Trade and Industry Investment of the US Chemical Sector

25.11.2017 -

-

(c) jannoon028/Shutterstock

(c) jannoon028/Shutterstock -

Heather R. Rose-Glowacki, American Chemistry Council

Heather R. Rose-Glowacki, American Chemistry Council -

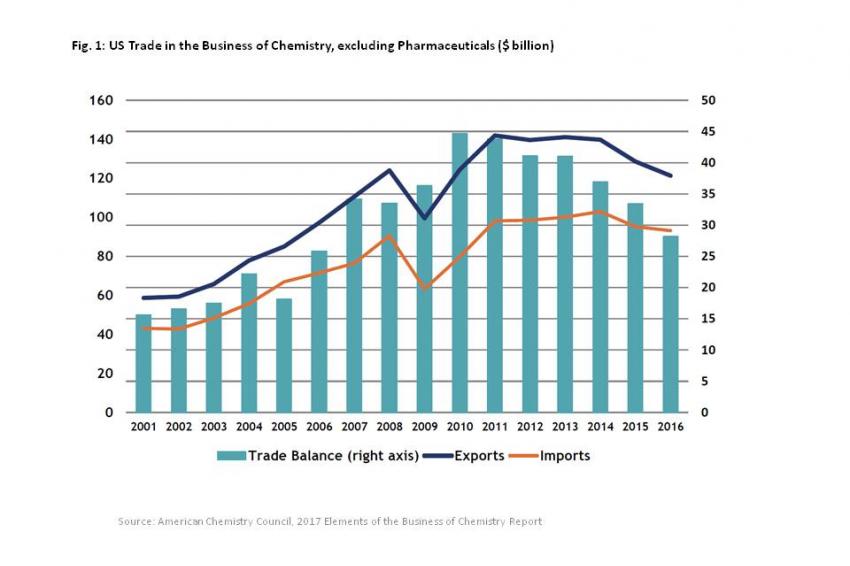

Figure 1

Figure 1 -

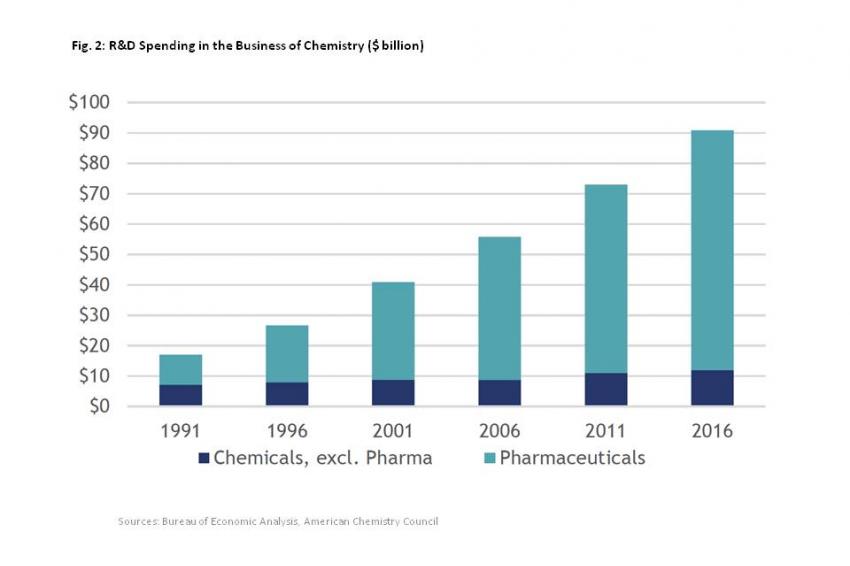

Figure 2

Figure 2 -

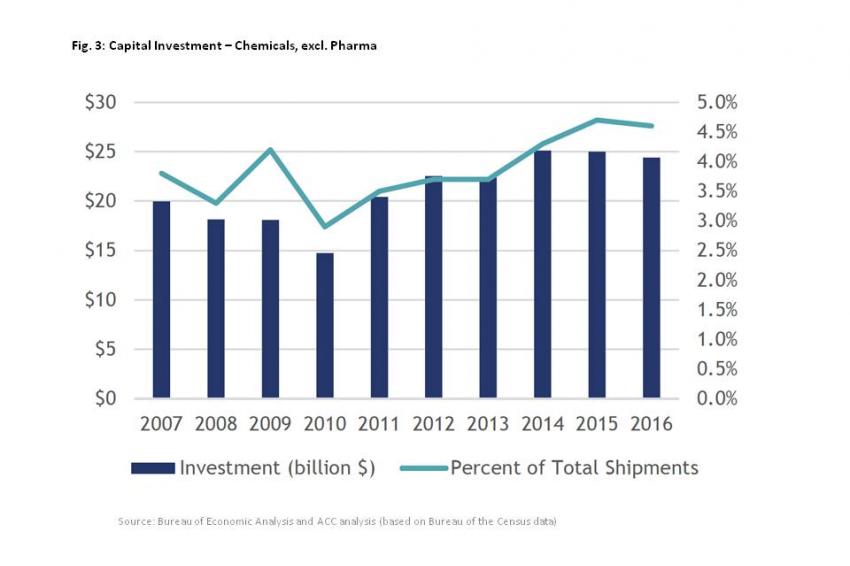

Figure 3

Figure 3

The American chemical industry is a dynamic, forward-looking industry and a keystone of the domestic economy. One of the oldest industries in the United States, the US chemical industry is the world’s second largest (after China) with 14% of global chemical shipments. The chemical industry is also a large exporting sector in the US, accounting for more than ten cents out of every dollar of American exports.

