Fine Chemicals: The Top 10

Analysis - When comparing the fine chemicals market of today to that of 2001, a few clear differences can be seen. Fine chemicals expert Jan Ramakers takes an in-depth look at the top players today.

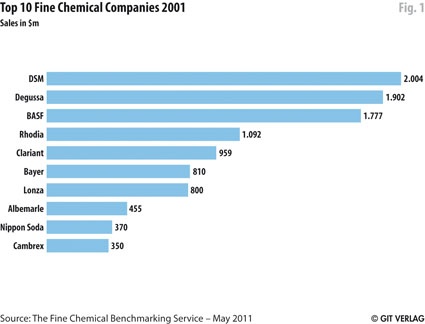

Back in 2001, the three largest producers, DSM, Degussa, and BASF were very close to each other, each of them having fine chemical sales in the $1.8-2.0 billion range. Also in that year, the top five companies had a combined market share of 12.3%; the combined market share of the top 10 was 16.7%.

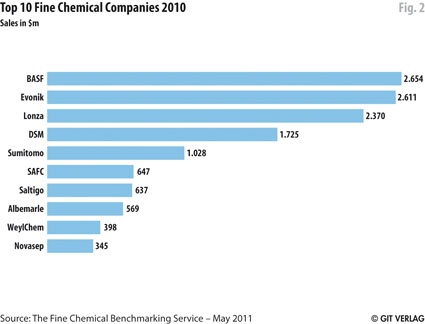

Looking at the current situation, the first impression is that the industry is more concentrated than it was 10 years ago. However, a closer look shows that this is not the case. In 2010, the market share of the leading company was 2.8%, whereas in 2001 the market share of the leading company was 3.5%.

The top five had a combined market share of 10.8%, which is less than the 12.3% they had in 2001. Also, the combined market share of the top 10 in 2010 was 13.5%, down from 16.7% in 2001 and only slightly higher than the top five 10 years ago.

So, the net result of all the mergers, acquisitions, spin-offs and divestments of the last 10 years has not increased the degree of concentration of the fine chemical industry at all. On the contrary, instead of being more concentrated, the fine chemical industry is more fragmented now than it a decade ago.

A Closer Look at the Top 10 in 2010

1. BASF

As the leading fine chemical producer in 2010, Germany's BASF also happens to be the largest chemical company in the world with production sites in 41 countries and some 109,000 employees. The product portfolio of the company includes chemicals, plastics, performance products, agricultural products and fine chemicals, as well as crude oil and natural gas. Following the acquisition of Ciba in 2009, the company acquired Cognis in 2010. Neither of those acquisitions have a direct impact on the fine chemicals business of the company.

2. Evonik

Evonik's fine chemicals business is part of its Chemicals business area, which formerly traded as Degussa. Its fine chemical operation mainly revolves around the custom manufacturing business. In the course of 2011, Evonik started divesting its non-chemical businesses (Real Estate and Energy). According to the company, its Real Estate business will be "placed on a more independent basis in the medium term." In the first quarter of 2011, the company sold 51% of the shares of its Energy business to a consortium of municipal utilities in Gernany's Rhine-Ruhr region. The remaining stake is to be sold within five years.

3. Lonza

Lonza has always viewed fine chemicals as its core business. At the end of 2006, the company divested its polymer intermediates business, and since then almost all of its revenues have been generated from fine chemicals. In recent years, Lonza has invested heavily in strengthening its position in the biotechnology area.

Biotech manufacturing facilities were built and/or expanded at the Visp, Switzerland, and Slough, UK, sites in 2004 and 2005, followed by a large number of acquisitions and investments in the biotech area, including: UCB Bioproducts, Cambrex's Bioproducts and Biopharma segments; Genentech's mid-scale mammalian biopharmaceutical production plant in Spain; large-scale commercial mammalian cell culture manufacturing facilities in Singapore; a large scale production plant for antibody drug conjugates; and some others. With that, Lonza has positioned itself as a leading player in the biotech/biologicals area.

In 2008, it entered into a partnership with Novartis for the development and manufacture of its biological pipeline, and into a joint venture with Teva, one of the largest generics companies for the manufacture of biosimilars.

In the course of 2010, the company streamlined its organization. It also signed co-operation agreements with Dalton Pharma Services (Canada) and California Peptide Research (U.S.). In early 2011, it announced investments to further expand its biopharmaceutical capacity as well as its capacity to produce high potency APIs (HPAPIs).

4. DSM

DSM, the leading fine chemical company in 2001, has streamlined its fine chemical portfolio over the past few years, which included some divestments and site closures in the pharma area in 2004-2006. One of the major reasons for this was the extremely competitive situation that developed in the market for semi-synthetic antibiotics, mainly from Asian producers, which had a heavy impact on DSM's business in that segment.

In 2007, the company decided to focus more on life and material sciences; it has since divested several of its commodity chemicals businesses and closed down or divested some smaller fine chemical manufacturing operations. The divestment of its elastomers business in early May 2011 completed the transformation of the company. To mark this milestone the company redesigned its house style, including a new logo.

