No Sign of a Crisis?

FDI in Chemicals is Playing by its Own Rules

-

Dr. Tobias Lewe, A. T. Kearney

Dr. Tobias Lewe, A. T. Kearney -

Ulrich Deutschmann, A. T. Kearney

Ulrich Deutschmann, A. T. Kearney -

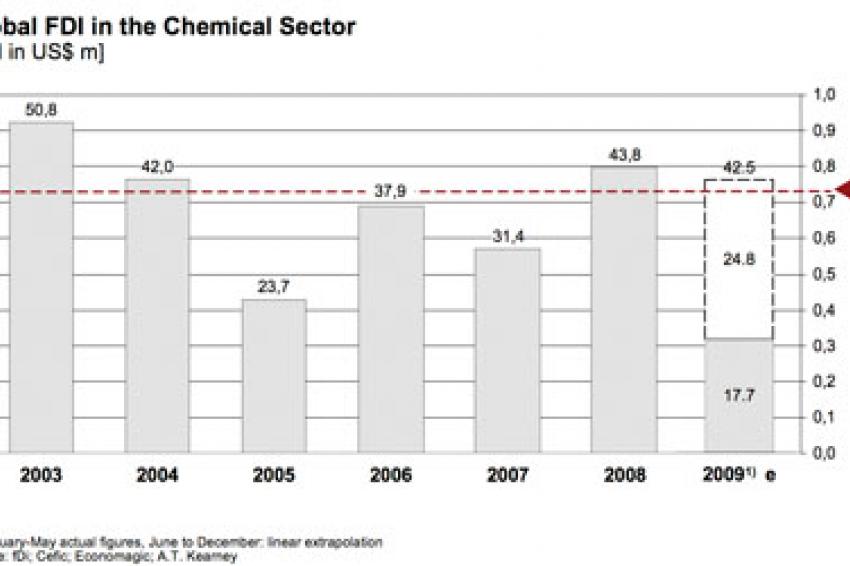

Fig. 1: At present, chemical FDI does not seem to be affected by the economic crisis

Fig. 1: At present, chemical FDI does not seem to be affected by the economic crisis -

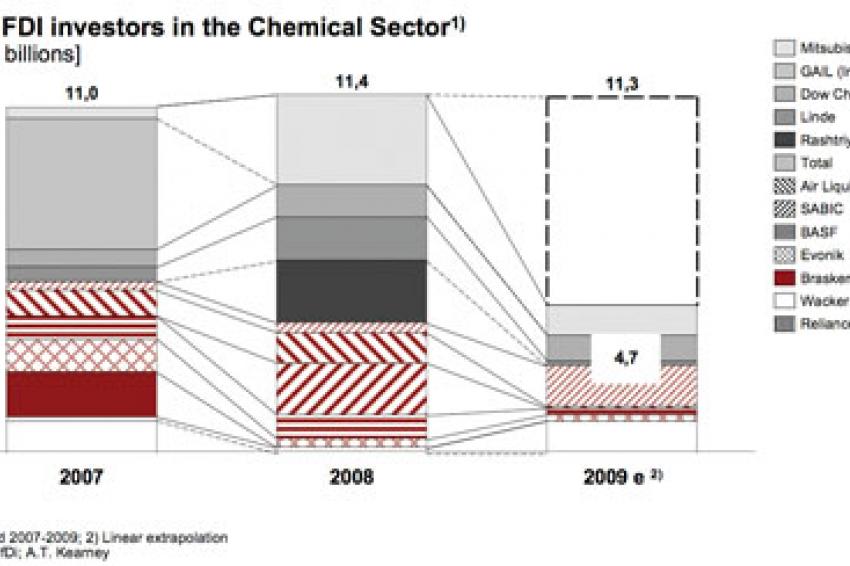

Fig. 2: Top global investors in chemicals have so far not reduced their total investments in reaction to the global downturn

Fig. 2: Top global investors in chemicals have so far not reduced their total investments in reaction to the global downturn -

