companies' business development during the next 12 months are concerned, price decrease due to patent expiry has climbed from the fourth position to the top risk since last year. In addition, more than 40% of respondents are nervous about political risks in growth markets, which is of course due to the political and economic developments in Russia/Ukraine, Southern Europe and other emerging markets.

Given these problems, it is not surprising that more than half of respondents consider cost reduction the most important industry trend. Securing supply reliability, which is vital for business success, is the second top trend while the continuing trend toward outsourcing is also reflected in this ranking. Another measure to cope with increasing competitive pressure is the creation of additional revenue sources. Subsumed under the term "beyond the pill," these services do not yet belong to the top priority trends for the next 12 months in logistics, but they are considered a priority trend with an interesting perspective for the medium-term future.

Service-Related Trends to Become More Important

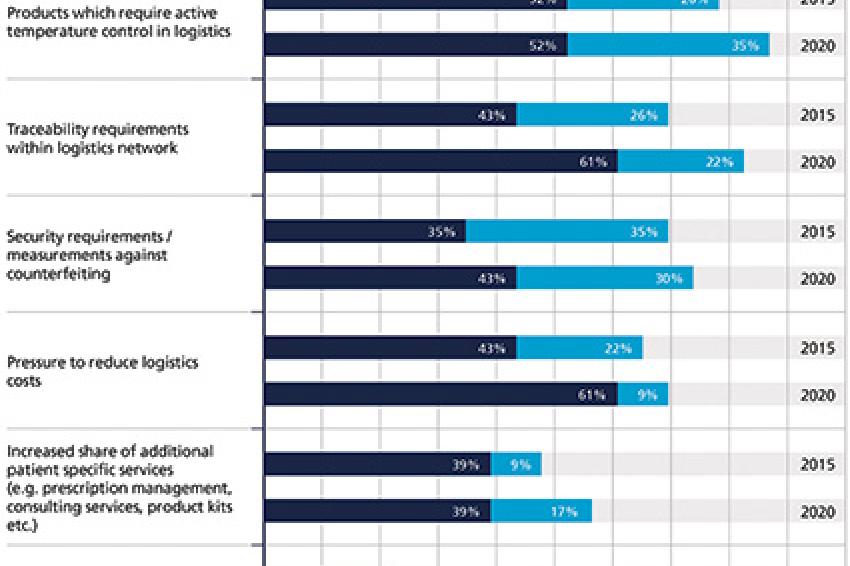

When asked about market trends influencing logistics organization and setup, the majority of respondents see increased challenges in products requiring active temperature control and traceability both in 2015 and during the next three to five years. Security requirements and measurements against counterfeiting as well as pressure to reduce logistics costs are also expected to become more important or even significantly more important both with regard to the near- and the medium-term future. Some considerable movement can be observed, however, when it comes to service-related trends. The relevance of additional patient-specific services such as prescription management, consulting services, product kits, as well as the importance of home-care services, is expected to be much higher by 2020 than during the next year.

