M&A in the Chemicals & Materials Sector in the First Half of 2012

What’s Up For Sale?

-

Recently, Squire Sanders commissioned a report from their partners at Mergermarket on mergers and acquisitions activity in the chemicals and industrials sector in 2011 and the first part of 2012. (C) Helene Souza / pixelio.de

Recently, Squire Sanders commissioned a report from their partners at Mergermarket on mergers and acquisitions activity in the chemicals and industrials sector in 2011 and the first part of 2012. (C) Helene Souza / pixelio.de -

Carolyn Buller, Squire Sanders

Carolyn Buller, Squire Sanders -

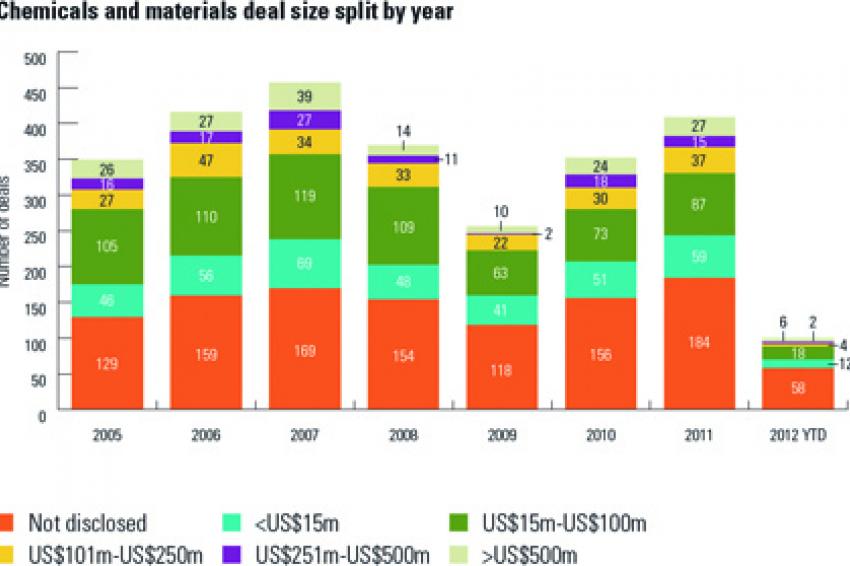

Fig. 1:

Fig. 1: -

Fig. 2:

Fig. 2: -

Fig. 3:

Fig. 3: -

Fig. 4:

Fig. 4:

Mergers & Acquisitions - Recently, Squire Sanders commissioned a report from their partners at Mergermarket on mergers and acquisitions activity in the chemicals and industrials sector in 2011 and the first part of 2012. The results were very interesting, bearing out what had been seen by Carolyn Buller, a specialist lawyer in the chemicals sector at first hand over the past few years.

As industry-watchers will know, the chemicals and materials sector, which can be cyclical, was directly affected by the disintegration of the global credit markets three years ago. The withdrawal of investors from the industry was inevitable and unsurprising. However, M&A activity did come to a virtual halt with both deal volumes and values falling dramatically - down 31% and 61% respectively on the previous year.

As the report demonstrates, there has been a slow and steady recovery underway since that time. In 2011 chemicals and materials M&A increased substantially from the previous year - with 409 deals completed, worth a combined $93.8 billion. That was a rise of 16% in volume and 56% in value on 2010. Private equity deals, which had slumped dramatically from 2008 to 2009, also saw an encouraging recovery. There were 55 private equity buyouts worth $6.7 billion in 2011, up 34% in volume and 56% in value from the previous year. And the evidence so far for 2012 shows this upward trend continuing.

Emerging Markets Attractive... But So Too Is North America

So, what is driving the recovery? An increasing interest in emerging markets for one thing - the desire to grow business in emerging economies has been a distinct characteristic of the chemicals and materials industry in the past few years. Some of 2011's largest deals showed this clearly. When Solvay of Belgium acquired France's Rhodia, part of the rationale was to strengthen the company's exposure to high-growth markets such as China and Brazil, where it generates 40% of sales.

Eastman Chemical Company's $4.6 billion acquisition of Solutia will enable strategic expansion into the Asia-Pacific region, with the company anticipating a compound annual growth rate of up to 10% in the next few years. More than 30 % of Solutia's sales came from the Asia-Pacific region prior to the acquisition. Such big-ticket deals are not the norm in the sector but they reflect well the trend that is also affecting the main mid-market. (The biggest proportion of M&A deals, where values have been disclosed, have been taking place in $15- 100 million range - some 39% in 2011).