Billions of dollars are invested in the US chemical industry each year. Since 2010, companies have announced more than $185 billion in new chemical investment in the US, more than half of which is foreign-direct investment. In addition, investments are routinely made in intangible assets, such as employee knowledge, brands, process technology, and data as well in physical assets, such as property and equipment. These investments help ensure that chemical companies in the US continue to be leaders on a global basis.

US Trade

The globalization of chemical industry investments and markets has spread capital resources, technology, and managerial capabilities around the world, resulting in a growing population of multinational chemical companies. As such, the international trade of chemicals reflects an intense competition for markets by producers in an increasingly global industry. Indeed, during the past decade, world trade in chemicals grew faster than global output. Total global chemicals trade is astounding, representing $215 billion in 2016, a significant portion of which is between related parties (intra-company).

The US chemical industry, with abundant natural resources and a highly skilled workforce, has long been a major exporter of chemistry products. The industry has consistently posted a large surplus in chemicals trade, peaking at $44.6 billion in 2010 – more than three times the surplus two decades earlier. Although the trade surplus has moderated since then, US imports and exports have, in general, exhibited a positive growth trajectory.

On a regional basis, there is a good deal of trade within North America. Canada, the largest single national market for US chemical exports, and Mexico, the second-largest, together account for one-third (nearly $40 billion) of US chemical exports. Canada is also one of the largest sources of chemical imports to the US, most of which are plastic resins and commodity chemicals.

Nearly one-fourth of American chemical production is exported. Outside North America, the largest markets for US chemistry exports are China, Belgium, Brazil, and Japan. While imports account for a slightly lower percentage of domestic consumption, more than half of US chemical imports are essential inputs used for domestic chemical production. After Canada, the top countries for US chemical imports are China, Germany, Ireland and Japan.

Investment in the Future: Knowledge

In order to maintain its position as a major trade partner, the US chemical industry must continue to innovate. Innovation – putting ideas into action through knowledge to create new products and services to meet the needs of current and future customers – is a long-term driver of financial performance and value creation in the chemical industry. From research and development (R&D) to business processes to customer relationships and knowledge, the leading-edge technologies made possible by chemistry improve functionality, reduce costs, and increase productivity.

In 2016, the American chemical industry – one of the largest private-sector industry investors in R&D – spent an estimated $12 billion on R&D. US chemical companies typically allocate 2-3% of their annual sales toward R&D and, over the last century, R&D efforts in the chemical industry have expanded, even in times of lower profit margins. Successful research in the chemical industry requires intensive effort and major expenditures; it can take years from the time a project is conceived to the time a chemical product is brought to the marketplace. For each success, there may be as many as 100 failures. Rates of return on successful innovations, however, can be quite high, often in the range of 20 to 30%.

Beyond products and processes, an increasing importance is placed on service innovations and many chemical companies have added management services to their portfolio in addition to – and sometimes instead of – chemical products. Specialty chemical and performance materials companies, in particular, require extensive technical servicing components with highly-trained service and sales representatives, knowledgeable customer service problem-solvers, and EH&S professionals.

Service innovations in the chemical industry are especially prominent in the automotive and electronics industries. Automobile manufacturers require specific properties when considering paint and coating applications (e.g., anti-corrosion properties). Rather than purchasing paint by the gallon, automobile companies engage with coatings manufacturers to meet individual requirements. The coatings companies are often integrated in the automotive manufacturing, running complete coatings operations at body plants. In the electronics industry, a chemical supplier may “lease” chemicals to a semiconductor company to process the chips, so that the semiconductor company is free from the management of used chemicals.

Investment in the Future: Capital

As companies continue to innovate, it remains critical that the chemical industry invests in the physical structures and equipment needed to maintain high levels of production. The chemical industry is capital intensive due to the large plant capacities and amount of equipment needed, the intricate nature of the equipment and processes, the high degree of process automation, technology requirements, and depreciation of process plants, among other factors.

In 2016, the US chemical industry was one of the largest private-sector investors in new plants and equipment (P&E) in the country, with over $24 billion in capital investment. Equipment investments, in particular, are notably important to long-term growth potential because equipment (e.g., instrumentation, computers, and automation technologies) is directly involved in the chemical production process. To a large degree, structures in the business of chemistry protect chemical processes from the elements, and support process equipment. Investments in P&E are made for a number or reasons, such as expanding production capacity for both new and existing products, replacing worn-out or obsolete plant and equipment, and improving operating efficiencies. It is common for existing chemical plants to undergo complete modernization programs that utilize the latest process technologies.

The financial-resources-employed-per-worker ratio is a good indicator of the adequacy of capital formation. Increasing levels of capital employed per worker have long been noted as a key to improved productivity, indicating that workers are equipped with the latest technological innovations embodied in the acquisition of new capital (and capacity). Higher productivity is, in turn, typically accompanied by higher real wages for workers. Among US manufacturing industries, chemistry is second only to petroleum refining in terms of capital employed per worker.

As the chemical industry becomes more integrated on a global basis, companies around the world strive to maintain, and hopefully grow, their market share. However, the valuation of companies goes beyond annual sales. It is the intangible assets – brands, technologies, and data and information about products, customers, and business processes, as well as more traditional intellectual property, such as patents, trademarks, and regulatory licenses – that increasingly define “real value.” As the dynamics of the global economy change, the US continues to be a leader in the global chemical industry and an integral part of the domestic economy.