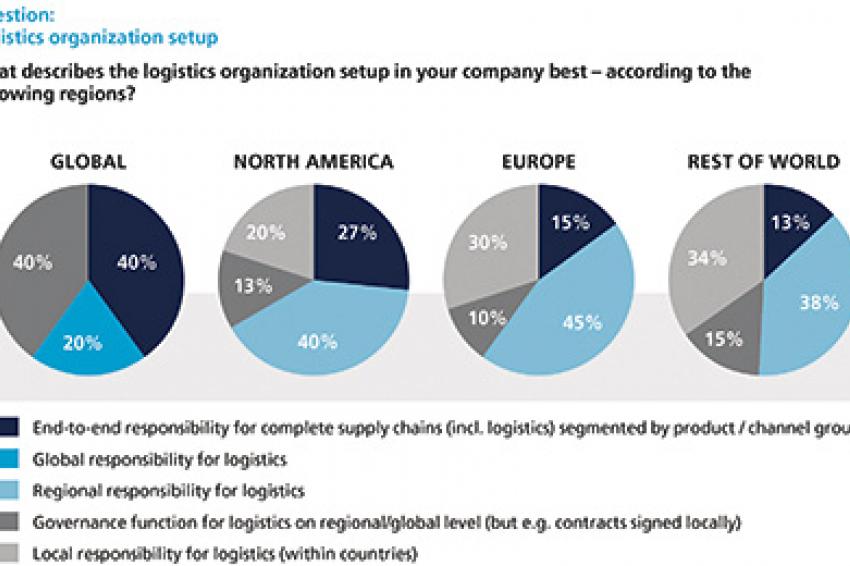

One trend to be observed within pharma logistics is the move toward regional logistics organization - especially with regard to Europe, where this was the top answer. Generally, however, the traditional model of local logistics organization still plays a major role, while the opposite concepts, i.e., global responsibility for logistics or an end-to-end responsibility for complete supply chains segmented by product/channel groups, are applied rather seldom.

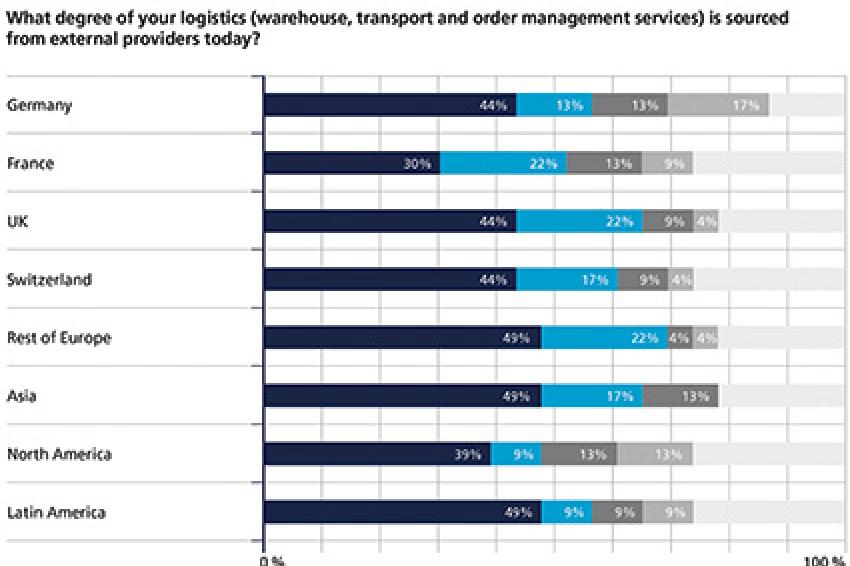

In accordance with the general sourcing trends, external support has become a matter of course with regard to logistics as well. For nearly all regions of the world, at least four in 10 respondents say that they have outsourced the biggest share (more than 75%) of their warehouse, transport and order-management services. When extending the scope to the year 2020, the respondents do not leave any doubt that the outsourcing trend in logistics will continue. As main drivers for this development, most respondents name the avoidance of investments into low value-added services in order to concentrate on their core business. While for the Generics mere financial considerations also play a very important role for logistics outsourcing, other major drivers for the Innovators are the qualification and specialization of service providers and the flexibility they offer.

Given the expectation that pharmaceutical companies, especially Innovators, will increasingly offer additional services in the medium-term future, logistics strategies will have to align closer with manufacturing and commercial strategies. So far, however, little more than 10% of respondents have a regular process with clear global roles and responsibilities in place when it comes to the alignment between logistics distribution strategy and manufacturing strategy. Regarding the integration with commercial strategy, there is even more room for optimization.

It seems, however, that this problem has been realized, as intra-company collaboration is widely considered a subject for logistics focus initiatives in the next two or three years. The survey found that at the moment, there is a lot of movement in other areas of pharma logistics: Approximately two-thirds of the respondents have currently ongoing initiatives to change logistics organization and process setup - which again indicates a possible move away from a strictly local setup to a more regional or even global logistics focus.

Please register here to participate in the next Pharma Management Radar survey!

Order free copies of Camelot's studies on the global pharmaceutical industry!

Contact

Camelot Management Consultants AG

Theodor-Heuss-Anlage 12

68165 Mannheim

+49 621 86298 0

+49 621 86298 250