Peter Pollak on the World of Fine Chemicals

26.10.2011 -

-

Dr. Peter Pollak, Fine Chemical Business Consultant

Dr. Peter Pollak, Fine Chemical Business Consultant -

In his book “Fine Chemicals — The Industry and the Business,” Dr. Peter Pollak provides a look at one of the most challenging segments of the modern chemical industry.© Maxim_Kazmin - Fotolia.com

In his book “Fine Chemicals — The Industry and the Business,” Dr. Peter Pollak provides a look at one of the most challenging segments of the modern chemical industry.© Maxim_Kazmin - Fotolia.com -

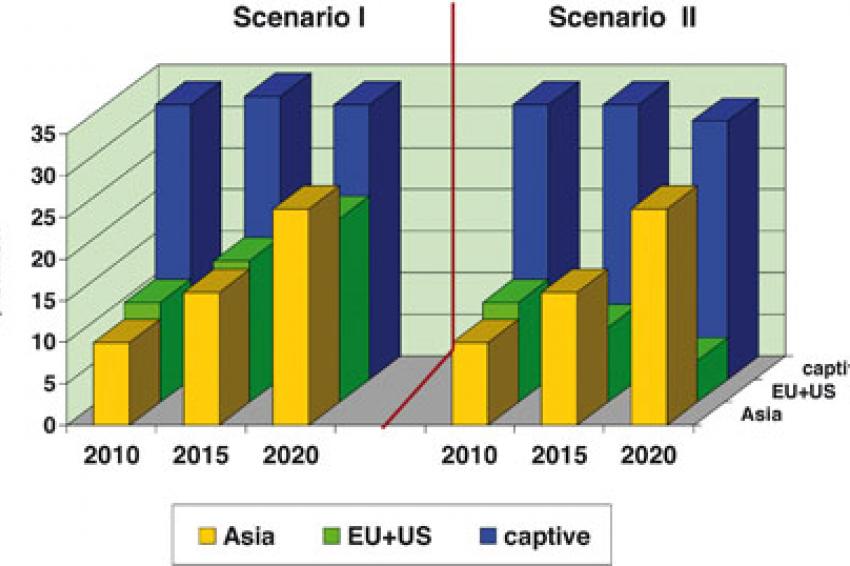

Figure 1

Figure 1 -

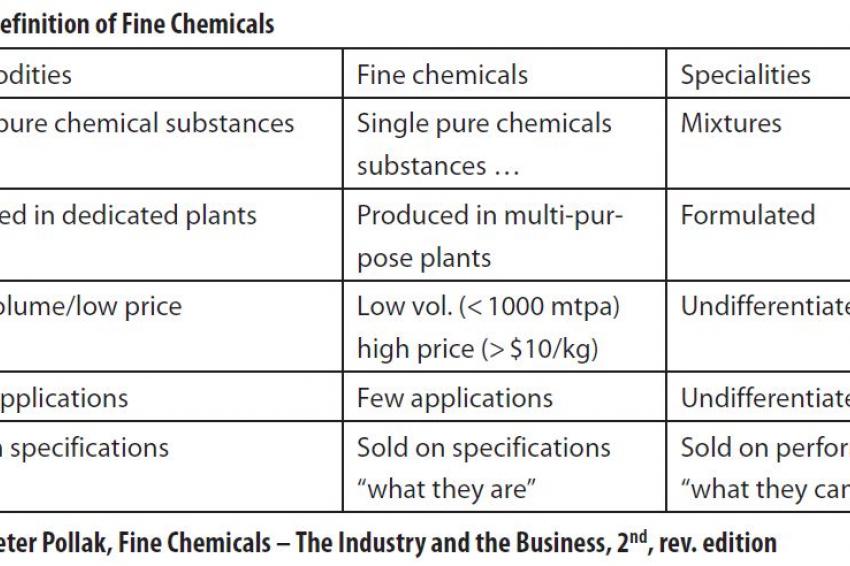

Table 1

Table 1

In his book "Fine Chemicals - The Industry and the Business," Dr. Peter Pollak provides a comprehensive view on one of the most challenging segments of the modern chemical industry, and a practical guide for succeeding in the multibillion dollar fine chemicals business.

