Chemicals M&A Review 2022 and Outlook 2023

Out of a Storm, the Chemical Industry Could See Resurgence in 2023

-

The combination of high interest rates, supply chain bottlenecks and geopolitical instability saw both the number and value of chemical M&As take a significant hit throughout 2022. | © Murrstock - stock.adobe.com

The combination of high interest rates, supply chain bottlenecks and geopolitical instability saw both the number and value of chemical M&As take a significant hit throughout 2022. | © Murrstock - stock.adobe.com

2021 was historic for chemical M&As, it was a record-breaking year in terms of total value of deals. Therefore, it was expected that 2022 would only build upon this. However, the Russia-Ukraine war initiated on Feb. 24, 2022, plunged the world into financial chaos breeding uncertainty and unpredictability. Furthermore, chemical supply chains and feedstocks were majorly disrupted due to political unrest after just recovering from Covid lockdowns. This led to a global energy crisis and a steep rise in inflation which touched double digit figures in most countries. Interest rates were then subsequently raised to combat inflation. The combination of high interest rates, supply chain bottlenecks and geopolitical instability saw both the number and value of deals take a significant hit throughout 2022.

For the first time EU chemical imports exceeded exports in volume and value. This coupled with a trade deficit of €5.6 billion for Q1 2022 for Europe outlines the sheer gravity of crisis plaguing the EU. Therefore, the chemical industry has a myriad of long-term crises to solve, causing the ratings agency Moody’s to downgrade its outlook for the global chemical industry from stable to negative.

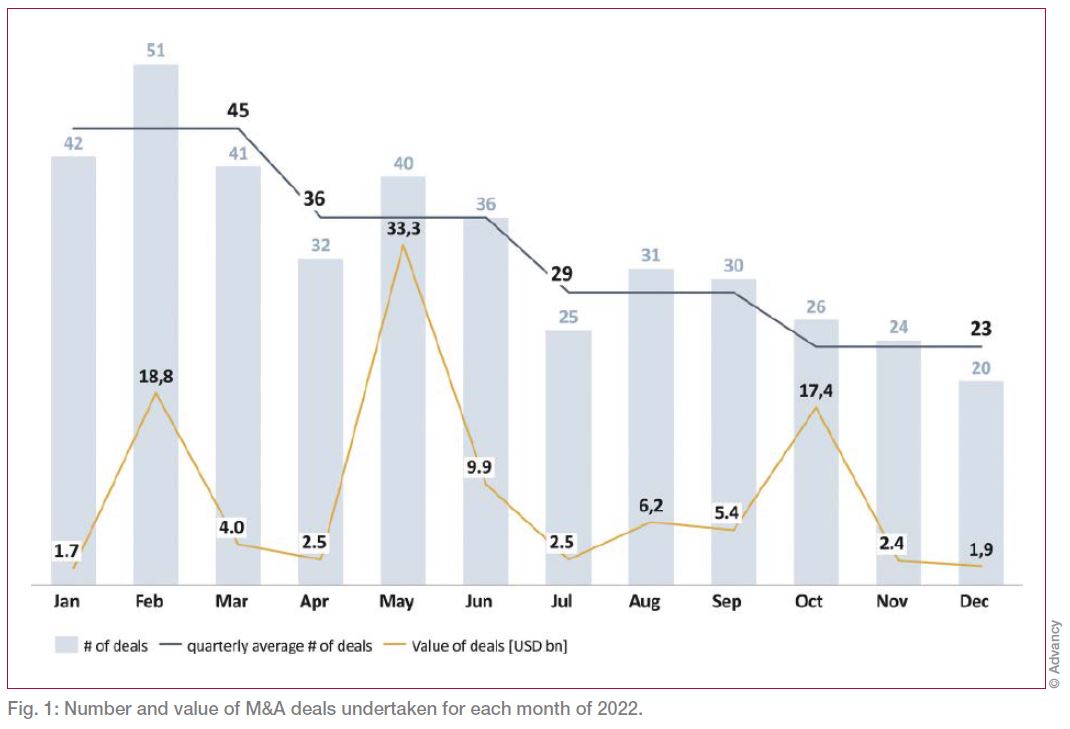

Declining Deals in 2022

Companies have faced a challenging macroeconomic environment worldwide since the 2008 Financial Crisis. Now, financial issues such as rising inflation, rising interest rates and a global economic recession looming on the horizon have significantly affected the deals which have taken place since the Covid-19 restrictions were lifted.