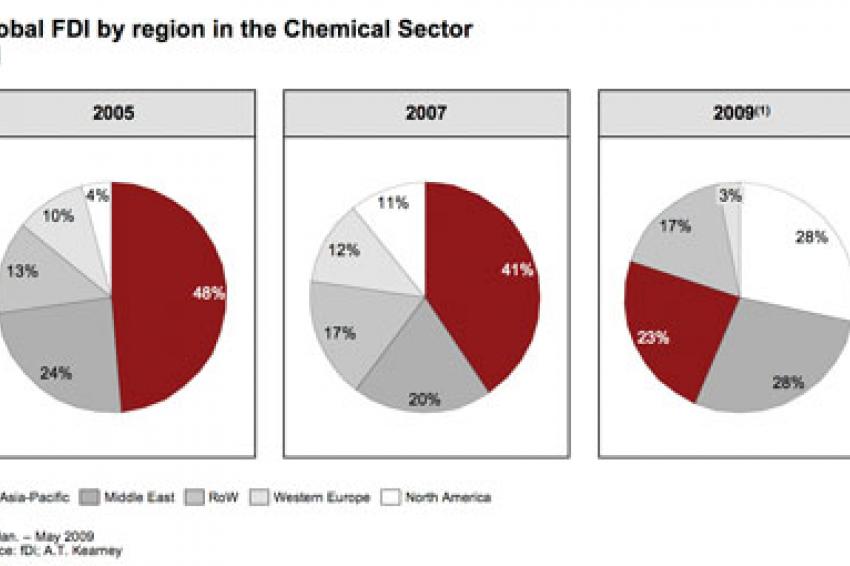

Fig. 3: Asia Pacific has continuously attracted more than 40 % of total chemical FDI, with the exception of 2009

Fig. 3: Asia Pacific has continuously attracted more than 40 % of total chemical FDI, with the exception of 2009 -

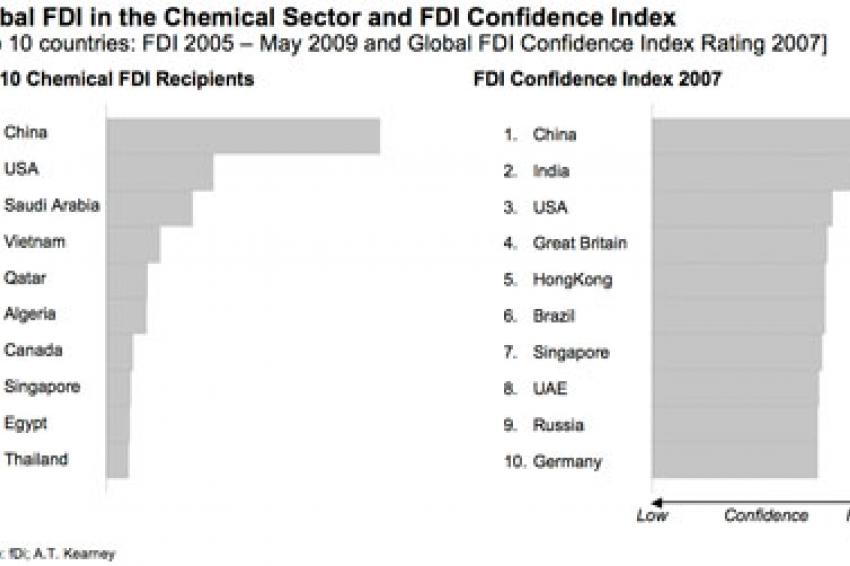

Fig. 4: Countries with a low confidence score for their general investment environment receive strong chemical FDI

Fig. 4: Countries with a low confidence score for their general investment environment receive strong chemical FDI

So far, global chemical Foreign Direct Investment (FDI) has appeared almost immune to the financial and economic crisis, with the 2008 figure being the second-highest after 2003 and the prospects for 2009 are also looking rather bright. Evidently, most companies simply cannot afford not to invest in their post-crisis market position. However, if the downturn continues, a delay in the ongoing shift of capacities toward the key destinations, Asia-Pacific and the Middle East, will become unavoidable.

The economic crisis has reduced economic activity dramatically. Many chemical manufacturers, such as Lyondellbasell, have been forced to undertake significant restructuring activities. Despite some recent recovery of demand, the continuing weakness still poses considerable challenges to chemical players around the globe. Companies such as Lanxess or Evonik have just recently reinforced their intention to further cut costs in light of their financial results for the second quarter of 2009.

FDI is a significant indicator of the financial health of an industry sector. However, in the case of the chemical sector, it doesn't paint such a clear picture. Since 2003, global chemical FDI has been fluctuating at around $40 billion per annum on average. It has been unstable and not shown any logical correlation with the growing worldwide demand for chemicals. In 2008, for instance, it reached a historical high of $43.8 billion - the second-highest value after the 2003 all-time-high investment level of around $51 billion.

This can be explained in two ways: first, by lengthy investment planning processes, and second, by long order lead times and a backlog from the boom years of 2007 and 2008. In addition, chemical players have not been in a position to halt major strategic investments, because this would have jeopardized their long-term strategic market position or put them at risk of incurring contractual penalties. Continuing high FDI figures throughout the first two quarters of 2009 indicate that this effect is still ongoing.

Asia-Pacific:

Bound for Long-Term Success

Though chemical companies shared a common path with regard to their short-term reaction to the crisis - most of them focused on actions that promoted profitability and their cash balance - strategies on how to proceed with investments differ.