The second edition, which was published by Wiley in May, takes developments in the field since the first edition was written into consideration, including substantial updating of facts and figures; new chapters on M&A and biosimilars; and a discussion of the offer/demand development of the modern pharmaceutical fine chemicals industry. Before becoming a consultant in fine chemicals business and a board member of several fine chemical companies, Pollak spent more than 30 years at Lonza.

CHEManager Europe asked him about the development and the current and future challenges of the global fine chemicals industry.

CHEManager Europe: Dr. Pollak, you write in your book that all fine chemicals, in general, are used to make specialty chemicals. Is there a more detailed definition that helps to understand the importance and value of fine chemicals?

Peter Pollak: Fine chemicals are complex, single, pure chemical substances. They are produced in limited quantities - up to about 1,000 tons/year - in multipurpose plants by multistep batch chemical or biotechnological processes. They are described by exacting specifications, used for further processing within the chemical industry and sold for more than $10 per kilo.

The class of fine chemicals is subdivided on the basis of the added value - building blocks, advanced intermediates or active ingredients - and the type of business transaction, namely standard or exclusive products.

The pharmaceutical industry, which is the largest user of fine chemicals, distinguishes between drug substance, which is the active ingredient, a fine chemical, and drug product, which is the formulated, finished drug, a specialty.

The fine chemicals industry is very fragmented...

Peter Pollak: Yes; globally, there are 2,000-3,000 fine chemical companies, extending from small, "garage-type" outfits in China making just one product, all the way to the big, diversified companies. Among the top 20, 17 are divisions of large chemical or pharmaceutical companies like Albemarle; BASF; and Boehringer-Ingelheim, and there are only three pure players. In terms of geography, nine of the top 20 are located in Europe, which is recognized as the cradle of the fine chemical industry. An example in case is the world's No. 1 company, Lonza, headquartered in Switzerland. The second largest geographic area is Asia, housing seven of the top 20. With four large companies, the U.S. ranks last. The combined revenues of the top 20 reached about $10 billion in 2009.

Traditionally a European and North American business, the fine chemicals industry is globalizing at a fast pace. What are the driving forces behind this globalization?

Peter Pollak: In the fine chemical industry, globalization mainly refers to the impressive foray of Asian, especially Chinese and Indian companies. In simple terms, their success is based on their "high skill/low cost / bright future" competitive advantage. "High skill" not only refers to the education of managers and scientists (not to mention the sheer number of university graduates), but also to the quality of the fine chemical plants, corporate governance, safety, health and environment standards, regulatory compliance, etc.

Auditors from the leading Western pharmaceutical companies agree that the top tier Chindian (Chinese and Indian) companies' standards are in line with those of their Western competitors. "Low cost" not only means low wages for the plant operators, but also low construction costs of Chindian fine chemical plants.

A dramatic example is the cost of the pivotal piece of equipment of every multipurpose fine chemical plant, the reaction vessel. The unit cost for a fully installed reactor ranges from $10 milllion/m3 for a reactor installed in a Western Big Pharma company, to $1 milllion/m3 for a Western plant, and $0.1 milllion/m3 in a Chindian plant.

"Bright future" means that the demand for the two main outlets for fine chemicals, namely pharmaceuticals and agrochemicals, enjoy "double digit percent annual growth rates" in the Eastern hemisphere, whereas it has decreased to "low single digit percent annual growth rates" in the Western part of the world. The main beneficiaries of this surging demand obviously will be the domestic suppliers in Asia.

Most fine chemicals are produced captively or under an exclusive contract for a single customer, especially when it comes to fine chemicals used for pharmaceuticals. What kind of pressure does the consolidation of the customer base (e.g. pharma) put on fine chemical companies?