Overall, around 400 deals took place in 2022 with a total value of €100 billion. Europe led the maximum deal value, driven by the mega deals between Firmenich and DSM (€19 billion), DSM and Advent/Lanxess (€3.9 billion), Perstorp and Petronas (€2.3 billion), DSM and Avient (€1.4 billion) which were announced in 2022. DSM decided to focus on their core-competency of high-end nutrition so have undertaken a major divestment in other areas, a trend representative of the last years. The maximum deal value peaked in May ($33.3 billion) which coincides with Q2 2022 when these mega deals took place. The majority of M&As were below $1 billion as raising finance for deals was difficult in the tumultuous economic climate. Fig. 1 shows the steady decline in the number of deals made, along with the total value for each month throughout 2022. There was a clear peak in May which corresponds to the large divestiture of DSM.

Q1 2022 will be remembered for the initiation of the Russia-Ukraine war. This redefined the face of the global market and chemical supply chain especially in Europe, which experienced soaring energy and feedstock prices, as key economies such as Germany were so dependent upon Russian gas.

The European chemical industry is extremely energy intensive, hence the significant increase and uncertainty in energy prices puts the European countries at a competitive disadvantage compared to non-European global players. Therefore, companies are rather focusing spending their capital on mitigating against the high energy prices than investing into M&A for growth.

Russia was the leading supplier of gas into Europe, which has fostered a dependency due to the pipeline system. After the Russian economic sanctions, energy costs in Europe raised significantly, along with fuel prices. European gas and electricity prices have increased by 115% and 237%, respectively, since the start of the war. As a wholesale gas benchmark, Dutch TTF averaged 7-8 times higher than the US Domestic natural gas prices, handing US companies a major competitive advantage over those in Europe. This created a huge uncertainty in the market which led to a subdued demand in M&A deals in Q1 2022.

Inflation reached an all-time high of 8.6% in the Eurozone by Q2 2022. As a result, the European growth forecast was reduced to 0.6%. Therefore, as a reactionary and cautious move to control inflation, the European Central Bank drastically increased interest rates. The deposit facility increased to 2%, the refinancing rate to 2.5% and the marginal lending to 2.75%; a 14 year high. High interest rates mean raising finance or capital is much more difficult, therefore lowering the leverage of Private Equity (PE) companies for M&As. Furthermore, in the US, the Federal Reserve also increased the interest rate for the 7th time in a year, taking it to a level of 4.25% to 4.5%, its highest level in 15 years.

Another blow to the M&A market in 2022 was the weakening and volatility of global currencies. The euro suffered massive depreciation against the dollar. It saw a maximum of 1.1464 against the US dollar on Feb. 4, 2022, and a minimum of 0.9565 against the US dollar on Sep. 28, 2022, with an average of 1.0531 for the year. This volatility caused uncertainty and resistance to make cross financial zone transactions. In fact, the vast majority of deals were completed within the same currency zone, due to additional costs and unpredictability, as outlined in fig. 2.

Primarily deals happened in the same region. 75% of deals by buyers in North America (NAM) were from companies based in NAM and only 18% went to Europe for acquisitions. Similarly, European companies accounted for 55% of the deals that happened within Europe. Transcontinental deals between different continents saw a decline due to rising interest rates, slowing economic growth and currency fluctuations.

China, the world’s largest chemical economy, has been suffering from its strict implementation of Covid restrictions. China rolled out mass testing, quarantines and strict lockdowns which has severely reduced its overall economy growth rate figures compared to earlier years. The original target growth figure for 2022 set by the Chinese government was 5.5%. However, the actual growth was only 4.4%, a significant reduction driven by many closures and idle plants in the chemical industrial space.

Impact of Environmental, Social and Governance Issues

The growing weight of environmental, social & governance (ESG) goals is a major factor for decision making in the chemical industry. New laws and legislations are being passed at an increasing rate, which only increases the importance of molding business strategy around compliance to these laws. For example, the European Climate Law outlines a legally binding target of net zero greenhouse emission by 2050. Similarly, the USA have announced an updated target to achieve a 50-52% reduction compared to 2005 levels in an economy wide net greenhouse gas emission by 2030.

