Germany’s Chemical Industry: Steeled for Competition

Germany is an Attractive Chemical Production Location due to Innovative Capacity and Productivity

-

(c) totojang1977/Shutterstock

(c) totojang1977/Shutterstock -

Dr. Thorsten Bug, Germany Trade and Invest

Dr. Thorsten Bug, Germany Trade and Invest -

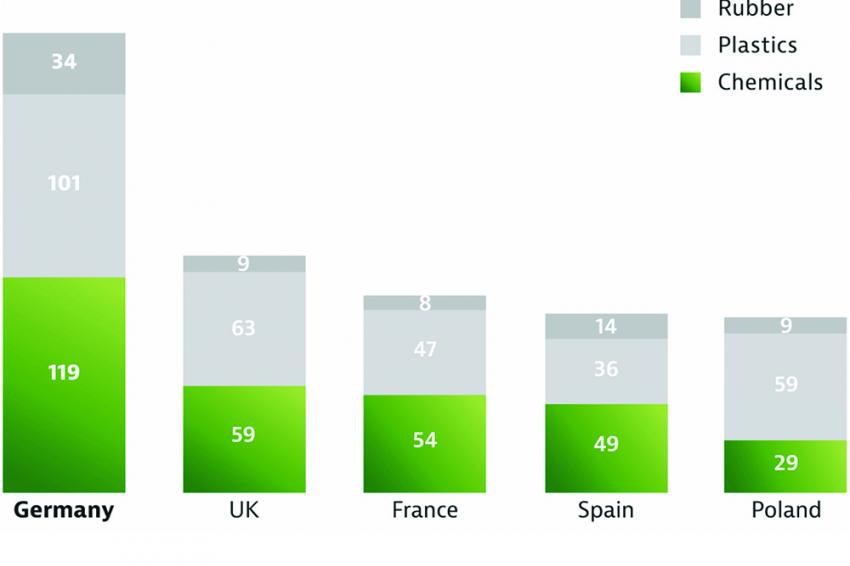

Fig. 1: Top-5 chemical industry FDI destinations in Europe (2011-2015)

Fig. 1: Top-5 chemical industry FDI destinations in Europe (2011-2015) -

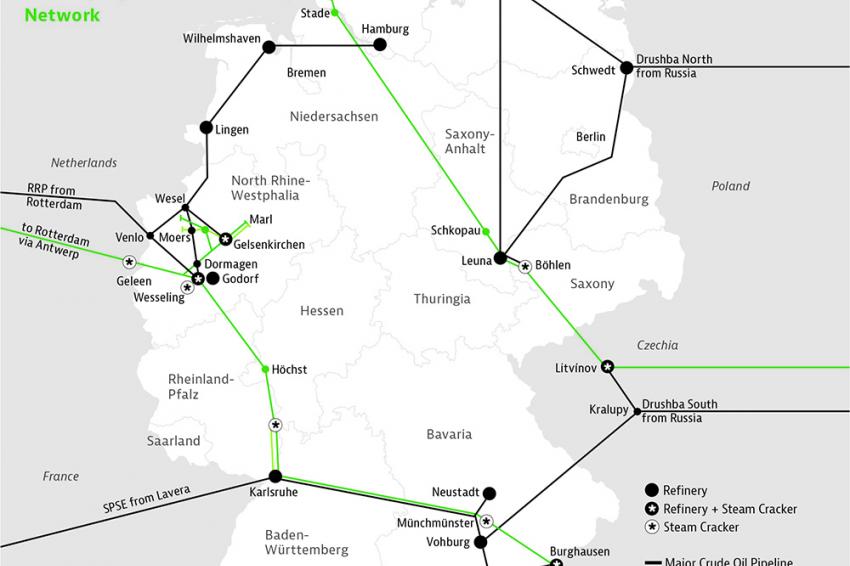

Fig. 2: Germany’s Chemical Industry Pipeline Network

Fig. 2: Germany’s Chemical Industry Pipeline Network

Germany is known for its rigorous environmental standards, its obsession with renewable energy, and high labor cost. Yet Germany’s chemical industry continues to be number one in Europe by a large margin and local companies export more chemicals than any other European country, and even China. Here is why:

The global chemicals market is in excellent shape. This is reflected primarily in the huge increase in global sales from €1,622 billion to €3,534 billion during the decade from 2005 to 2015, equivalent to an average annual growth rate of more than 8%. However the balance of power in the global industry has shifted. The chemical industry in China – with revenue of €1,409 billion and a global share of about 40% – was the biggest market in 2015, followed by the US (€519 billion), Germany (€148 billion), and Japan (€136 billion) according to CEFIC. The German Chemical Industry accounted for 28% of the €519 billion in sales in the total European market in 2015, thereby maintaining the lion’s share of revenue – twice as much as its nearest European counterpart. The industry not only maintained its position within Europe over the past few years, it actually improved it.

