The Miracle of Shale Gas

Changing the Global Petrochemical Landscape

-

Fig. 4: World shale gas resources assessment

Fig. 4: World shale gas resources assessment -

Vir Lakshman, head of chemicals and pharmaceuticals, Germany, KPMG

Vir Lakshman, head of chemicals and pharmaceuticals, Germany, KPMG -

Paul Harnick, global COO, chemicals and performance technologies, KPMG

Paul Harnick, global COO, chemicals and performance technologies, KPMG -

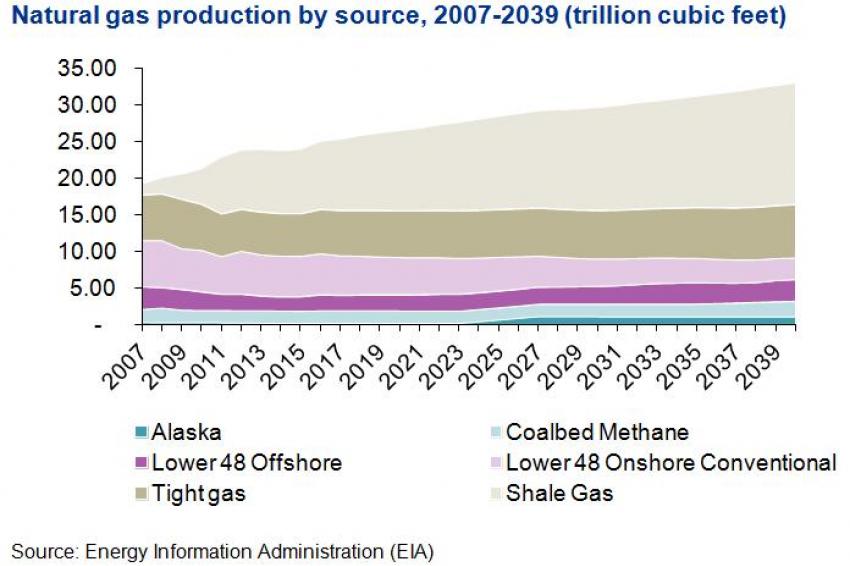

Fig. 1

Fig. 1 -

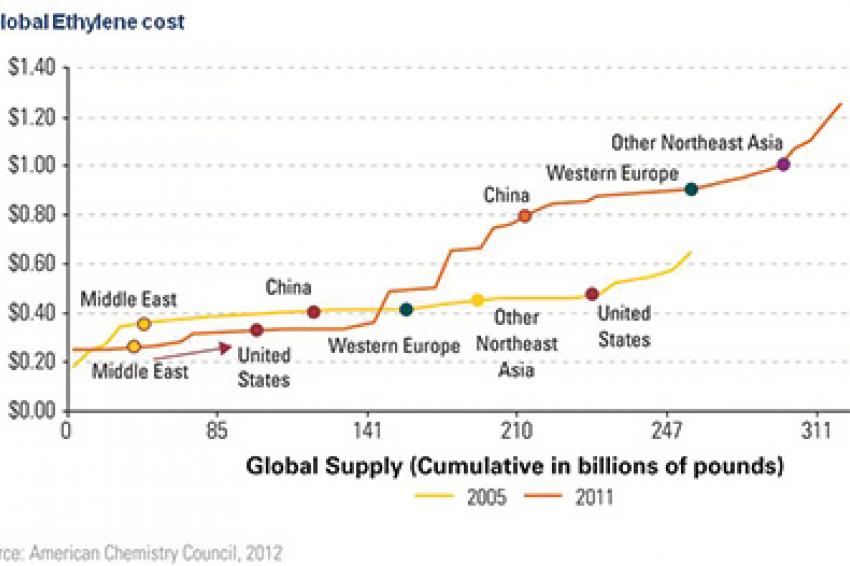

Fig. 2

Fig. 2 -

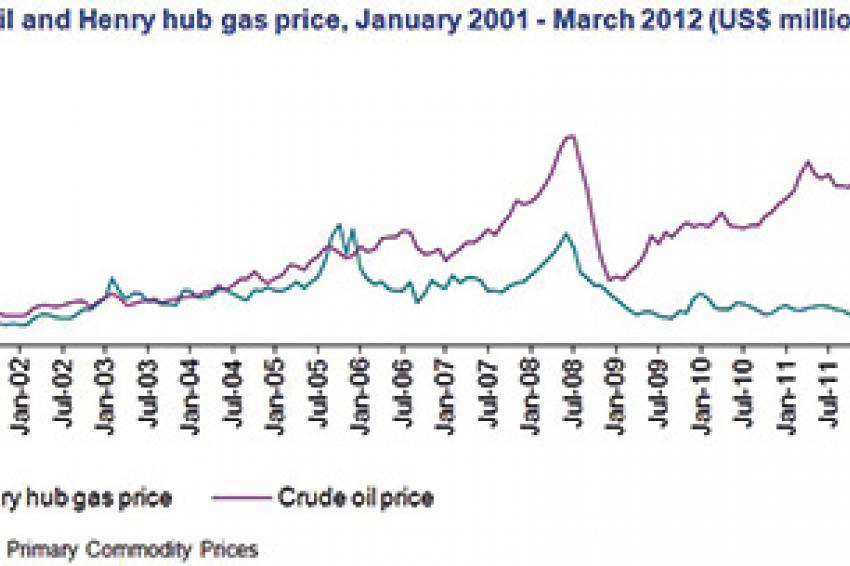

Fig. 3

Fig. 3 -

Fig. 5

Fig. 5 -

The discovery of abundant reserves of shale gas in the U.S. has driven down the natural gas price and has created a massive competitive advantage for U.S. companies. © Les Cunliffe - Fotolia.com

The discovery of abundant reserves of shale gas in the U.S. has driven down the natural gas price and has created a massive competitive advantage for U.S. companies. © Les Cunliffe - Fotolia.com

Cheap, Clean And Controversial - Shale gas has the potential to turn the world's energy industry on its head. It's abundant. It's cheap. It burns cleaner than other fossil fuels. And it's being found almost everywhere. But for shale gas to become a game-changer, the industry has to surmount tremendous organizational, reputational and regulatory hurdles.

Clean-Burning Benefits

Once captured and processed, natural gas is one of the cleanest burning and lowest carbon content fossil fuels. For companies subject to greenhouse-gas emission-reduction targets, natural gas usage may offer more "tick-the-box" benefits than traditional fossil fuel sources. At the consumer level, regions that rely on oil-based heating, such as parts of the United States, could bring their emissions down by encouraging homeowners to convert to natural gas heating. Additional incentives could be granted to promote the development and sale of vehicles powered by natural gas.

Pushing Prices Down

