Selecting the Right European Location for Life Sciences Activities

KPMG’s Site Selection Report for Life Sciences Companies in Europe Provides Information for Companies as well as Governments

-

©rachwal - stock.adobe.com

©rachwal - stock.adobe.com

Agile and resilient: This is how manufacturers in the life sciences industry could be described during the Covid-19 pandemic. As disruption took hold in many other industries’ supply chains, life sciences companies moved to rapidly develop new products and build new capacity. They are maintaining this momentum, with pharmaceutical and biotech businesses showing continued interest in expanding existing operations in Europe or starting operations from scratch.

Fully integrated Biopharmaceutical companies and contract development & manufacturing organizations (CDMOs) can be seen developing existing manufacturing facilities or setting up new R&D centers in Europe.

At the same time, “first time launchers” — small biotech companies that are launching products for the first time — are beginning to realize that they do not need large pharmaceutical groups in order to do so. Instead, they are setting up their own distribution networks across Europe, while many are currently looking for the ideal location for their regional headquarters.

Further impetus is provided by climate discussions and the EU’s Green Deal, and a resurgence in industrial strategies to stimulate post-pandemic economic growth. These factors are encouraging governments across Europe to attract direct investments in the life sciences industry, which is generally a low-carbon-emitting and high-added-value sector. Tax incentives, grants and loans are all on offer, though it is always advisable to take a close look at the fine print of offers before taking such a big decision such as where to establish business operations.

Against this background, what should life sciences executives look for, and how do the various European jurisdictions compare? It is a simple question with a complex answer. Let us look at some of the contributing factors.

“Clusters of life sciences companies are a major plus; however, they can be victims of their own success.”

Taxes Are Suddenly Less Interesting

Large businesses that are planning significant capital investments in manufacturing plants or R&D facilities are generally attracted by low corporate tax rates. Life sciences companies, in particular, have typically structured their operating and tax models to benefit from low taxes and government incentive programs such as tax holidays. Such tax planning models have suddenly become far less relevant and will not give the desired return if they are based on an effective tax rate of less than 15%. This is because of moves by the OECD, where on 8 October 2021, 136 member states — representing over 90% of global GDP — agreed on a minimum corporate tax rate of 15% from 2023 on. Host countries are likely to raise tax rates to a minimum of 15% for companies with revenues above a certain threshold and abolish tax holiday schemes.

Loans or grants may become the preferred means of governments to attract foreign direct investments (FDI) instead — though such moves might be restricted by international state aid regulations and anti-subsidy rules. Moreover, governments are connecting their support for greenfield and brownfield projects to job creation and other commitments. Strict ‘claw back’ rules might apply if the recipient of governmental support does not comply with the predefined objectives.

Sticking Together: Cluster Size Matters

Clusters of life sciences companies are a major plus. They make it easier to attract and create an even larger pool of talent, expertise, and know-how. This in turn supports profitable pipelines. A positive cluster impact is particularly evident when it comes to innovation, as it can encourage a creative environment around a solid academic ecosystem, supporting the development of specialists and the discovery of new drugs.

Clusters can be victims of their own success, however. High demand for qualified talent, experts and specialists often means a spike in salary levels and increases in land prices and office rents. In many life sciences hotspots, a run on talent results in a rise in staff turnover and higher retention costs.

It can be difficult for life sciences companies to respond effectively to such developments, especially on more extensive manufacturing projects. It is therefore advisable to have a shortlist of locations that have a strong manufacturing industry outside the life sciences sector, such as food production, from where qualified staff may be sourced.

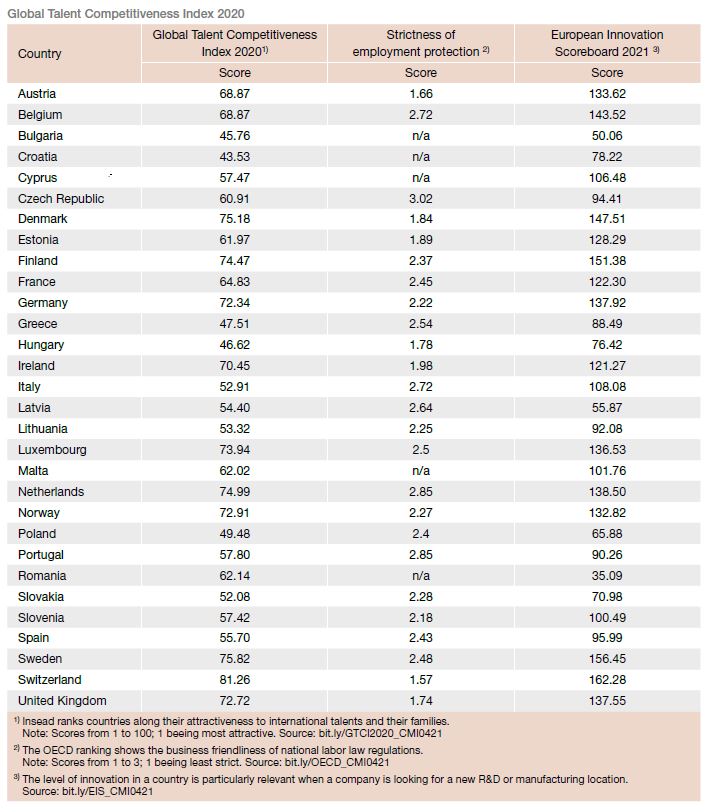

Balancing Salary Costs with Labor Law Flexibility

Salary costs can be an important decision factor when choosing a location. Yet, for life sciences projects, for which access to talent is key to success, this factor should be weighted carefully against the flexibility of labor law and a location’s attractiveness to specialists. Countries with flexible labor laws and high educational standards almost always also have high labor productivity which is one of the reasons for higher salary costs. By contrast, jurisdictions with lower salaries often lack the capacity to attract qualified workforce necessary to adequately staff operations.

André Guedel, Director — Head Intl. HQs Cluster, KPMG AG, Zurich, Switzerland

_________________________________________________________________

Site Selection Report

In September 2021, KPMG released the sixth edition of its report “Site Selection for Life Sciences Companies in Europe”. It is aimed at life sciences companies of any size that are looking at establishing or expanding operations in Europe, as well as governments seeking to benchmark themselves in terms of attractiveness for foreign direct investments (FDI) in the sector. The report is available for download: www.kpmg.ch/siteselection

_________________________________________________________________

-

André Guedel, KPMG

André Guedel, KPMG

Contact

KPMG

Badenerstrasse 172

8004 Zürich

Switzerland

+41 58 249 31 31