5. Sumitomo Fine Chemicals

The Sumitomo Chemical Group includes around 100 companies around the world, with activities in fine chemicals, basic chemicals, petrochemicals, plastics, agrochemicals, pharmaceuticals and IT-related chemicals.

Sumitomo Fine Chemicals, the highest ranking Japanese producer of fine chemicals, merged with the fully owned Sumitomo subsidiary Sumika Fine Chemicals in 2003. After that no other major acquisitions were made.

Sumitomo also has a majority share in Koei Chemical, another Japanese producer of fine chemicals.

6. SAFC

SAFC, the fine chemicals business of Sigma-Aldrich, has a clear focus on the pharmaceutical market. The company has shown a rapid growth to its current sales level over the past few years, largely as a result of a large number of acquisitions, mainly in the biotech and high potency area.

In late 2010, the company completed the expansion of its Jerusalem, Israel, facility. The additional capacity expands SAFC's contract manufacturing capabilities in large molecule recombinant proteins and small molecule APIs through fermentation, including HPAPIs and secondary metabolites.

7. Saltigo

Saltigo, formerly the fine chemical business of Bayer, has certainly benefitted from its independence, as well as the subsequent realignments.

In May 2010, Saltigo entered into a cooperation agreement with Syngenta, a leading agrochemical company. Syngenta is investing some €50 million in expanding several Saltigo facilities in Leverkusen, Germany, to significantly enhance its capacity for manufacturing active agrochemical ingredients. Saltigo supplies the active ingredients and intermediates produced in those facilities exclusively to Syngenta.

8. Albermarle

Albemarle showed good growth in the first few years after 2001, partly fuelled by the acquisition of DSM Pharmaceutical Products' generic API business that was operated out of South Haven, U.S., in 2006. After that, growth stalled for a while but recently Albemarle's fine chemicals business is showing signs of improvement.

9. WeylChem

WeylChem was formed in 2005, when International Chemical Investors Group (ICIG) of Germany acquired part of Rütgers. The deal included the pharma fine chemicals business of Mannheim-based Rütgers Organics and its U.S. affiliate, which specialised mainly in agrochemicals. Since its formation, the company acquired a number of other businesses, including Albemarle's Thann, France, facility; the Cork, Ireland, and Landen, Belgium facilities of Cambrex; Clariant's custom manufacturing business; and Miteni.

In 2010, the company acquired DyStar's production site in Brunsbüttel, Germany from Chemie Bitterfeld Wolfen. WeyChem and CBW are planning to use the site in the future as a mutual production platform. With the new facilities, WeylChem intends to add phosgenations to its technology portfolio. For that, the phosgenation capacity in Brunsbüttel will be expanded.

10. Groupe Novasep

Last but not least, the number 10 on the list is Groupe Novasep. The company is organized in two strategic business units: Novasep Process (focused on purification engineering) and Novasep Synthesis (focused on chemical and biochemical synthesis)

Novasep uses the combined strength of the business units to manufacture advanced intermediates and APIs for custom manufacturing services to the pharma industry and other fine chemical industries. Séripharm, part of Novasep Synthesis, is involved in the manufacture of highly potent compounds. In 2009, the company acquired Henogen (Brussels, Belgium), a contract manufacturing organization offering bioprocess development and manufacturing services ranging from cell bank to supply of clinical products.

Trends In The Market

Fine chemicals are used in a wide variety of applications, and it is not too difficult to make a list of 40-50 market segments. The products are used as active ingredients in biocides, cosmetics and toiletries, as additives for plastics and coatings, etc. Larger markets for fine chemicals include agrochemicals, flavors and fragrances, and dyes.

The pharmaceutical industry has been the main market for fine chemicals for many years. As a result of the fact that the average annual growth of pharma has always been significantly higher than the average annual growth of any other fine chemical market, the relative importance of pharma for fine chemicals has increased. In 2010, the pharma segment was responsible for 68% of the fine chemical market, up from 54% in 1999. Given the current growth rates of the various fine chemical market segments it is anticipated that pharma will be some 71% of the market in 2015.

Because of the dominance of pharma in fine chemicals, the main drivers for the fine chemical market are the trends and developments in the pharma market, including

- The markets for HPAPIs and biopharmaceuticals are growing at rates above the average pharma growth rate, and it is anticipated that between them these markets will be responsible for some 30% of the pharma market in 2015

- The market for biopharmaceuticals is growing at rates above the average pharma growth rate

- Increasing market share of generics

- Increasing cost and regulatory pressure

- Increase in pharma outsourcing

Profitability

Although R&D-related pharma business was affected the overall pharma market continued to grow during the global economic downturn and in spite of adverse market conditions in many other fine chemical market segments the total market for fine chemicals continued to grow. Profitability levels dropped off significantly though. In 2009 close to 50% of the top 40 fine chemical producers had an operating profit of less than 5% of fine chemical sales, or suffered an operating loss; more than two thirds of the top 40 had an operating profit of less than 10% of sales.

In 2010 profitability levels improved, with 37% of the top 40 generating an operating result of 5% of sales or less, and 59% generating an operating result of 10% or less. Going forward it is expected that profitability levels will gradually return to more normal levels.