Iran: Rediscovering a Sleeping Giant

Iran has one of the longest histories of medical practice in the world. In the modern era, however, the Middle East country has fallen off the world‘s medical and pharmaceutical radar. Crippling international sanctions have restricted trade with Iran, severely affecting the pharmaceutical sector. But since January 2016, most international sanctions have been lifted under the internationally agreed Joint Comprehensive Plan of Action (JCPOA). As a result, early movers have the opportunity of gaining a head start in entering the Iranian market, provided they are aware of the risks and ambiguities and know how to mitigate them.

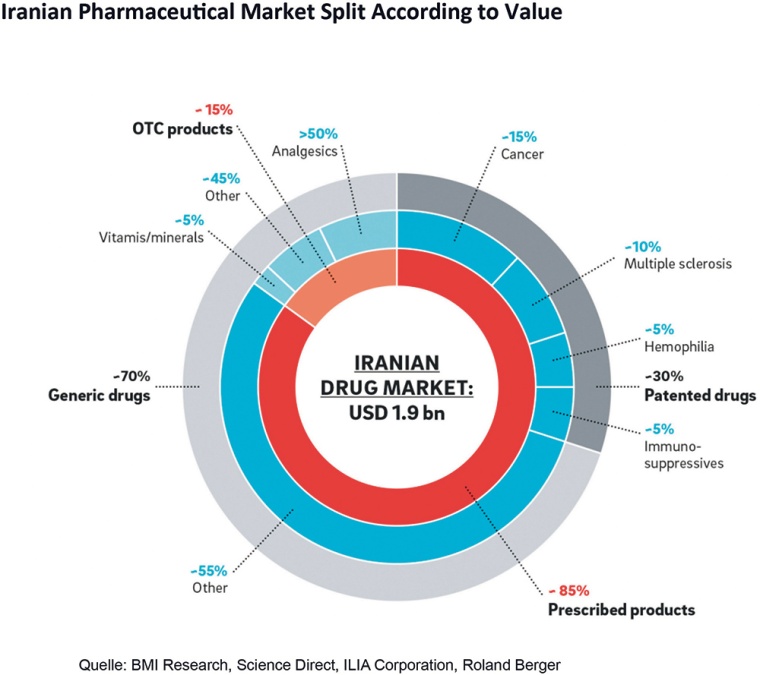

The Iranian pharmaceutical market has much to offer for new entrants. Being a trade crossroads due to its geographic location, Iran is an ideal export hub for Central Asia (population: 400 million) and, in addition offers positive market dynamics, an established pharmaceutical infrastructure, skilled workforce, and a competitive landscape. Iran’s pharmaceuticals sector is made up of about 100 companies. The country’s pharmaceuticals market – valued by BMI Research at $1.9 billion in 2015 – is predicted to grow at a compound annual growth rate of 6%. Some 60 pharmaceutical plants currently produce almost 40 billion drug units each year. More than 80% of Iranians receive a secondary education, according to the UN. But pharmaceutical companies must have a thorough understanding of Iranian market conditions to maximize opportunities and avoid pitfalls.

Enter – Prepare Well

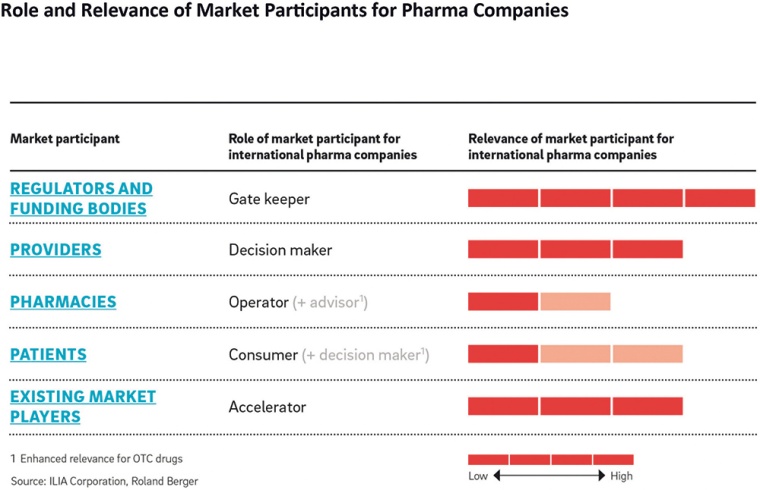

The Iranian healthcare system exhibits unique features that present both opportunities and hurdles for new entrants. Thorough preparation, including acquiring a deep knowledge of structure, decision makers and key stakeholders, is therefore essential, as is fostering good relationships with market players.

