Chemical Distributors Can Be Successful Through Change

How the Chemical Distribution Sector Can Navigate Market Downturns and Transformation Trends

-

© photoschmidt - stock.adobe.com

© photoschmidt - stock.adobe.com

New buzzwords such as polycrisis and permacrisis are increasingly circulating, highlighting that we have grown accustomed to facing multiple crises since the 2000s, including 9/11, the financial crisis, debt crisis, refugee crisis, and the ongoing Covid-19 pandemic. However, the challenge now is that several crises are converging over a longer period, making it more difficult to assess variables such as inflation, energy prices, geopolitics, and the possibility of further pandemics. Recent difficulties faced by individual banks have only added to the existing tensions. Despite the ongoing uncertainty, we can observe a decline in economic growth, greater volatility in supply chains, and a partial reversal of globalization. In this context, “business as usual” is not an option, even for chemical distributors who play a significant role in the global economy.

In recent months, the automotive and manufacturing industries have been primarily focused on “restructuring” and “crisis management” due to rising energy and purchasing costs, as well as changes in sales markets. However, chemical traders and distributors — who are considered to be less vulnerable to price and cost increases and therefore more robust and crisis-proof — have largely been excluded from these discussions. Instead, chemical distributors are increasingly becoming occupied with transformational trends that will contribute towards their development: What do increasing economic pressures from suppliers and customers mean for portfolio management? Do mergers and acquisitions (M&A) still drive growth? What opportunities does the next wave of digitalization measures offer? Do opportunities arise from the trending topic of ESG (Environment, Social, Governance) and from new regulatory requirements? How can the chemical distribution industry attract young and specialist workers to address the impending shortage of skilled labor in the years to come?

Changes in Production and Portfolio

Chemical markets are experiencing a lot of activity, with expectations for high prices on the supplier side as producers are forced to pass on their rising energy and raw material costs. Whilst inflation slowed down in the first quarter of 2023, price stability is not expected to return for the foreseeable future. Moreover, recent years have shown that supply chains are prone to disruption for various reasons and companies should make provisions for failure. The production landscape is also changing as a result of cost considerations, with a trend away from Europe and towards the Middle East and the USA. Geopolitically, China, the current leading chemical production location, is being increasingly questioned, and efforts to find alternative locations are ongoing. Given this situation, it is advisable to conduct a risk assessment of current suppliers and clients, as well as to increase flexibility in order to reduce over-dependence. Regarding the customer side of chemical distribution, it is expected that passing on higher prices will become more challenging due to shrinking margins in many sectors, particularly in the manufacturing industry, and a gloomier macroeconomic outlook. This puts distributors in a “sandwich position,” facing pressure from both suppliers and customers. In this context, it is advisable to assess the customer portfolio for default risks and adjust commercial terms accordingly. In the long term, it may be sensible to reallocate the portfolio and shift towards less volatile sales markets.

Transactions and Digitalization on the Rise

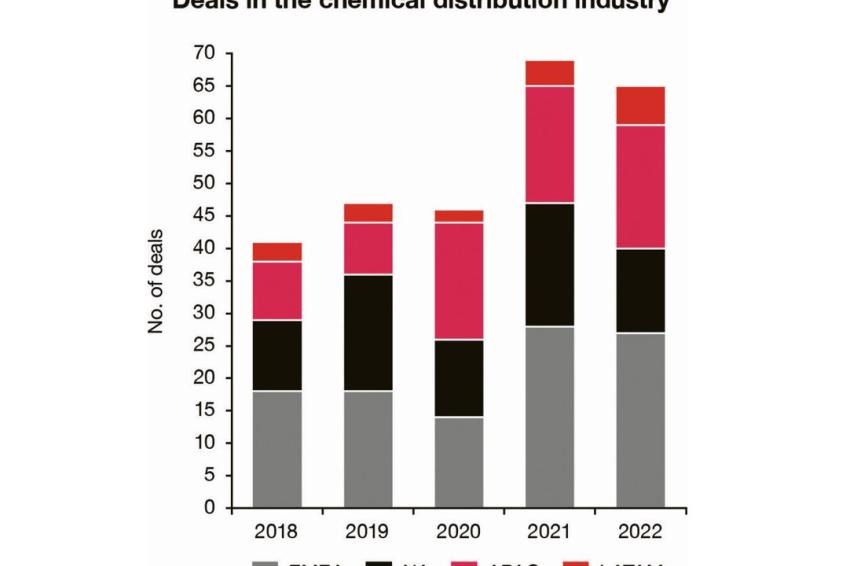

The number of transactions in chemical distribution reached record levels in 2021 and 2022 despite a myriad of crises, and M&A activities were regularly used as growth drivers or to streamline portfolios. Due to continually fragmented markets — particularly in Asia — we expect a further increase in deals in the medium to long term, especially when more and more financial investors come out of the defensive. Here, it is important to start looking for targets early in order to benefit from correct valuation levels in the short term and not to miss the boat in the medium to long term.

