Inflation and Uncertainty in European Plastics Industry

10th PIE Market Survey

While Europe's energy crisis is easing, inflation and general uncertainty continue to shake the European plastics industry, according to the latest Plastics Information Europe (PIE) survey. Nearly half of respondents said their company's performance in the first half of 2023 was worse than in the second half of 2022, with only 28.7% seeing some improvement. This follows a trend from last year, when almost half of respondents reported worsening performance in H2 2022, with only 26.7% reporting an improvement.

Companies based in France, Spain, Portugal, the UK and Ireland did not report a downturn in business, while most companies in Benelux, Italy and Central and Eastern Europe said business had weakened, suggesting regional irregularities. Plastics recyclers have been particularly hard hit by falling prices for virgin plastics, with 70% reporting less business in H1 2023 compared to H2 2022, and none seeing an improvement.

-

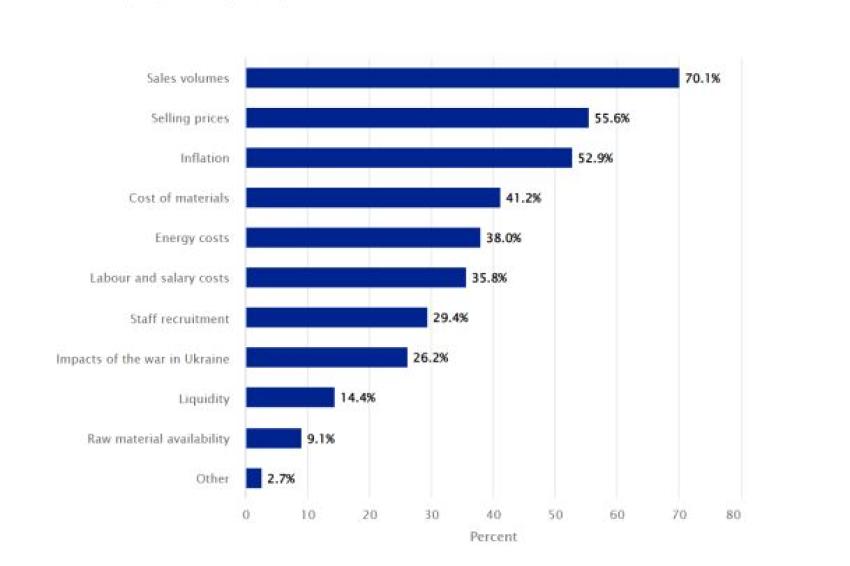

Main concerns for respondents represented by percent. Multiple responses were possible. © Plastics Information Europe

Main concerns for respondents represented by percent. Multiple responses were possible. © Plastics Information Europe

Future Outlook and Investments

While H1 2023 fell short of expectations, the industry remains cautiously optimistic, with over 29% of respondents expecting an upward trend in H2 2023 and the majority not expecting a decline. European sales forecasts are cautious, with Spain, Portugal, and the Benelux showing strong optimism, while plastics recyclers and resin producers lack positive forecasts.

In the face of economic pressures, some 31% of companies surveyed reduced budgets, while only 19.7% increased spending compared to the previous year. Investment varied by region, with Southern Europe showing higher activity and the Benelux/Nordic regions showing lower investment. Plastics recyclers were the most eager to invest, while those involved in the trade and distribution of plastics products were more cautious.

Staff Remains Unchanged

Despite ongoing labour shortages, the plastics industry in Europe experienced minimal changes in staffing levels. The majority of companies surveyed reported stable staffing levels during the first half of the year. While 19.3% of companies hired new staff, 26.2% reduced their workforce.

In the Iberian Peninsula, 40% of respondents increased their headcount, while there was no growth in Southeastern Europe, Italy, German-speaking Europe, and CEE. Companies with more than 500 employees tended to make redundancies (38%), while those with less than 20 employees largely maintained the status quo (87.5%). Uncertainties about inflation and global markets led to the postponement of staffing decisions.

Expectations for the second half of 2023 show that 65.7% aim to maintain current headcount levels, with an increase in the number of companies anticipating layoffs (19.3%) and a decrease in those planning new hires (15%) compared to the previous survey.

-

Plastics sourcing strategy displaying the acquisition methods for purchasers in the plastics industry by percent. © Plastics Information Europe

Plastics sourcing strategy displaying the acquisition methods for purchasers in the plastics industry by percent. © Plastics Information Europe

Management Concerns and Changing Sourcing Strategies

In 2022, managers were mainly concerned about rising energy costs, but in 2023, instability in the sales market became more prominent. Concerns shifted to low sales volumes (70%), selling prices (55%) and inflation (53%) in H2 2023, while material and labour costs became less of a focus.

In the face of fluctuating international forces affecting prices, plastics processors are adapting their ordering practices, with over 60% of respondents changing their purchasing strategies, 9% using the spot market exclusively, and some 46% adjusting their sourcing methods, including supplier expansion and bundling.

In the midst of wars, inflation, recessions, and uncertain weather, the majority of managers (86%) are still struggling to recover, with more than half expecting a return to pre-pandemic levels only next year. A small percentage expect a later recovery or none at all, and a significant proportion are uncertain. In short, the prevailing uncertainties have had a significant impact on companies' outlook and timeframe for recovery.

Contact

Kunststoff Information Verlagsgesellschaft mbH

Saalburgstr. 157

61350 Bad Homburg

Germany

+49 (0) 6172 9606-0

+49 (0) 6172 9606-99