Growth-Driving Industries

One of the largest contributors to the industry’s success in Germany is the presence of strong client industries including the automotive sector with sales of more than €400 billion in 2016. As a result of close collaboration between chemical suppliers and their industrial clients, and the global expansion of Germany’s industrial manufacturers, the chemical industry has been able to expand into new markets with them. This is reflected in the export numbers of the chemical industry. In 2015, Germany was the world’s second largest exporter of chemicals – with a value of around €100 billion and global market share of 9.3%, numbers surpassed only by the US.

Another success factor of Germany’s chemical industry is its capacity for innovation. As the largest chemicals market in Europe, Germany has one of the highest R&D intensity levels in Europe, with 2.8% of revenue spent on R&D in 2015 making it the continent's innovation hub. As a result, the second-highest number of patents (18%) in the chemical industry at the European Patent Office originate from Germany.

This strength in innovation combined with productivity has helped establish Germany as an attractive chemical industry production location. In the latter respect, Germany’s chemical companies were able to reduce their energy needs by 20% between 1990 and 2010 - with output over the same period increasing by almost 60%. As a result of these efforts, the production output of basic chemicals – including ethylene, chlorine and ethylene oxide – has remained constant since 2000.

Germany’s Chemical Parks: The Old Retainer

The traditional chemical production sites – some of them more than a century old – have, through good strategic investment and production optimization, been integrated into a network of highly integrated production sites: Germany’s unique Chemical Parks. The country’s chemical complexes are served by excellent logistics networks – from road and rail to waterway and pipeline (fig. 2). Investments are constantly being made to improve provision across the existing logistics infrastructure.

With their ‘plug and play’ concept, Germany’s chemical parks are able to offer state-of-the-art conditions for international investors. Investors can choose the services from a site operator that suits their business model best. The new production site, developed sites and site security services are all made available for the investor’s core activities. Optional services such as warehousing, logistics, and analytics can also be requested as needed. German Chemical Parks increase cost effectiveness by splitting cost and overhead – a benefit to both the site operator/owner and investor.

Chemical parks offer a wide range of business models. Subject to the investor’s individual requirements, land can be leased or purchased in order to establish a production unit. At the other end of the scale, a site operator invests in and operates the new plant for the investor on a custom or toll manufacturing basis. Investors are supported by a number of investment planning and construction services. The most sought-after service is for permit applications. Licensing procedures are completed quickly and efficiently with the competent public authorities assisting in the process from a very early stage.

High-Quality Energy on Tap

A secure power supply is imperative for profitable industrial plant operation. Chemical parks secure their energy through the provision of a number of redundant supply lines. Most chemical parks operate their own on-site power plants in order to secure supply. A continuous supply of steam and overall energy are also key cost success factors. On-site power plants utilize the high efficiencies found in combined cycle heat and power (CHP) generation, thus further optimizing energy production

The reliability of Germany’s electricity supply is very high by international standards. Unlike some countries in Europe where major blackouts are recurrent, power outages are definitely the exception in Germany, where grids lose just 14 minutes per year in interruptions.

German Workers: Never Strike Out

One of the largest cost drivers in production processes is the cost of labor, including critical cost aspects such as motivation and days lost to industrial action. According to the IMD World Competitiveness Yearbook 2016, German employee motivation levels are very high. This can be derived from the fact that Germans work more than their international peers (41.2 hours per week) and lose less days per annum due to industrial action than other market-determining European nations. There were a total of 19 strike days per thousand employees (equal to about 220,000 working days per year in Germany) in the seven-year period between 2009 and 2015 – exactly half of the European average. The high level of workforce satisfaction is further illustrated by the fact that the last strike action in the chemical industry in Germany took place in 1971. This reflects the good cooperation between the IGBCE trade union and companies in the sector.

Similar to the low strike numbers, wage increases have been very moderate in Germany compared with other countries in the EU. The overall labor cost gap between Germany and its eastern European neighbors has been significantly reduced in the past decade. Since 2006, wages in the European Union have grown on average by 2.5%.

Steeled for Competition

The presence of strong client industries, cost-efficient production, and sensible labor market reforms prior to the financial crisis in 2008, which gave corporations higher labor flexibility, have allowed the German chemical industry to consolidate its market-leading position within Europe. This is best evidenced by a strong increase in foreign direct investment in Germany (fig. 1). Much of this investment is in basic chemicals, against public perception. The goal of these investments is to ensure the global competitiveness of the respective facilities, which is why so many of the investments involve keeping technology up to date.

Amid global competition, production capacities with sensitive cost structures will further migrate away from industrial regions. However, because of its specific strengths, particularly in innovation, productivity, and resource efficiency, Germany, alongside the US and Japan, will continue to be a highly attractive production location for the chemical industry.