Eastman Announces Second-Quarter 2012 Financial Results

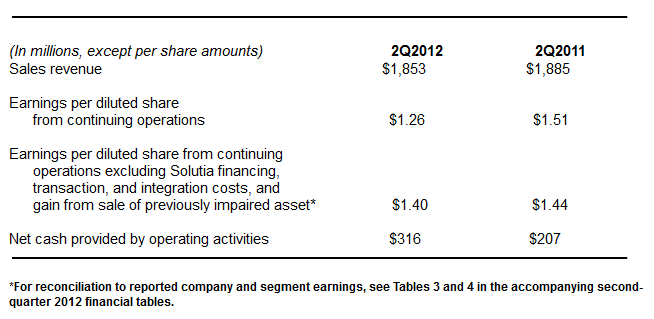

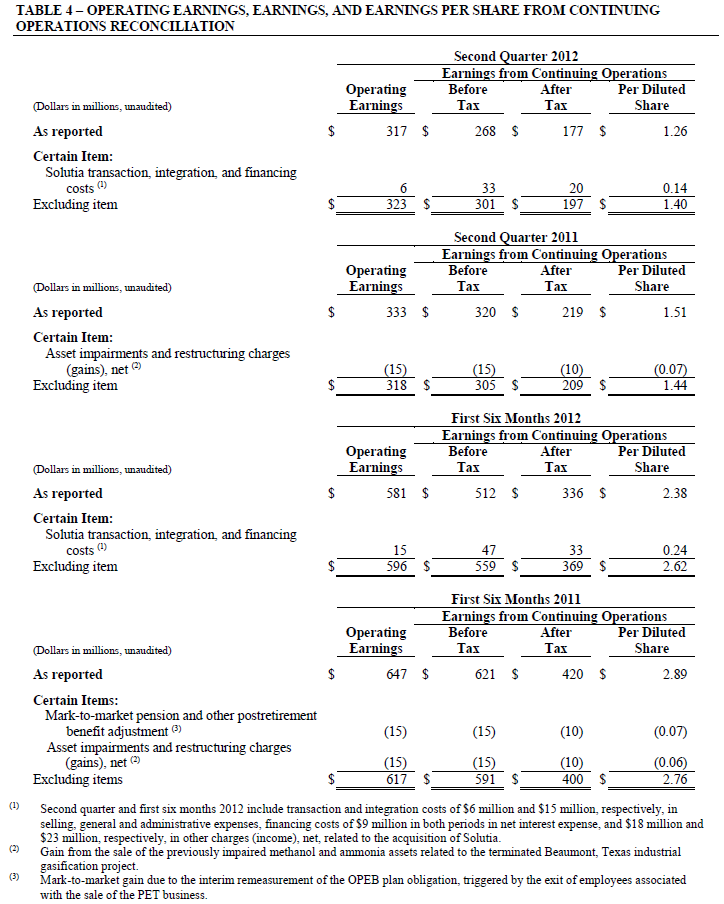

Eastman Chemical Company today announced earnings from continuing operations of $1.40 per diluted share for second quarter 2012 versus $1.44 per diluted share for second quarter 2011, excluding $33 million of financing, transaction and integration costs in second quarter 2012 related to the acquisition of Solutia and a $15 million gain in second quarter 2011 from the sale of a previously impaired asset. Reported earnings from continuing operations were $1.26 per diluted share in second quarter 2012 and $1.51 per diluted share in second quarter 2011.

"This is an exciting time for Eastman with continued strong earnings performance throughout the company and the recent completion of the Solutia acquisition," said Jim Rogers, Chairman and CEO. "The integration of Solutia is well underway and our capture of cost synergies is on plan such that we are poised to deliver earnings growth and generate significant cash for years to come."

Sales revenue for second quarter 2012 was $1.9 billion, a 2 % decline compared with second quarter 2011.

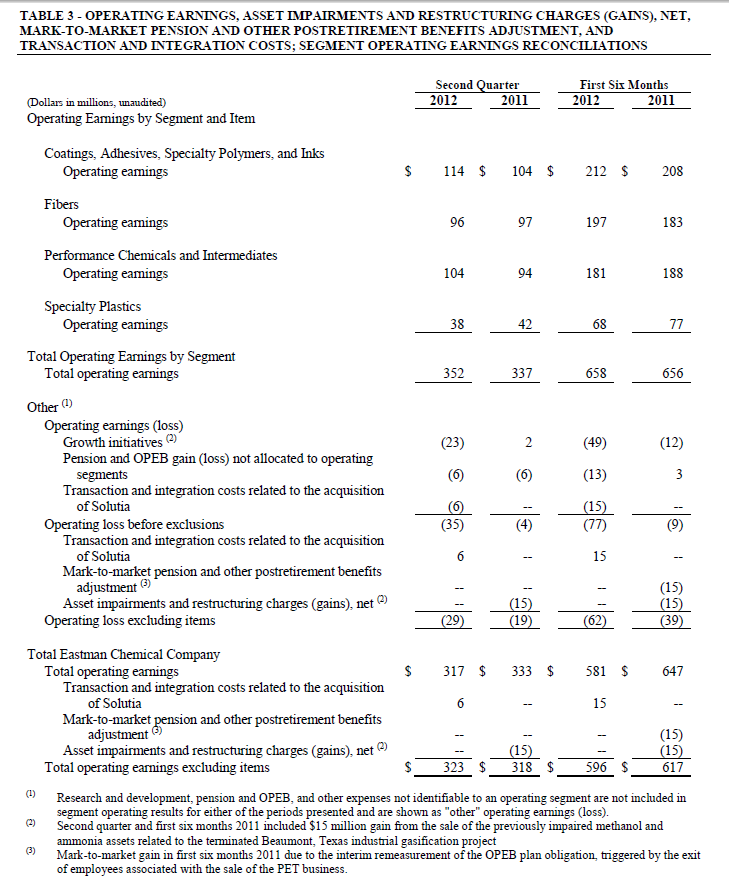

Operating earnings in second quarter 2012 were $317 million compared to $333 million in second quarter 2011. Excluding transaction and integration costs related to the Solutia acquisition in second quarter 2012 and a gain from the sale of a previously impaired asset in second quarter 2011, operating earnings were $323 million and $318 million, respectively.