The latter also applies to digitalization, which chemical companies have been adapting to for many years. We are currently observing developments in the direction of digital trading platforms and ecosystems, which pioneers in the agrochemical and healthcare industries are driving forward with the aim of retaining customers through comprehensive technical solutions (end-to-end) and a customer experience geared to private consumer habits. The use of customer and product data also opens up new opportunities for value creation, whereby companies should bear in mind that part of the required digital competences must be built up in-house. Given the labor market situation, this is no easy undertaking.

ESG and Skills Shortage as Focus Topics

In the past, activities related to ESG and regulation were often viewed as mere “tick box” exercises. However, a new opportunity is emerging for chemical distributors, given their role as intermediaries between producers and end-users. The chemical industry provides a wealth of information about planned applications and associated products, which can be leveraged for ESG initiatives and the development of environmentally friendly products. In this way, distributors can offer advisory services for sustainable products alongside trading activities. Additionally, there is potential for consultation on compliance with regulatory requirements and reporting obligations, which can be facilitated by utilizing available product data, such as origin and carbon footprint information.

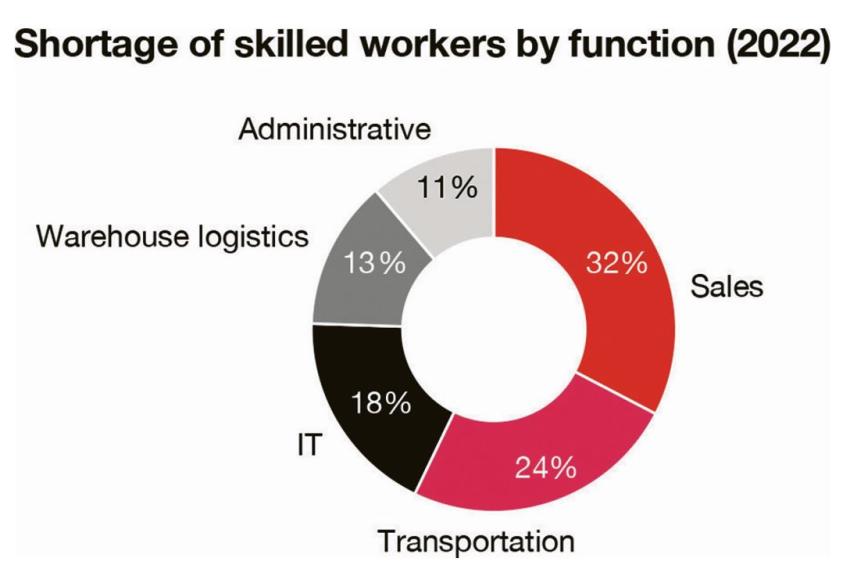

Last but not least, chemical distributors are also exposed to the shortage of skilled workers. It is important to secure the workforce today that will be needed for the work of tomorrow. Currently, the image of chemical distribution is often perceived as traditional, which may not appeal to younger, digital-savvy workers. Moreover, companies have been slow to consider New Work requirements such as demonstrating the company’s purpose or providing mobile work devices to increase flexibility in working time and location. There is a definite need for action to attract the workers who will be necessary for the tasks that lie ahead in the upcoming years.

In conclusion, chemical distribution is undergoing a series of developments that will bring about transformative change for companies. Amidst changing geopolitical conditions, distributors must question their own footprints and adjust their business models to address issues such as inflation, unstable supply chains, and differences in target industries, like the automotive industry.

Additionally, trends in strategic areas including M&A, digitalization, ESG, and recruitment cannot be disregarded or addressed in isolation. To achieve a successful transformation, we recommend a holistic approach that takes into account all relevant fields of action.

Volker Fitzner, Partner Global Chemicals Lead, PWC Deutschland, Frankfurt am Main, Germany

Christian Eilinghoff, Director Integration & Divestments, PWC Deutschland, Hamburg, Germany

-

Deal numbers in the chemical distribution industry were at an all-time high in the past two years. | © PWC

Deal numbers in the chemical distribution industry were at an all-time high in the past two years. | © PWC -

Chemical distributors state that skills shortages affect sales teams the most; IT experts are also hard to find but are the key to driving digital agendas (graph numbers include rounding differences). © PWC

Chemical distributors state that skills shortages affect sales teams the most; IT experts are also hard to find but are the key to driving digital agendas (graph numbers include rounding differences). © PWC

-

Christian Eilinghoff, PWC Deutschland © PWC

Christian Eilinghoff, PWC Deutschland © PWC

-

Volker Fitzner, PWC Deutschland © PWC

Volker Fitzner, PWC Deutschland © PWC