Deciding on how to go forward with investments and where the strategic importance of such investments for post-crisis market positioning lies is of utmost importance. BASF, for instance, recently announced it intends to increase its investment in its Nanjing site in China and will invest $1.4 billion instead of $0.9 billion by 2011. Even though this investment may be delayed should the present crisis continue, this move clearly highlights BASF's long-term ambition in the Asia-Pacific region and in China in particular. By contrast, Lanxess has been forced to announce the postponement of the construction of a new butyl rubber facility in Singapore owing to poor demand. The $560 million investment is now scheduled to come on stream in 2014 instead of 2012.

This mixed picture is reflected by the latest announcements from equipment suppliers and EPC companies. Technip reported a sharp decline in new orders of -67 % for the second quarter of 2009 compared to the same period in 2008, although most of it resulted from reduced oil & gas investments. Foster Wheeler's global engineering and construction group, on the other hand, managed to maintain its incoming orders at the 2008 level and recorded only a slight fall in new orders of -5 %.

What has been observed in recent years is a continuous shift of investments toward the Asia-Pacific region. In 2007, it attracted more than 40 % of worldwide FDI in the chemical sector. As demonstrated by BASF's investment decision, this trend is unlikely to change due to the current crisis. On the contrary, it will most likely result in only a moderate delay of a remarkable growth story.

Among the companies that have engaged in the largest capital investments since 2003, petrochemical companies represent the largest group. Petrochemical activities of companies such as Shell, BP and Total together make up almost one third of global FDI in the chemical sector. The other major group of investors are large basic chemicals producers such as BASF, Dow Chemical, Sabic and Mitsubishi.

Preparing for the Post-Crisis World

So, what developments can be foreseen for the rest of 2009? After all, this year has already seen a handful of important investment announcements, such as Methanex's $1 billion investment in a methanol facility in Vietnam or Wacker Chemicals' $1 billion investment in a polysilicon facility in the U.S.

Assuming the first five months of this year were symptomatic of 2009 as a whole, global FDI in the chemical sector should experience only a minor drop-off. Linear progression of what was seen up to May would result in annualized investments of around $42.5 billion, indicating yet another strong year following 2008. Analysis of the actual investments of the current top global investors in the chemical sector (basis 2007 to date) reveals a similar picture: Neither can a notable decrease in FDI be detected, nor has a large number of strategic investments been significantly postponed as a consequence of the crisis.

Hence, the current economic crisis will most likely merely delay but not reverse the mid-to-long-term trend in chemical investments: These are increasingly directed either upstream toward, for example, the Middle East, to secure access to strategic raw materials, or toward emerging markets, such as those of the Asia-Pacific region, to reconfigure customer value chains. Any postponement of strategic FDI would hurt a chemical leader's future prospects and ability to benefit from a recovery of the market after the crisis.

With a share continuously in excess of 40 %, the Asia-Pacific region has over the last years been the undisputed leader when it comes to attracting FDI. Not surprisingly, China's share of $83 billion or 34 % of global FDI has been dominant. 630 out of 2,400 global investment projects recorded since 2003 were launched in China. Although in terms of total FDI the crisis has hit China and the Asia-Pacific region particularly badly, it is not expected that this will last for long given China's importance as a large-scale, end-consumer market and as the major chemical manufacturing base in this part of the world.

Despite this, however, FDI inflows into the Middle East are likely to outperform those into the Asia-Pacific area in 2009. Among other things, this can be traced back to 2007 and 2008, with global raw material prices at all-time highs thanks to the markets demand for resources, growth in global demand and political interests. The key focus of these investments - on top of investments in the oil & gas sector, not covered here - is on petrochemicals, which helps to increase local value added in the Middle East and further enhance the growing importance of the Middle East region as an export hub.

Top Chemical FDI Destinations

Riskier Than Others

Unlike FDI in other industries, chemical FDI does not necessarily follow the logic of directing capital investments toward regions in which one can be confident of realizing positive returns. For the most part, this can be put down to the fact that raw materials are often located in regions with weak economies and/or political instability. This is confirmed by A.T. Kearney's FDI Confidence Index. This index is a regular survey of global executives, conducted by A.T. Kearney's Global Business Policy Council, which takes a look at the present and future prospects for international investment flows, covering all major industries. Key regions for FDI inflows into the chemical sector, such as China and the U.S., correlate closely with the FDI Confidence Index. Both countries rank among the top three regions. By contrast, other key chemical investment destinations such as Saudi Arabia, Vietnam and Qatar were judged unfavourable or did not make it into A.T. Kearney's listing of the top 10 locations. And India, for example, a potential future powerhouse, ranked only 12th in terms of actual FDI, although it comes second in the FDI Confidence Index.