Segment Results 2Q 2012 versus 2Q 2011

Coatings, Adhesives, Specialty Polymers and Inks - Sales revenue declined slightly in second quarter 2012 compared with second quarter 2011. Operating earnings in second quarter 2012 increased to $114 million compared with operating earnings of $104 million in second quarter 2011. The increase was primarily due to lower raw material and energy costs more than offsetting slightly lower selling prices.

Fibers - Sales revenue declined by 4 % due to an unfavorable shift in product mix that was partially offset by higher selling prices. The unfavorable shift in product mix was primarily due to lower acetate tow volume in Asia Pacific attributed to customer buying patterns. The higher selling prices were in response to higher raw material and energy costs, particularly for wood pulp. Operating earnings in second quarter 2012 were $96 million compared with $97 million in second quarter 2011, with the slight decline due to the unfavorable shift in product mix mostly offset by higher selling prices.

Performance Chemicals and Intermediates - Sales revenue was unchanged in second quarter 2012 compared with second quarter 2011 as higher sales volume and a favorable shift in product mix were offset by lower selling prices. The higher sales volume and favorable shift in product mix were primarily due to increased sales volume for acetyl product lines in the U.S. and the favorable impact of the acquired Sterling and Scandiflex businesses. The lower selling prices, primarily in olefin derivative product lines, were in response to lower raw material and energy costs. Operating earnings in second quarter 2012 increased to $104 million compared to $94 million in second quarter 2011. The increase was due primarily to lower raw material and energy costs and the benefit of producing versus purchasing olefins, partially offset by lower selling prices.

Specialty Plastics - Sales revenue declined by 6 % in second quarter 2012 compared to second quarter 2011 primarily due to lower sales volume partially offset by a favorable shift in product mix and higher selling prices. The decrease in sales volume, mainly in the U.S. and Europe, was attributed to weakened demand for copolyester product lines primarily in the consumer and durable goods markets. The favorable shift in product mix was due to higher sales volume into the LCD market for cellulosic product lines. Second-quarter 2012 operating earnings were $38 million compared to $42 million in second quarter 2011. The decline was primarily due to lower sales volume and resulting lower capacity utilization, which was partially offset by the favorable shift in product mix and higher selling prices.

Cash Flow and Financing

Eastman generated $316 million in cash from operating activities during second quarter 2012, primarily due to strong net earnings. As part of the financing of the July 2, 2012 acquisition of Solutia Inc. and of repayment of certain Solutia borrowings, on June 5, 2012 Eastman received $2.3 billion net proceeds from the public offering of notes due 2017, 2022, and 2042 and on July 2, 2012 borrowed $1.2 billion under a five-year term loan agreement.

Solutia Acquisition and 2Q12 Results

On July 2, 2012 Eastman completed the acquisition of Solutia Inc. With the acquisition, the company made structural and reporting changes resulting in five reporting segments: Additives and Functional Products, Adhesives and Plasticizers, Advanced Materials, Fibers, and Specialty Fluids and Intermediates. The company will report third quarter 2012 financial results under the new reporting structure.

Sales revenue for Solutia in second quarter 2012 was $520 million, a 4 % decline compared with second quarter 2011, due primarily to the strengthening of the U.S. dollar versus the euro. In addition, slightly higher sales volume in the Technical Specialties and Performance Films segments was more than offset by lower sales volume in the Advanced Interlayers segment. Net income was $31 million in second quarter 2012 including $15 million of acquisition related expenses, and $68 million in second quarter 2011 including $1 million of other charges. Adjusted EBITDA (as defined in Appendix A) declined to $115 million in second quarter 2012 compared with $141 million in second quarter 2011. The decline in adjusted EBTIDA, primarily in the Advanced Interlayers segment, was mainly due to lower sales volume in Europe for Saflex product lines, lower sales volume for photovoltaic encapsulants product lines, and costs of growth initiatives.

Outlook

Commenting on the outlook for full year 2012, Rogers said: "Despite persistent global economic uncertainty, we continue to expect double-digit year-over-year earnings growth resulting from the solid performance of heritage Eastman businesses and second half earnings from the acquired Solutia businesses. As a result, our expectations for 2012 EPS of $5.30 remain unchanged." Costs and charges related to the Solutia acquisition, including financing, transaction, and integration costs, asset impairments and restructuring charges, net, and mark-to-market pension and OPEB adjustments are excluded from the earnings per share projection.

most read

VCI Welcomes US-EU Customs Deal

The German Chemical Industry Association (VCI) welcomes the fact that Ursula von der Leyen, President of the European Commission, and US President Donald Trump have averted the danger of a trade war for the time being.

CHEManager International Media Kit 2026

Compelling solutions through strategic partnerships

Orion Announced Plans to Shut Down Carbon Black Plants

Carbon black manufacturer Orion Engineered Carbons plans to rationalize production lines in North and South America and EMEA.

Novo Nordisk to Cut 9,000 Jobs Globally in Major Restructuring

Novo Nordisk announced a global workforce reduction of approximately 9,000 positions to streamline operations and reinvest DKK 8 billion (€1 billion) in growth opportunities for diabetes and obesity treatments.