Specialty Chemicals – Ideas for Growth

Getting the Investment Mix Right: How European Chemicals Companies Can Boost Growth

-

What European Chemicals Companies Should Do to Boost Growth

What European Chemicals Companies Should Do to Boost Growth -

Bernd Elser, Accenture Strategy

Bernd Elser, Accenture Strategy -

Eike Christian Eschenröder, Accenture Strategy

Eike Christian Eschenröder, Accenture Strategy

In both the specialty and chemicals segments, companies can spur growth by yield optimization, capacity expansions with longer-term focus and new business models along the entire value chain, investment in core business – and a more risk-taking investment mindset.

As emerging market rivals continue to gain market share from their European counterparts, chemicals companies in Europe need to sufficiently target all opportunities for growth that exist, such as new growth models, including circularity, and increased investment in their core business.

In the decade before 2016, European chemicals companies lost 4 % in market share due to declining production capacities, and, at the same time, they have generated free cashflows at record levels, but have under-invested compared to their global peers.

In our view, European chemical companies are at risk of so-called “compressive disruption,” or a slow decrease in absolute profits and market relevance, due to their investment patterns - and their mindset.

For instance, European companies often anticipate a payback on fresh investment in about eight years, while those in emerging markets like China, India or the Middle East, may be willing to wait 10 to 15 years for a return.

Similarly, many European companies focus on cash optimization, and they calculate with an asset lifecycle of 30 to 50 years. This leaves plants built in the 1960s still in operation, even though companies have strong cash reserves that could be invested. As a result, some companies should push for growth to avoid becoming candidates for takeover.

Compare this to the approach of emerging-market competitors who produce with newer and often world-scale plants. These players also tend to set ambitious growth targets, such as doubling capacity in a decade or building regional and even global positions.

For these reasons, European companies need to find the right mix of investment in new growth models, such as circularity, and in the core business; the where and the how will depend on the segment and the growth model.

Specialty Chemicals – Ideas for Growth

In general, we see a potential for European companies to invest in capacity expansion, but for specialty chemicals, we see more potential for short to mid-term growth from chemical process optimization and innovation. Even increases in yield and/or small decreases in input costs can boost margins further. It comes down to the all-time classic growth approach of production optimization, which can be achieved in standard ways, such as process stabilization, optimization of operating points, lowering energy and other costs, or in less-standard ways, for instance with complete process redesign. All in all, we see significant opportunity to narrow the gap between best daily production and average production yields, which can range from 94 to 96 % for continuous chemical processes.

Other specialty companies are embracing circular models by positioning themselves for more relevance in downstream applications, such as applications that make cars more lightweight and therefore more fuel efficient. Another example is materials that make cars more durable, for instance for car-sharing companies that expect substantial wear and tear on their vehicles.