Regulators and funding bodies: Authorization from two government "gatekeeper" bodies is essential to successful trading in Iran. The first is the Food and Drug Administration of Iran (FDA), an agency that authorizes the import and manufacturing of all drugs, and controls the Iran Drug List (IDL). The second is the Supreme Council of Health Insurance (SCoHI). It decides which drugs can have their costs reimbursed and at what level. The costs of most drugs in Iran are reimbursable, so securing this status ensures a strong competitive advantage.

Providers: Prescribed medicines account for about 90% of sales value of drugs consumed in Iran, according to BMI research. This means the prescribing physician is usually the key decision maker in the buying process.

Pharmacies: There are around 8,500 pharmacies in Iran. About 55% are linked to public institutions, enjoying a large market share due to their near-monopoly position in the provision of scarce and expensive drugs. About 85% of patients present pharmacists with a predetermined prescription, but in the case of OTC drugs, which make up about 15% of total sales, pharmacists can advise patients.

Patients: Iran’s high proportion of prescription drug sales limits patient choice, but they have growing decision-making power in the expanding OTC market.

Existing market players: About 100 domestic pharma companies are active in Iran and can serve as accelerators for multinationals entering the market. Most are affiliated with government-backed investment companies.

Consider the Regulatory Framework

Approval process: FDA authorization is a prerequisite for the sale of drugs in Iran. The application process to introduce new drugs is not dissimilar to those in developed markets, but may be less transparent and more time consuming.

IP rights: Under current legislation, pharmaceutical formulae and compounds are not patentable, leading to extensive unauthorized production of generic medicines. However, with Iran currently seeking World Trade Organization membership, this is likely to change as the country will have to adopt the WTO's patent protection terms.

Pricing: Drug prices are determined by the FDA's Pricing Commission. It decides on the expenses incurred by producers and importers for each drug, and then fixes a price taking into account the upper range of cost.

Reimbursement: Health insurers pay 70% (outpatient dispensed) or 90% (inpatient dispensed) of the cost of drugs with reimbursement status. The remaining amount is paid by users. Most drugs have this status, but some drugs commonly used in the West do not.

Land – Start Smart

The setting up of backend functions will vary depending on the choice of local production or import. But in both cases the route to market is identical.

Sourcing: Half of the raw material used in drug manufacturing in Iran is imported. But local sourcing is on the rise, and a number of base materials required to make rare medicines have reportedly been produced since 2013.

Manufacturing: Whether carried out at self-owned facilities or those of partners, manufacturing in Iran must abide by certain cultural rules. Selected medicines and dosage advice must be halal compliant, for example.

Imports: Finished pharmaceutical products are shipped in by importing companies, which are often subsidiaries of large local pharma groups. These offer significant opportunities to tap into local expertise. Import taxes and custom tariffs range between 0 and 65% depending on whether the product has a locally produced equivalent.

Distribution: Drugs are primarily distributed by six government- owned companies. But smaller private operators are increasingly entering the market, with about 20 currently active. Overall, the 10 largest distributors have a 75% market share. This level of consolidation makes the leveraging of existing local networks an attractive option.

Exports: Iran's government is keen to promote the export of medicines to help chip away at its negative trade balance. By 2025 it hopes to have balanced exports and imports of medicines; as such, drug export income is tax exempt, and initiatives are underway to improve manufacturing practices.

Succeed – Win Fast

Several areas of unmet or growing demand exist in the Iranian pharma market. For example, increasingly blurred lines between OTC and prescription drugs mean that a significant number of prescription medicines can be bought directly by users. The market for vitamin and dietary supplements is expected to become another important area according to Euromonitor.

In the prescription sector, there are several supply gaps owing to the fact that many prescribed drugs cannot be produced locally. An expected epidemiological shift towards chronic diseases is likely to crank up this demand further.

Generic drug makers can also benefit from Iran's long tradition of favoring generic prescription medicines to keep down costs.

Leverage – Benefit from Partners and Competitors

Collaboration with local players is the dominant strategy employed by international companies wanting to establish a foothold and grow in the Iranian pharma market. Such partnerships offer new entrants access to infrastructure, distribution networks and key stakeholders. Tie-ups with domestic companies have proven particularly beneficial for companies wishing to establish import-export businesses, as local expertise can be tapped to help manage regulatory compliance.

Foreign investment in the Iranian pharmaceuticals market is picking up pace and becoming increasingly ambitious. In addition to the partnership strategies being employed by the multinationals, most of which focus on distribution, other companies are establishing a bricks-and-mortar presence.

Conclusion

There is little doubt that Iran offers multinational pharmaceutical companies clear growth opportunities. But it is not a straightforward operating environment and its unique character presents risks rarely found in most developed or developing markets. In order to mitigate these, it is recommended that new players comprehensively investigate local market mechanics, the regulatory framework, business culture and domestic competition before entering. New entrants may also wish to consider partnering with local firms to smooth their landing and enhance growth once operational. They should also closely study the actions of competitors. Prevention, after all, is better than cure.