The majority of manufactured goods have roots in or are somehow linked to the chemical sector. Subsequently, chemical companies are under significant pressure to push the frontier of decarbonization strategy and technology development to reduce emissions. And of course, this applies to all players throughout the whole value chain. The increased importance of ESG issues spurs companies to explore M&As with the aim of acquiring businesses which can accelerate the achievement of sustainability goals, divest in their own business areas which are the least sustainable, or acquire emerging technologies to help meet the environmental goals.

PE Firms and Corporate Investors

The types of companies engaged in M&As can be broadly categorized into two brackets: chemical companies and PE firms. Out of a total of ~400 deals in 2022, only 20% involved a PE firm buying a chemical company, however this accounted for almost 36% of the total value which took place in 2022. This shows the tendency for PE firms to leverage higher value deals compared to deals solely completed between chemical companies.

PE firms help sculpt the M&A landscape. They often follow a buy and build strategy; buy a well-positioned platform company and then make multiple smaller acquisitions with key synergies in the weakest areas which helps to reduce the firm’s average acquisition cost and delivering enhanced asset value. PE firms look for the highest performance or growth potential in companies so they can build upon this with key acquisitions and then later sell the company for a much higher value and EV/EBITDA multiples. This occurs typically over a 5–8-year timeframe.

The main driver behind M&As performed by PE companies contrasts with the reasoning behind M&As for chemical companies. Chemical companies pursue M&As in order to: consolidate or strengthen their position in active segments; grow or refocus their portfolio; fix certain financial or cash flow issues; remove underperforming segments; or expand their portfolio into new and profitable areas. However, M&As performed by both PE and chemical companies attempt to create additional value by strengthening key business areas or eliminating weaknesses.

Outlook for 2023

Higher energy prices are likely to continue, especially in Europe. To start getting cheaper gas, it would take at least 2-3 years as countries need to build permanent LNG terminals and strike deals. This, combined with the implementation of the European Climate Laws will require vast funds and investment to adjust, made more difficult without an immediate return on investment. Therefore, many smaller companies will find it hard to adapt and subsequently might see large scale and broad restructuring and consolidation across the chemical industry.

Chemical companies in Europe are facing material shortages along with the energy crisis creating disruption across the supply chain which is expected to carry over to the first half of 2023. Therefore, companies will try to create resilience within their own supply chain and look for deals which can bolster their core competencies.

The carbon neutral targets set for 2050 make it essential for companies to reduce their Scope 1, 2 and 3 emissions. Therefore, many companies will consider M&As which would help reach these goals. The Inflation Reduction Act seeks to attract companies to work on addressing climate change by increasing investments in renewable energy, with a total fund of $369 billion. Such schemes exert even more pressure on European companies and will accelerate M&As in this area.

The rising cost of production forces European companies to spend more money on innovation and continuous evolution to stay competitive and achieve higher growth in key areas. Therefore accelerating a detailed search to find such smaller companies with synergistic technologies to transform companies’ processes to be more cost effective and sustainable.

Companies will also look to shift their production operations overseas to the US, due to abundant gas and energy reserves, attractive tax breaks and a predictable political and jurisdictional environment. With production in China currently slowing down and demand also suffering, many chemical companies in APAC might also consider moving towards the US for setting up new bases in the future if falling exports to China continue.

The handful of deals still in the pipeline will likely be announced soon. We anticipate the planning of deals throughout Q2 which will come to fruition in the second half of 2023 after careful negotiations and due diligence. Furthermore, increased M&A activity is likely due to the lull in such activities towards the end of 2022 with many deals waiting for a more stable climate. Some release on energy prices could be seen with prices having fallen and new (temporary) LNG terminals are opening in Europe. This, coupled with China easing its Zero Covid policy restrictions, will induce more certainty and predictability throughout the global market. Considering these factors, we predict a tentative first half of 2023 for M&A deals which is likely to see rise in the second half of 2023, as forecasts become more predictable and currency volatility steadies. This could happen especially in the divestiture area as large companies sell off non-core competency business sections to focus on their most profitable sections. PE companies or other chemical companies could then start to build new synergies in areas more aligned to their own expertise.

Sébastien David, Senior Partner, Advancy, Paris, France, and

Gunter Lipowsky, Managing Director, Advancy GmbH, Frankfurt am Main, Germany

-

Sébastien David, Advancy | © Advancy

Sébastien David, Advancy | © Advancy

-

Gunter Lipowsky, Advancy | © Advancy

Gunter Lipowsky, Advancy | © Advancy