Transformation of the Chemical Distribution Industry

Adapting to Market Trends and Customer Expectations Is Essential to Stay in Business

-

For Chemical Distributors, Adapting to Market Trends and Customer Expectations Is Essential to Stay in Business (c) leungchopan/Shutterstock

For Chemical Distributors, Adapting to Market Trends and Customer Expectations Is Essential to Stay in Business (c) leungchopan/Shutterstock -

Guenther Eberhard, DistriConsult

Guenther Eberhard, DistriConsult -

Jürgen Mohrhauer, DistriConsult

Jürgen Mohrhauer, DistriConsult -

M&A Activity by Continent (2009 onwards). Source: DistriConsult 2018 (C) CHEManager

M&A Activity by Continent (2009 onwards). Source: DistriConsult 2018 (C) CHEManager -

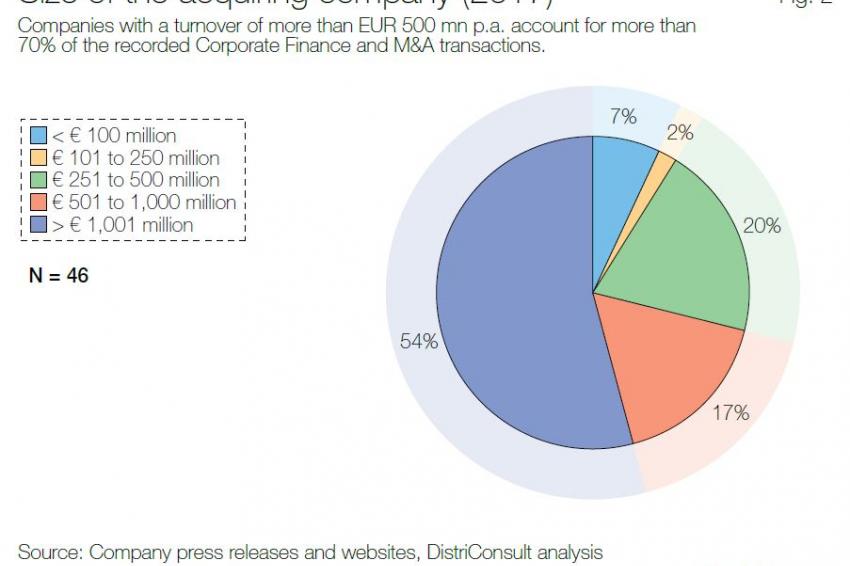

Size of the acquiring Company (2017). Source: DistriConsult 2018 (C) CHEManager

Size of the acquiring Company (2017). Source: DistriConsult 2018 (C) CHEManager -

Rationale of M&A Transactions (2017). Source: DistriConsult 2018 (C) CHEManager

Rationale of M&A Transactions (2017). Source: DistriConsult 2018 (C) CHEManager

Everywhere in business today, customers, suppliers, employees, shareholders or owners, consultants and other pundits, and also the media seem to only have one topic. It is “digitalization” and the upheaval it will bring. These perceived and sometimes even real changes, currently impacting the economy in general, are having an influence on the chemical industry and within that also the chemical distribution industry.

The changes come in virtual form, labelled “Chemical Industry 4.0” and “Digitalization”, and also in physical form, as the “Circular Economy”. Some perceive them as a threat. But they can also be seen as an opportunity, just like all those changes over the last centuries, which have at any one time challenged the status quo. Now, as back then, adapting to market trends and customer expectations is essential to stay in business.

A Short Look Back

Trading and distribution companies have long played a significant role in opening new markets and developing additional sources of supply for the emerging global economy.

Since the early years of chemical production in the 1860’s, when everybody was mostly producing locally around the raw material sources, the need for specialized traders for these products to establish additional and often further away markets was there. That continued through the first half of the 20th century when transcontinental trade was expanding, particularly after WW II.

During the “globalization and specialization” of the chemical industry since the 1980’s and the cost-optimizing and outsourcing efforts of the last 20 years, the chemical distributors became an important marketing and sales arm for the product supplier, more and more a specialist for the downstream markets, but also a partner of the customer, with in-depth application knowledge adapting to technologies available. Small and medium-sized customers value this, but also the “one-stop-shop” capabilities for several products needed for their formulation, not necessarily supplied by a single producer.

Driven by the large range of products delivered into the marketplace due to the suppliers’ portfolio enlargement and the existing regional and geographic differences, a local supplier was needed. The producer focused on the large strategic accounts for cost-effectiveness, while the marketplace changed form a producer-oriented supply field to a more customer focused value field: the link to the medium customers is kept by the chemical distributors, when it comes to specialties and formulations.

The “New Normal” ahead of us

The break-up of the traditional large chemical sites into “industry parks” through specialization trends within the industry and significant M&A activities have changed the landscape of the chemical industry again in recent times. New sourcing areas have developed in Asia (especially in China, but also in India), and the traditional raw-material regions, like the Middle-East, are emerging into down-stream producers, paving the way for more competition, and forcing the distributors to re-position the offering while being “stuck in the middle”, needing to gain size and coverage (geographically and with respect to industries served). And not enough, alongside to these movements and re-configurations, IT-related developments such as “Artificial Intelligence” (AI for short) and “Big Data” have reached the chemical industry. The envisioned shift is potentially so big that everybody is talking about nothing else but Chemical Industry 4.0. What could this potentially mean for the chemical distributors?

