Going Inland

Historically, China’s chemical industry has mainly been located in coastal provinces, with Shandong as the biggest and Jiangsu as the second biggest province by chemical sales, while the coastal regions of Hebei, Tianjin, Zhejiang, Liaoning and Guangdong are also among the top ten producers of chemicals.

Historically, China’s chemical industry has mainly been located in coastal provinces, with Shandong as the biggest and Jiangsu as the second biggest province by chemical sales, while the coastal regions of Hebei, Tianjin, Zhejiang, Liaoning and Guangdong are also among the top ten producers of chemicals. This concentration is partly a consequence of the high population density and subsequent central role in industrial production of these provinces. Coastal provinces are also obviously favored as locations targeting overseas exports of chemicals and more importantly the end products produced from these chemicals within China.

In the past few years, however, the situation has changed to some extent. Comparatively rich areas such as Jiangsu or Shanghai have encountered limits regarding available space. These provinces also face rising concerns both from an increasingly environmentally conscious middle class and from government officials worried about accidents, threatening their careers — such as the March 2019 explosion at a chemical plant in Jiangsu Province which killed 78 people. At the same time, these locations have various alternatives regarding interested industrial investors, many of which are regarded both as less risky and providing more jobs of a higher quality.

Environmental legislation has also had a strong impact on the chemical industry, particularly in the coastal provinces. The mandatory shift to chemical parks — along with often strict acceptance criteria these parks impose on new tenants — has forced many small companies to close down their production in these provinces. The legislation enacted to protect the Yangtze river (the „Action Plan for In-depth Protection and Restoration of the Yangtze River,“ which prohibits chemical production within one kilometer of the river and its main tributaries) has led to further closures and also limited the area available for the settlement of chemical companies.

In Shandong, for example, the number of chemical parks was reduced from 199 to 84 within a period of five years, and more than 2,000 chemical companies were closed. In Jiangsu, after five years of intensified regulation of chemical companies, there are now only fewer than 1,000 chemical companies, down from more than 4,000 in 2015 and more than 3,000 in 2019. Several chemical parks in Jiangsu were closed as well. Other provinces including Hubei, Guangdong and Henan have also issued policies restricting chemical production.

Depending on their size, investment capital and profitability, affected chemical companies have reacted in different ways. Small, low-technology companies have mostly simply closed, a consequence that was probably quite intentional on the part of provincial governments, since these enterprises contribute relatively little to the economy while contributing disproportionately to the risks of chemical production.