Circularity in Specialty Chemicals

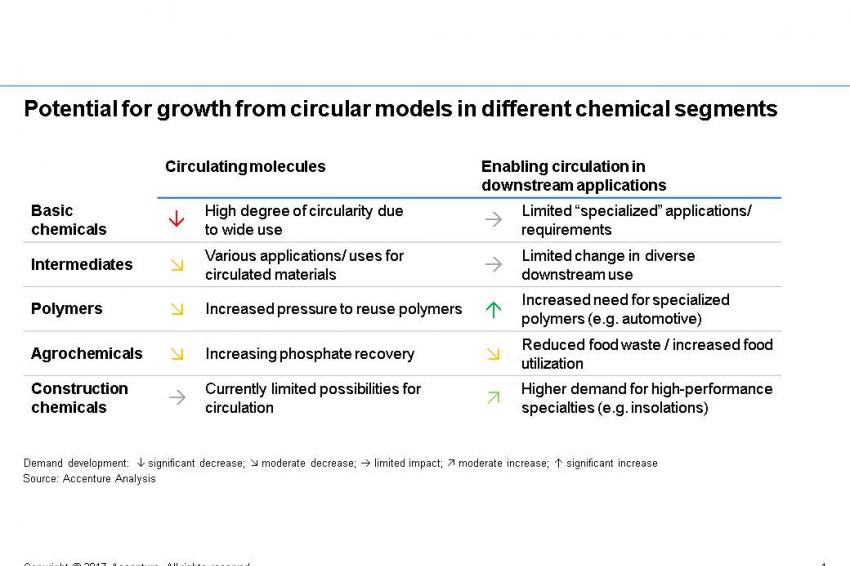

In the chemicals industry, we see two primary ways to apply circular economy business models. Like the examples described above, the first is enabling circular models in downstream applications. The second is recirculating actual molecules. Both are, in part, driven by regulatory and consumer pressure to reduce impact on the environment.

We see strong potential for growth from circular models and have even gone so far as to say that enabling circular models in downstream industries is the single most important growth opportunity for the chemicals industry in the years to come. But we stress that the impact will be starkly different on each market niche.

As indicated in Figure 1, enabling downstream applications will mean an increased need for specialized polymers, for instance in the automotive industry, as well as higher demand for high-performance specialty construction chemicals, including foams for insulation. Such chemicals will be needed in greater quantities for more energy efficient building.

In agrochemicals, however, we see circularity models potentially having the opposite impact on growth for specialty chemicals: When molecules can be recirculated, for instance when more phosphates can be recovered, demand will decline. Or, when reduced food waste and higher food utilization by large producers takes place downstream, demand for agrochemicals will stagnate or even decline.

Given the differing impacts, companies must face the challenge of finding – and investing in – the right circular niche.

To visualize opportunities, to better analyze the trends and to find niches to explore, it’s important to think in terms of the entire value chain. Co-creation events are one possible format for fostering discussion with internal and external experts who represent the value chain. Bringing a company’s own salespeople, startups, and academia into such exercises can deepen the inquiry as well.

Commodities – Growth Scenarios

In the commodities segment, the market continues to be driven by supply – demand balance and price. Many commodities seem to experience a peak in terms of profitability – a favorable supply-demand balance, faster than expected demand growth and selected outages and force majeures contributed to an expansion of profit margins.

Here companies in established markets need a clear mindset change about time horizons. As mentioned before, emerging market players often accept longer payback periods for their investments. Since established players are hesitant to wait out longer horizons, they often don’t invest at all. It’s a question of risk profiles. Generally speaking, established companies are more risk-averse in their investments close to home and in beneficial environments.

Our recommendation to European chemicals companies is to assess whether moving closer to the risk profiles of companies in emerging markets makes sense, even though doing so means standing up to shareholder short-termism. Companies will have to re-evaluate investment decisions and prioritize those that can have a strong impact from a global perspective, even if such decisions ruffle feathers on a local basis or require a re-think of resources committed to the pursuit of new molecules.

We understand European companies face many internal barriers, but they have already shown their capacity for change. Previously they adapted their expectations about investment time horizons to make them shorter; now it’s time to move in the other direction on that same continuum. We believe it’s time for European chemicals companies to step up and take the opportunities for growth that are available to them, even if it takes longer to realize a return.

Over the long-term, these efforts need to be combined with business-model innovation that brings companies closer to their customers so they can become providers of solutions and services, and not just raw materials.

This links back to the idea of circularity. Since many commodity chemicals are solvents, we can imagine chemicals companies as providers of solvents “for rent” that they, in turn, reuse or recycle. Indeed, we estimate that up to 60 % of the molecules provided by the European chemical industry to customer industries and end-users can be re-circulated if certain conditions are met. Yes, it’s a move away from clearly established chemical uses, but the logic behind solution chemicals is compelling.

All in all, the biggest long-term gains are to be made in the commodity chemicals segment. We strongly encourage European companies to prepare to play out the circularity advantage in both commodity and specialty chemicals over the long-term – while also expanding capacity and innovating processes in specialty chemicals for a faster impact in the short and mid-term.