MENA Pharmaceutical Market

The MENA (Middle East and North Africa) region is a largely untapped, yet potentially hugely fruitful part of the world for the pharmaceutical industry, both as a sales region and for the establishment of manufacturing facilities.

However, it is by no means a simple task for international firms to enter this market. This is due to a variety of factors, such as vastly differing spending powers amongst its constituent nations, the lack of a centralized pharmaceutical regulator, and varying preferences for branded products vs generics.

Market Share and Growth

Consisting of approximately 22 countries and with over 350 million inhabitants, the MENA pharmaceutical market was worth $36 billion in 2016, which represented 2% of the global market. This relatively low starting base is now seeing projected growth of 10%, vastly outstripping the current global growth rate of 4-6% – even surpassing the traditional “pharmemerging” economies such as Brazil and China.

Demographics

The growth of the pharmaceutical market in the MENA region is driven by a number of demographic factors. These include rapidly changing population dynamics, where populations are expanding, but also ageing. Additionally, lifestyle changes have led to higher incidences of non-contagious chronic diseases and conditions – most notably cardiovascular diseases, obesity and type-2 diabetes.

Pharmaceutical Usage and Government Policy

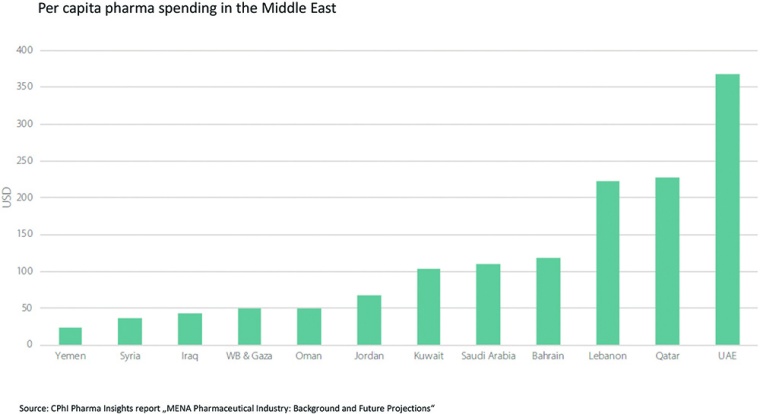

The current pharmaceutical markets in the MENA region vary greatly between different nations. For example, a high spending power and a cultural preference for expensive foreign brands in Saudi Arabia has resulted in 85% of pharmaceuticals in the country being imported, whereas in Egypt, 90% of consumption is domestically produced with a much greater market share for generics.

Africa as a whole has grown its pharmaceutical industry well over the past decade, with an expected value of around $40 billion by 2020. This is being driven significantly by urbanization, with more economically developed cities meaning that more people have the means to access medicines. Government policy is also encouraging local manufacturing of drugs, as imports currently outweigh exports. However, the rise of non-communicable diseases, and rising healthcare costs are likely to attract foreign investment into the continent, as well as the further development of domestic manufacturing capabilities.

In Sub-Saharan Africa, the largest pharmaceutical manufacturing market is found in South Africa, which is currently worth $2.8 billion. In recent years South Africa has turned increasingly to generic drugs, providing a great opportunity for both domestic and foreign manufacturers, with the generics market forecast to grow by a robust 12% compound annual growth rate (CAGR) during 2017-2022.

Another promising pharmaceutical industry is in Nigeria, with its compound growth rate projected to be around 9%, hitting $3.6 billion by 2026. Its population is also set to become the third largest in the world by the year 2050.

Countries in North Africa that have managed to establish pharmaceutical manufacturing industries in recent years include Morocco, Tunisia and Algeria. In 2015, the industry in Morocco was able to cater for 65% of the demand in the country (compared to 49% in Tunisia and 30% in Algeria). Pharmaceuticals produced in Morocco were also exported to Europe, other parts of Africa, and the Middle East. These capabilities could lead to partnerships being made between foreign and North African firms that have strong manufacturing and distribution networks.

Governments are central to the pharmaceutical industry in the MENA region, with their Ministries of Health regulating the industry and product prices. In an attempt to cut their healthcare spending and diversify their economy, the Saudi government are actively trying to increase generic consumption through regulating imported branded drugs and promoting local generics production. This has seen some notable recent investment from foreign firms into the country, including partnerships with domestic manufacturers, as well as the building of new facilities.

The European excipient certification organization EXCiPACT has now issued certificates in Saudi Arabia, indicating not only the development of the manufacturing industry in the country, but also its ability to meet high quality standards.

These developments could represent new trends developing over coming years for foreign pharmaceutical firms. On one hand, these firms could provide foreign direct investment (FDI) into the MENA region in order to penetrate the market through locally manufacturing. Another trend could be the partnering with other domestic manufacturers or CMOs to license their products and bring them to the region that way.

One of the crucial aspects of the MENA pharma market is the existence of the Gulf Cooperation Council (GCC). The GCC is a multinational partnership consisting of Bahrain, Oman, Saudi Arabia, Kuwait, the UAE and Qatar, who came together in 2014 to establish a drug price harmonization strategy in order to standardize drug prices within the region.