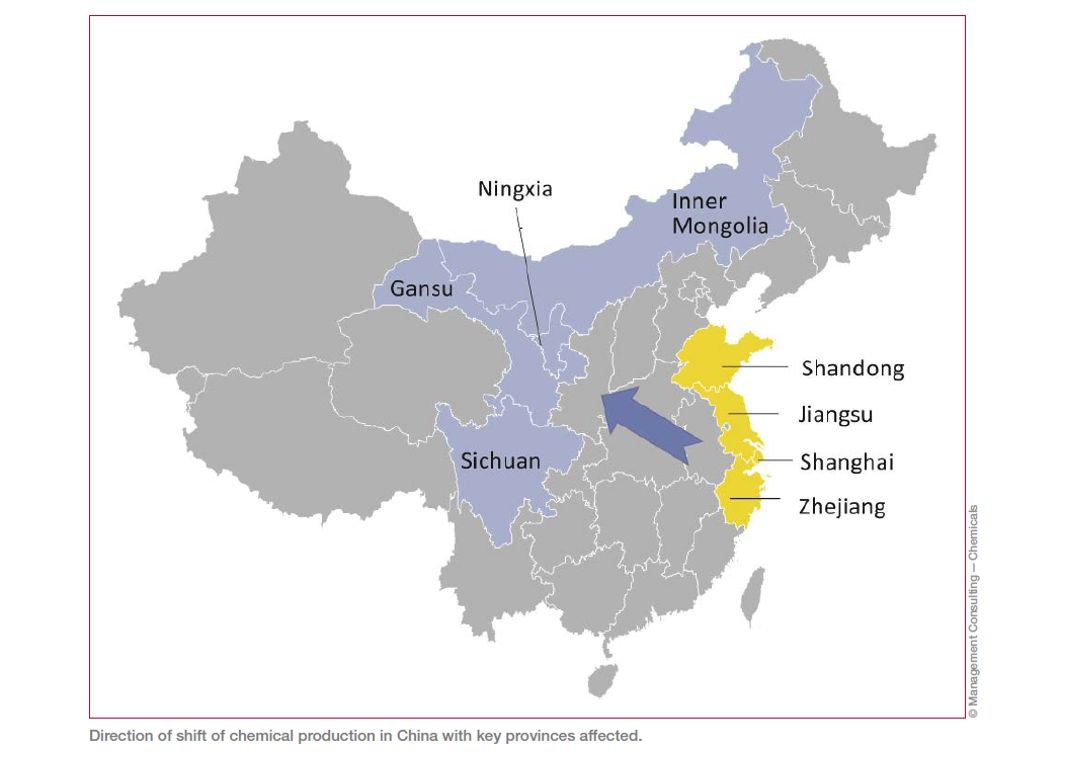

However, several larger domestic companies have relocated production to provinces which are perceived to have less stringent criteria. For example, several pesticide producers from Jiangsu province have moved parts of their production to inland provinces, such as Inner Mongolia, Gansu, Ningxia and Sichuan, where local governments have established chemical parks and provided incentives for companies from eastern China to locate there.

The scale of these relocations is quite large — one recent Chinese paper talks of 632 new transfer projects in the central, western and northeastern regions since 2019. It has even led to a partial backlash in the target provinces. For example, while about $900 million was invested in chemical projects in Ningxia Province from 2016 to 2020, chemical production near the Yellow River basin has been restricted by the central government‘s environmental policy since 2021. Therefore, Ningxia has significantly tightened environmental regulations in 2022. From then on, many of the inspections and supervision that have mainly affected companies in the coastal provinces will also apply to chemical companies in Ningxia. Accidents like the 2022 one in Lanzhou, Gansu province, at the Shandong-based pesticide manufacturer Binnong Technology‘s production facility (Lanzhou production did not begin until 2021) are likely to further speed up governmental supervision.

In any case, some of the relocations probably are not aligned with the objectives of the central government. For example, regulation specifically prohibits the transfer of outdated chemical production capacity across regions. However, the performance of provincial government officials is measured by a variety of parameters including both criteria related to environmental protection and to economic figures such as local employment and GDP growth — and there is a widely shared perception that in the less-developed, poorer provinces, the economic factors have a higher weight than in the richer coastal provinces.

One potential consequence of the production shift mentioned in this paper is an increasing separation of chemical production and chemical R&D. Highly qualified R&D chemists are unlikely to be willing to move to regions such as Ningxia or Inner Mongolia, preferring the lifestyle, educational infrastructure for their children and employment opportunities for their spouses only available in the highly developed coastal provinces. This potential split may be further enhanced by the specific promotion of R&D in places such as Shanghai, a place that (with a few exceptions) is unlikely to provide encouragement for the expansion of traditional chemical production.

Interestingly, foreign chemical companies have so far shifted their production far less of away from the coast than domestic players, though many of them have been affected by the closure of chemical parks and the relocation of chemical production to chemical parks. This is due to a variety of reasons. Generally, Western foreign companies have higher environmental standards and thus have had fewer problems adapting to the local tightening of these standards. Their production plants tend to be fairly large compared to the average Chinese player, and they are the preferred tenants of coastal Chinese chemical parks due to their higher safety and environmental standards as well as their above-average tax payments. In addition, Western companies are potentially more likely to pay a higher premium on being close to international airports and residing in cities that are attractive and easy to reach for expats and customers. Also, they tend to be active in chemical segments that are somewhat less price sensitive, relying on superior technology rather than the lowest production costs, and thus can afford the higher costs of the coastal provinces. In fact, some Western companies such as BYK have even expanded production in coastal areas such as Shanghai despite already having an inland production site in Anhui province.

In conclusion, it remains to be seen whether the relocation of chemical production away from the coastal provinces is a longer-term trend or just a short-term phenomenon that will weaken once regulation and its implementation becomes more unified throughout the country. In the latter case, the disadvantages of producing chemicals in the more remote areas — such as increased logistics costs, potential separation of production from R&D and the greater difficulty to find qualified personnel — may well outweigh the benefits.

Kai Pflug, CEO, Management Consulting — Chemicals, Shanghai, China