Finding the Right Emerging Markets for Growth

A Pragmatic Approach to Explore the Economic Attractiveness, Ease of Access and Strategic Market Size of Potential New Markets

-

Finding the Right Emerging Markets for Growth (c) Tatiana Popova/Shutterstock

Finding the Right Emerging Markets for Growth (c) Tatiana Popova/Shutterstock -

Tobias Lewe, A.T. Kearney

Tobias Lewe, A.T. Kearney -

Otto Schulz, A.T. Kearney

Otto Schulz, A.T. Kearney -

Robert Renard, A.T. Kearney

Robert Renard, A.T. Kearney -

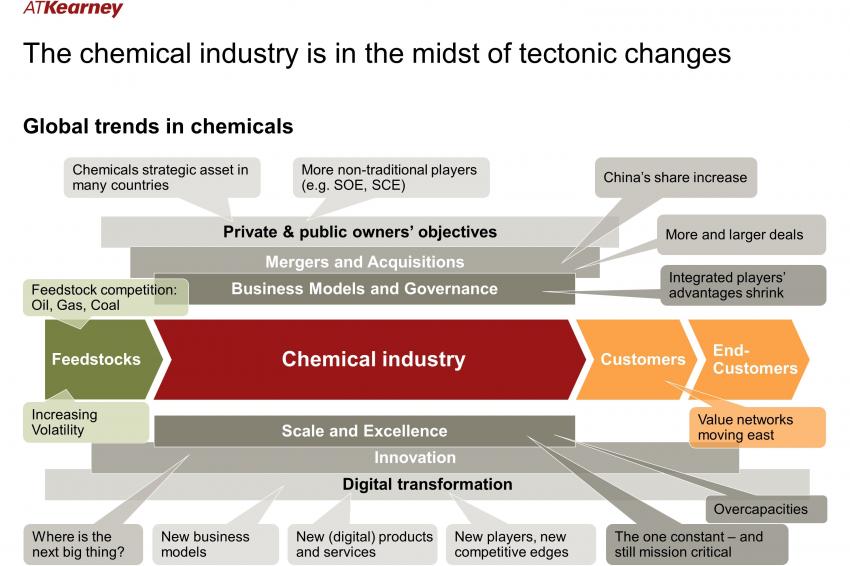

Fig. 1: Global trends in the chemicals industry

Fig. 1: Global trends in the chemicals industry -

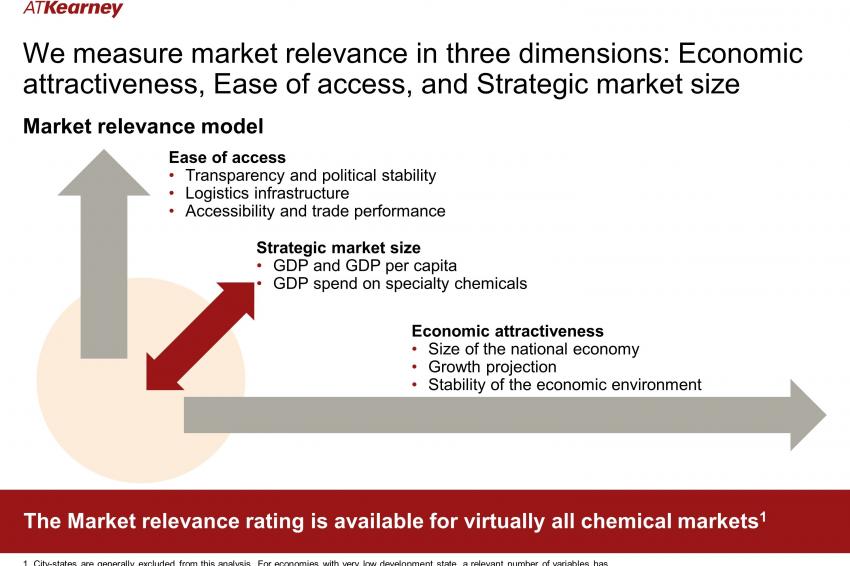

Fig. 2: A.T. Kearney’s market relevance model

Fig. 2: A.T. Kearney’s market relevance model -

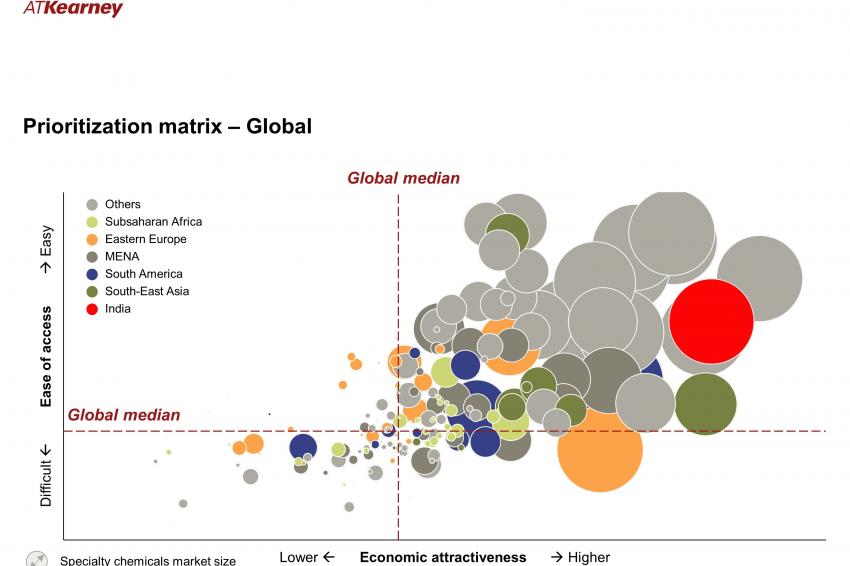

Fig. 3: A.T. Kearney’s prioritization matrix

Fig. 3: A.T. Kearney’s prioritization matrix

In the past, much of the attractive growth for specialty chemicals companies came from China and the rebound of the US economy. In the future, companies need to consider a portfolio of emerging markets even more, despite the risk of market instability and the difficulty of projecting short-term growth in those markets. We suggest a pragmatic approach that explores the economic attractiveness, ease of access and strategic market size of potential new markets and allows companies to quickly create a shortlist for investment opportunities that fits their risk profile.

Specialty chemicals companies in Europe and other established markets face difficulties growing in home markets, beyond what can be achieved through GDP growth and small gains in market share.

Overall, the specialty chemicals market is set to grow 3.5% per year, but the higher growth will likely come from emerging economies, where traditional western players may not have strong footprints. Some companies will find growth opportunities from the manufacturing rebound in the United States, and most companies have developed a strategy and channels for operating in China.