The chemical industry has been a quick adaptor of “Information Technologies”, but traditionally in the engineering and production area. Now it is being challenged with combining data generated internally with external market and customer data in order to create additional value. The so-far “linear structure” of our economy will become much more a sort of complex eco-system, with significant interdependencies, which will not be easy to determine upfront and then “manage” smartly for this relative conservative industry, alas also for the distribution sector.

However, this is now the opportunity to utilize digitized records to improve and streamline business processes, create new business models and solutions for competitive advantage and to serve customers even better, by being able to model and predict developments earlier and faster.

Achieving efficiency, taking cost out of the system and supporting decision-making is probably the most palpable short-term effect from the so-called “digital transformation” for the distribution industry. This does not mean, that all sales will be settled by a “click of a mouse”, but where it makes sense, e.g. in transactional types of purchases, an intelligent platform or e-commerce facility is conceivable, with chemical distributors staying part of the offering on their own, or partnering with their supplier as an external service operator.

Going for such a concept of “lowest delivered cost” as suggested in the 1990s by Derek Abell, then a Professor of Strategy Marketing at IMD, is in essence commoditization strategy. And that may not be the smartest thing to do as the core value proposition for many distributors is based on differentiation, trying to project the “highest perceived value” to a customer base. Although cost must be kept under control at all times.

For the more “performance critical” products and applications, where product know-how and formulation technology (and all their inherent limits to digitalization) are crucial, it can be envisioned that digitalized communication can be of a benefit, when utilizing blogs, chats, webinars, and bots to clarify standard (and sometimes even specific) application issues, conduct product trainings or discuss commercial terms. Relationship will still matter in many cases, and after all, chemical distribution will stay a mostly local business for a foreseeable time. Thus, these technologies can be important as set up is fast and efficient and benefits in the relationship can be achieved for all stakeholders.

The more complex set-up and use of new business models using data-based technology will have to be determined on an individual basis; there will not be the “one-size fits all” approach, as geography, application market, competitive position and strategic intent are very diverse in this industry. But chemical distributors need to be aware and ready to act when requirements evolve.

What about the Resulting Threats?

A potential threat is facing the distribution industry when upstream producers start to take back former distribution accounts utilizing the possibilities of new technologies that are making it easier and cheaper to handle even smaller accounts. To make up for potential losses of volume, chemical distributors must engage in new areas of business that are currently not the main emphasis.

The evolving and increasing “Circular Economy” will be an area of opportunity to enhance the portfolio of services, which have been offered historically, like bulk-breaking, repackaging, diluting, pre-formulating etc. by building on the existing strengths of being in the distribution sector, close to the formulator using the products.

These services will help customers and suppliers by supporting them beyond storage and delivery, when being challenged with the demand to “use less, use longer, use again” by end-users of formulations and products, increasing efficiency, life-span and recovery of materials, molecules and energy.

Services could include items such as the re-assignment and offering of out of shelf-life material and off-spec material, the take-back and redistribution of overstock material, the collection and re-offering of recovered/recycled material for re-use, waste collection and disposal, and offering more materials from renewable sources for “classic” applications, just to name a few. Some of this is not new, but it could evolve into more of a business activity by itself.

This approach would look at the value chain in a more comprehensive way, when in the future value creation is more geared to delivering smart solutions rather than pure supply of chemicals. Utilizing the already existing market links with customers and suppliers by reallocating the product knowledge to the next level of requirements would need to be supported by enhanced data-driven technology.

Differentiation will be Key

Already today, differentiation is an important strategy to evade strong price pressure., In the future it will be more and more a key lever to generate a competitive edge in the marketplace. Even with less drastic changes in the business model, chemical distributors will enhance their visibility and promote their competencies by cooperating with suppliers and customers on technical projects, putting their expertise to work. Here it helps to have invested in a laboratory infrastructure (for selected industries) that can help when dealing with small and medium sized customers in jump-starting their development work.

Distributors are also engaging more and more in conferences and fairs with technical papers. To be better visible in a “crowded space” and to showcase their technical capabilities, they are increasingly applying for (and winning!) awards set up by conference and trade show organizers as an additional offer to presenters and exhibitors.

Absorbing other newly available technology, capturing the value generated through utilization of data enhanced insights and sustaining these gains through an optimized way to operate will help making life easier, for customers, suppliers and the distributors themselves, not much different from what has been the driver in the past.

Yes, there is a lot in for me as a chemical distributor, taking on the challenges of today and staying on top of the developments by selectively engaging in digitalization programs. It is not about a complete re-design and rebuilding of an end-to-end virtual distributor in the digital space, but more about applying just those selected technologies and business practices, required to stay ahead in business, while keeping a close eye on meeting the needs of customers and suppliers. This has always been a driver for the commercial success and the sustainability of the chemical distribution industry.

Contact

DistriConsult GmbH

Säntisstrasse 69C

8820 Wädenswil

Switzerland

+41 44 680 1431

+41 44 680 1432