In addition, players from the emerging markets themselves have also been driving many of the M&A deals in the sector. Investors from the Asia-Pacific sphere played a role in the upswing in M&A in 2011, with state-backed entities from the region snapping up companies specialising in raw materials, technology and innovation. Take ChinaChem's acquisition (through its subsidiary China National Agrochemical Corp) of 60% of Israel's Makhteshim Agan Group (MAI).

In turn MAI, a branded off-patent agrochemical producer, bought DuPont's non-mixture diruon herbicides business. While this deal illustrates the company's ambitious expansion plans, it also re-emphasises the central importance of the North America market to the global chemicals sector - the region is the most important target in terms of M&A value (46% in 2011-Q1 2012), and the second most important target in terms of deal volume (28% compared to 34% for Western Europe). As for bidders, North America again appears dominant in terms of M&A value (54% in 2011-Q1 2012), and neck-and-neck with Western Europe for deal volume (both at 32%).

Disposals and Exits Are Key

The MAI-DuPont deal last year is a good example of a corporate disposal, and this highlights another big trend in the recovery of the chemicals and materials sector. Corporate disposals have produced approximately half of all M&A targets between 2005 and 2011, with spin-offs from major chemicals players such as Dow and DuPont hitting the market - and frequently going into the hands of overseas buyers: examples from the past year are Brazil's Braskem SA acquiring Dow's polypropylene business and India's Indofil Chemicals Company buying Dow's European dithane fungicide business.

Private equity exits were a significant feature in the market too last year. Stand-out deals were Clariant AG of Switzerland buying the majority of Germany's Sued-Chemie - owned by One Equity Partners of the US - for $2.6 billion, and China's Wanhua Industrials Group acquiring a 58% stake in Hungary's BorsodChem from UK-based buyout house Permira and Austria-based VCP Vienna for $1.7 billion. Strong secondary buyout (SBO) activity has also been lifting the sector. SBO volume totalled 15, worth $4.5 billion, in 2011 and two SBOs were among the top ten largest chemicals deals globally.

What Can We Expect

We can assume that corporate disposals and private equity exits will continue to drive chemicals and materials M&A through 2012, despite continued anxieties about the Eurozone. So far in 2012 we have seen some 200 chemicals and materials deals worth $22.3 billion globally, with still about 38% of total deal volume coming from the $15 -100 million range. So we are on track for a similar level of activity to 2011.

However there are issues particular to the industry and its various sub-sectors which are worth considering as we go forward. Opportunism has characterised much M&A activity in the agrochemicals sector. But for specialty chemicals we are very likely to see vigorous competition for increasing market share.

A decade ago, specialty chemicals presented the ‘promised land' of higher margins and less capital investment. Many companies rushed to significantly increase their specialties investments. The result is no surprise: specialties are now seeing pressure on margins, as the competition to boost market share becomes more and more intense.

All businesses are exposed to rising costs, such as energy, but none more so than the petrochemical sector, where high and volatile commodity prices may reduce their attractiveness. On the other hand the development of unconventional sources such as shale gas should greatly contribute to the appeal of North American targets.

In fact, the shale phenomenon has been a major game-changer. In the past it has been taken for granted that the centre of the global chemical industry would be moving to the Middle East, and away from Europe and the US, driven by the abundance of relatively inexpensive oil feedstock in the Arab World. This idea has now been turned on its head. The shale gas phenomenon has created an abundance of ethylene and its derivatives, and set the stage for an abundance of inexpensive raw materials in the US.

It's not only the US that will benefit from shale discoveries. Argentina is on the cusp of large-scale production, and China's reserves could prove to be the world's largest. Both countries are actively looking for international partners.

We expect that this will translate directly into M&A opportunities for this year and especially in 2013. Indeed, energy independence a top priority for all major economies, after the volatility of commodity prices and the political turmoil in several oil-rich nations in the past few years.

Who would have predicted even two years ago, new refineries being built or old refineries reopening in the US? Now in 2012 that scenario is commonplace.

Contact

Squire Patton Boggs

7 Devonshire Square

London EC2M 4YH