However, to take advantage of more substantial growth, many companies will choose to expand more in emerging economies. Some recent examples are opportunities to sell electronics chemicals in Thailand, construction chemicals in the Middle East or textile chemicals in Turkey. Value chains will likely continue to move eastward, and their control points will increasingly become local in these countries. But finding the right approach for the next steps is often a challenge, because it is difficult to compare opportunities and risks in markets like India, Brazil and selected southeast Asian or southeastern European countries.

No matter which corner of the globe your company is tackling, we urge you to start early with a pragmatic approach to finding the right strategy. Companies should expect challenges getting that strategy in place, given the diversity and complexity of these markets. But the first step – creating a shortlist of targets – can be a relatively simple exercise.

We realize that in many cases, international expansion takes a backseat to other management priorities, and this is one reason a simple but data-driven approach is useful in the first step.

It can help busy executives set priorities with confidence and act more quickly in the face of disruptive changes in traditional markets. These include increasing administrative and environmental regulation, digitization of value chains, the electrification of automotive, and recent M&A. There’s also pressure to create solutions that go beyond products, as well as uncertainty from China-US trade tensions, to name a few points.

A.T. Kearney’s 2018 Foreign Direct Investment Confidence Index indicates that investors are uncertain about where to invest – beyond the largest, most obvious locations with the lowest perceived risks – even as they plan to increase their level of FDI. However, companies in developed markets can achieve attractive revenue growth over the mid-term in specific countries outside their home turf.

Finding a Pragmatic Approach to Investing in Emerging Markets

Before getting started, it’s critical to understand that companies eventually need their own assessments of the local industry and their own value propositions for target countries.

But there is a long list of emerging markets that offer potentially attractive opportunities and screening them is time and resource consuming. So, a methodology is needed that reduces the long list in a pragmatic way. As we like to say, just because a country’s economy is growing, that doesn’t make it a good place to invest.