Although there was a growing awareness in many populations in the region for personal health and the benefits of over the counter pharmaceuticals, domestic regulations previously inhibited growth of some markets. The introduction of the GCC could see many of these regulatory barriers reduced, with an excellent example being the free trade agreement between the GCC and India that will likely result in further generic penetration into the Middle East market. It may be the case that final products are imported into the region from Indian generics manufacturers. However, due to a high average spending power and a cultural distrust of cheaper foreign made products, it is perhaps more likely that APIs will be imported, with local manufacturers providing the final product.

Another aspect to the Middle East pharmaceutical region that could be conducive for the growth of branded generics manufacturing is the increasing pressure on governments to cut healthcare budgets. This pressure could result in the implementation of compulsory healthcare insurance policies in order to reduce the burden on governments and pass costs onto private hands. This, in combination with a potential free trade agreement with India, could provide great opportunity for branded generics manufacturers. Due to insurance providers pushing for cheaper drugs to be used, plus a consumer preference for a recognizable brand, locally produced branded generics, perhaps using APIs from India, could thrive in coming years.

Egypt has a strong manufacturing industry; it is the largest producer and second largest consumer (after Saudi Arabia) of pharmaceuticals in the whole of the Middle East and Africa. Prices of both OTC and prescription drugs are controlled by the government.

Another part of the Middle East region that has a strong established pharmaceutical market at the moment is Israel. The market has been projected to grow to $2.12 billion by 2020, at a compound annual growth rate of 3.9%, according to a study by GlobalData.

Israel already has a strong network of academic and research institutes, R&D facilities and advanced medical facilities. Advancing biotech will likely be a driver of the market in future. This contrasts to the other markets in the region, many of which are emerging and are only just starting to build up this infrastructure to support their pharmaceutical industries.

Israel’s generics market, which accounts for around 20% of the market sales, is underpinned by Teva, the world’s leading generics manufacturer, which owns several manufacturing and export facilities across Israel, North America and Europe. However, there has been talk in recent months about Teva transitioning away from generic drugs in the future, to focus more on branded drugs and the development of new specialty pharmaceuticals, in the wake of growing competition from manufacturers based out of countries with cheaper labors.

This could present an opportunity for foreign businesses if Teva closes or sells some of their generics operations in the country, as they made $9.85 billion in generics revenue in 2016.

Future Trends

The healthcare agendas of countries in the MENA region are more heavily shaped by the government’s economic development agenda than those in Europe. For example, Saudi Arabia is trying to move away from being a purely oil-based economy, and so growing their healthcare sector is a good way of diversifying. However, this investment is also in part out of necessity – 25% of Saudis now have diabetes, as compared to just 10% of Americans. This may not only be due to increasing Westernized and sedentary lifestyles, but also to genetic predispositions, and so encouraging innovative drug discovery is highly in the country’s interest. This is a problem that is also facing Africa as well, as Western fast food grows in popularity and more people lead inactive lifestyles.

Another disease area that is also increasing in incidence are the rising oncological concerns in the MENA region. This is linked to increasing life expectancy, as age is the largest risk factor in any given cancer. One way in which foreign firms could benefit countries facing an increased cancer incidence is through education and encouraging the population to take diagnostic tests to address diseases earlier on.

There are also some difficulties faced when foreign companies attempt to introduce generics to the market in the MENA region. Stringent registration processes of a generic product and even its packaging, means a lot of effort is required to introduce a generic into a country. A lack of a centralized regulator means that these protocols will also differ from country to country, resulting in a reluctance for some foreign businesses to attempt to enter the generics market.

Conclusion

The diverse economic, political, cultural, and public health profiles in the MENA region are mirrored by a highly varied market environment for the pharmaceutical industry. In general, prospects look good for both foreign and domestic firms, with growing populations and longer life expectancies producing a much greater demand for pharmaceuticals in the Middle East and North Africa, with huge growth in the market projected over the coming years. Local generic manufacturers, and potentially foreign generic firms from countries such as India, who could set up manufacturing bases in the region and export from there, are likely to have good prospects.

However, this may not be the case for all international firms looking to enter the region; there is a current preference amongst several MENA countries to reduce imports of foreign branded drugs and increase both domestic production and consumption of generics. Nevertheless, foreign firms producing branded products have also recently begun to enter the region with direct investment in manufacturing facilities, such as Sanofi in Saudi Arabia, and this may be one of the optimal ways to enter this potentially highly lucrative market.

This article is based on the CPhI Pharma Insights report “MENA Pharmaceutical Industry: Background and Future Projections. The original publication including references is available here.

most read

Q1 2025 Chemical Industry: Diverging Trends

The first quarter of 2025 highlights a continued divergence between the European and US chemical industries.

Lead or Lag: Europe’s AI Materials Race

How AI and Robotics are reshaping the race for materials discovery.

Pharma 4.0 – the Key Enabler for Successful Digital Transformation in Pharma

Part 1: Building a Business Case for Pharma 4.0

Pharma 4.0—the Key Enabler for Successful Digital Transformation in Pharma

Part 3: Seven Theses for successful Digitalization in Pharma

US Tariffs Fatal for European Pharma

Trump's tariff policy is a considerable burden and a break with previous practice.