The discovery of abundant reserves of shale gas in the U.S. has driven down the natural gas price and has created a massive competitive advantage for U.S. companies. Generally a ratio of 6-1 between crude oil and gas prices is enough to make the U.S. chemical environment favorable. At today's prices, the disparity is more like 9-1, creating lasting advantages for U.S. producers. Cheap shale gas is also providing a boost to the wider U.S. manufacturing base - providing competitively priced energy such that "made in America" is becoming a cost competitive option again, leading some multinationals to rebase their production in the U.S.

Continued discoveries in unconventional oil reserves, coupled with growing production, efficiency improvements and a relatively slow recovery in North American demand, have all contributed to depressed gas prices.

This has led to a significant decline in dry gas shale development over the past 18 months. After growing from around 750 billion m3 in 2005 to more than 7,845 bcm in 2011, U.S. natural gas production is forecasted to remain effectively flat until 2015, according to the U.S. Energy Information Administration's Annual Energy Outlook.

Maximizing Shale's Potential

Certain regions of the U.S. lack pipelines, terminals and storage to hold and transport shale gas and oil to the customer base. In order to fully exploit the potential of shale gas, it is estimated that, between 2011 and 2035, the sector needs $2 trillion in upstream investments for wet gas production and $1.7 trillion for dry gas. An additional $205 billion capital spending would be required for gas infrastructure development, according to a report from private equity firm KKR & Co., with mainline gas transmission expanded by about 35,600 miles and an additional 589 billion cubic feet (bcf) of working gas storage. Although the required infrastructure will take decades to build, and gas prices may not recover for several years, there is no questioning shale's overall potential. In 2007, shale accounted for less than one-tenth of total gas production; by 2035, the U.S. Energy Information Administration forecasts it to reach half of total gas production.