This idea – that GDP growth doesn’t tell the whole story – is an integral part of our approach to evaluating emerging market opportunities and creating heat maps.

We have worked to make our approach objective, data-driven and transparent. It measures economic attractiveness, ease of access and strategic market size, through short and medium-term indicators.

For instance, for economic attractiveness, we recommend looking at the size of the national economy, growth projections, and stability of the economic environment. For ease of access, we look at: transparency, political stability, logistics infrastructure, accessibility and trade performance.

For strategic market size, we calculate a figure that is a “proxy” for local chemical consumption, given the possibility of inconsistent data from heterogeneous and complex specialty chemicals markets.

When thinking about the starting point for the strategy, it is the mix of country-specific and company-specific questions that matters. With a structured approach, we can define a robust starting point for discussions with business leaders.

Questions to ask include: Which of your products and services fit best with local value chains, which competitive or complementary industry exists locally, and what is your company’s own capacity for growth? Also, what is the local, country- or hub-specific supply and demand in the industry – e.g. where would additional volume help, and where would it create unnecessary trade-offs with existing business?

Country-specific questions include the size of an economy and its growth rates, but also how relevant and sustainable is the GDP for your business intent?

For instance, does GDP per capita indicate sufficient wealth in the country for a relevant share of the population to buy processed products on a regular basis – everything from fertilizers to consumer-packaged goods and durable household equipment? Are the government’s investments in industrialization and human capital sufficient? How will demographics impact the opportunity?

The ability to get goods into the country and revenue out of the country are equally important factors to consider about a target market. This is impacted by infrastructure, the effectiveness of public administration, and integration of the economy into the global financial system.

In the end, companies need to understand the data that drive results in the model. Not all data points will exist for all countries. In many cases, country-level data is combined under the category “Rest of World.” But it is possible to use available data to significantly reduce the scope for a detailed strategic analysis in a data-driven model.

In short, companies looking to build up a chemicals value chain in a new market need a quick, accurate and data-driven way to narrow the list down to those countries that offer a strategic fit and growth potential that is built on solid footing.

How One Company Approached Its Analysis

For one client, we examined their portfolio and mapped it to the producing industries in target countries. For its business producing food and animal feed, we considered the size and development of the agricultural sector in target countries and the consumption of specialty meats.

We created a footprint for the client’s business and for the target countries, and then saw where they overlapped. In the end, we were able to reduce a long list of potential markets to six countries. The process confirmed some of the “obvious” candidates but some countries on the shortlist might not have been considered with the same intensity without the analysis.

Amidst all the changes going on in the chemicals industry, and the risk of competitors gaining increased market share or key partnerships in your target countries, a data-driven, objective analysis to quickly find opportunities for growth in emerging markets can give you confidence that no opportunities have been overlooked.

It will also help you be prepared for discussions within your own organization with business units that are ready and waiting to argue why their current region-focused investment plan is the right one.

With Priorities Set, What Is Next?

We acknowledge that this methodology delivers the starting point to capturing additional growth opportunities and not the complete strategy. But it gives the right focus for defining the next steps, including building a commercial and supply chain model for the opportunities. Companies may also answer questions like what are the right channels, or where can additional demand be found in the global network?

By examining these questions, companies can reap additional benefits besides prioritization. For example, they may learn more about when a group of emerging countries could be served from one hub, or how synergy with an existing partner could lead to a local joint venture.

A robust model also gives an initial idea of the size of the opportunity. We have seen that this focused starting point, together with having a target to reach, helps get the growth strategy onto the management agenda.

Foreign Direct Investment Confidence Index

A.T. Kearney’s 2018 Foreign Direct Investment (FDI) Confidence Index illustrates three trends: Trend 1: The United States has topped the list of FDI recipients for six years and many European countries continue to attract significant investment. Executives are clearly focused on established markets, and companies must continue to consider where their competitors and customers are. Trend 2: Companies need more localization due to the increasing complexities of delivering customer-centric solutions locally, with a global supply and delivery network. At the same time, 80% of investors expect FDI to impact their profitability and competitiveness substantially. Trend 3: We see only four emerging economies in the list of top 25 FDI destinations: China, India, Mexico and Brazil. This is fewer than ever before in the index. The data shows limited action of companies to expand their local activities in many attractive markets. Nonetheless, 44% of respondents reported they are seeking to increase their investments in emerging markets.