Regulatory Debate On Fracking

The chemicals in the fracking process may contaminate local drinking water or the environment, which has led to a regulatory debate about shale gas. Despite its cost benefits, it must be noted that shale gas extraction remains a contentious and divisive issue for many politicians, communities and even the chemical industry. Nearly a dozen major energy companies, including Chevron and Shell, recently released a set of shared standards for fracking in the Appalachian region. While the regulatory debate about shale gas is still ongoing, the commercialization of shale gas has already heralded in a new era of growth and prosperity for the U.S. oil and gas industries.

Advantage: United States

Recent announcements from Dow, Shell, Sasol, Chevron Phillips and others suggest that we will likely see more than 10 million tons of new ethylene capacity come in stream by 2017. Investments in the extraction coupled with the sheer abundance of proven shale reserves (200 years based on current U.S. demand outlook) have made the U.S. industry the second most feedstock-advantaged region after the Middle East. As Middle East countries, however, continue to use more gas for domestic energy and fuel for water desalination plants, gas allocation to the petrochemical industry has become extremely limited, such that the U.S. is expected to become the most advantaged location for petrochemical production worldwide.

Until the development of European and Asian shale, which is not likely before 2017, the U.S. will continue to enjoy this competitive advantage. However, the U.S. market remains a mature economy, which will not be able to absorb all the planned chemical capacity. Therefore significant investment in supply chains is required along with a focus in establishing a broader growth market presence.

Three Potential Scenarios

As these dynamics play out over the next few years, the shale phenomenon is likely to fundamentally alter the established pattern of global petrochemical trade flows. We see three potential scenarios, which are not necessarily mutually exclusive. The first is the potential for a return to boom and bust cyclicality in the U.S. - the U.S. commodity chemical industry is currently well rationalized - perhaps for the first time ever - with much of the historic cyclicality removed and commodity chemical businesses enjoying stable long-term returns. If U.S. chemical companies are unwilling or unable to develop customers for their products outside of the U.S., we are likely to see the return of cyclicality, resulting in large margin swings through the cycle, the closure of old plants at the bottom of the cycle and all the other ills historically attributed to the commodity industry in the U.S.

The second scenario is price and margin erosion in Asia. The Asian market is currently predominantly served by local product supplemented by vast imports from the Middle East. We are already seeing a shortage of ethane feedstock for the chemical industry in the Middle East, with new and forthcoming expansions increasingly relying on more expensive naphtha-based feeds. The U.S. market is mature and may not be able to absorb all of the planned capacity. As U.S. product starts to flow to Asian markets, we may see increased price competition - which may become increasingly fierce if some of the implications above have already started to affect the U.S. market - making producers increasingly desperate to sell their product whatever the cost.

The third potential scenario spells trouble for the petrochemical industry in Europe. Large parts of the European commodity chemical industry are characterized by overcapacity and older, less efficient plants. If U.S. producers export directly to Europe, or if Middle Eastern producers respond to increased competition in Asia by switching their export focus to Europe, many European commodity chemical producers will find themselves at a severe cost disadvantage, making it difficult for them to compete. That is not to say the European chemical industry is doomed, as many have predicted. Rather, we are likely to see a continued squeeze on the commodity end of the sector with companies focusing on high-value specialty chemical areas, where European companies continue to have an advantage on many of their overseas competitors based on long-established technology and know-how.

U.S. Prevails For Now

While many other areas of the world have huge potential shale gas resources (fig. 4), there are many challenges associated with bringing production to a commercial scale. If we focus on some of the world's key chemical markets, China has recoverable reserves of 1,275 trillion ft3 but lacks the horizontal drilling technology required for extraction - not to mention the thousands of miles of pipeline that would be required to get the gas to the chemical producing regions on the east coast. Likewise, Germany and Poland lack the pipeline infrastructure to move gas from the shale basins. Environmental issues abound, not least in France where the government has banned fracking. Even in the UK, where test drilling has started with government support and where an established gas pipeline is in place, we are unlikely to see commercially significant quantities of shale gas this side of 2020. Finally, in Europe as a whole, even if the pace of shale gas extraction accelerated, only four of 45 steam crackers on the continent are capable of consuming gas feedstock in significant quantities. As such, the U.S. chemical industry is likely to retain its feedstock advantage for considerable time to come.

Contact

KPMG AG Wirtschaftsprüfungsges.

Tersteegenstr. 19 -31

40474 Düsseldorf

Germany