Peter Pollak: The increasing purchasing power of the life science industry in general and Big Pharma in particular leads to more and more stringent clauses in the supply contracts for fine chemicals.

These comprise not only the pricing, "cost transparency" and pre-fixed yearly "cost improvements" have become almost standard elements, but are extended to currency clauses - a particular problem for the Swiss industry, suffering from a grossly overvalued franc-, flexibility regarding production volumes and timing of production campaigns, obligation to source raw materials from a given supplier, share know-how with competitors, etc.

The pharmaceutical industry itself is under pressure by governmental drug price reductions, patent expirations and low innovation rates. What does that mean for the fine chemical producers and custom manufacturing organizations?

Peter Pollak: Most of these developments have an unfavorable effect both for the fine chemical industry in general and custom manufacturers in particular. Although the incidence of the cost of the fine chemical used for a particular pharmaceutical is small, typically less than 5%, price reductions on the finished drug invariably lead to requests for price concessions. More than $100 billion of drug sales revenues will be affected by patent expirations over the next few years. When proprietary drugs plunge over the patent cliff and become generic, prices start to collapse immediately and typically end up at a level of about 20% of the original price of the APIs affected.

Consequently, Western suppliers are driven out of business in many cases. New drug launches have fallen from an all time high of 51 in 1997 to about 20 per year at present. Thus, not even all of the top 20 pharma companies manage to launch one new product per year. Moreover, as many new drugs either are me-too drugs, showing only marginal improvements, or treat rare diseases, also the volume requirements decrease. The unpleasant consequences for the CMOs are fewer business opportunities, both quantitatively and qualitatively.

There is, however, also a piece of good news. As part of restructuring programs implemented by most life science companies, the axiom of captive manufacture of fine chemicals being a core activity is abandoned. The practical implications are plant divestments or even shut-downs - and more outsourcing, both of drug substance and product. The chips are out as to which extent the increase in outsourcing will compensate the negative developments mentioned.

Pfizer, with sales of $50 billion in 2009 is the world's largest pharma company. Its top selling product, with a revenue of $11.4 billion, is the cholesterol-lowering agent Lipitor. Patent expiries in Canada and Spain already caused a sales reduction of 21% in Q2 2011. The situation will worsen when generic versions will also be on sale in the U.S. as of November. According to Bloomberg, Pfizer will suffer from patent expiry of 18 more drugs by 2015. They generated 60% of revenues in 2009!

What is your estimate for the size of the fine chemicals market in the future depending on different growth scenarios?

Peter Pollak: The future growth of the fine chemicals market depends mainly on the growth of the pharmaceutical industry and the trend in outsourcing. The development of the Western fine chemicals market alone depends on the globalization. Using optimistic/pessimistic assumptions for the three variables the following API growth scenarios result (fig. 1).

Due to the impact of reduced growth of the pharma industry on the one hand, and increased outsourcing on the other hand, the value of captive API production within the pharma industry will remain flat at about $33 billion / year throughout the 2010-2020 period.

In scenario I, the API production in the European and U.S. fine chemical industries will continue to grow, albeit at a slower rate than Asia's (+6% p.a. against +10% p.a.). demand and globalization. In scenario II, both the EU and U.S. will be negatively affected by the twofold impact of soft demand and globalization. The production value will be about halved. In contrast, the production value of the Asian fine chemical industry will more than double.

What are major market trends in terms of customer requirements?

Peter Pollak: In the medicine chests of the people living in emerging countries, more and more Western type pharmaceuticals will be stored. Worldwide, originator drugs will be substituted by generic versions. Therefore, custom manufacturing of pharmaceutical fine chemicals will lose ground against API-for-generics production.

On the M&A market, there have been two important developments since the beginning of the new millennium. In order to get a stronger grip on the Western markets, cash-rich Indian pharmaceutical and fine chemical companies entered into an acquisition spree of Western fine chemical/generics companies. Between 2004 and 2006 alone, more than 20 deals were completed. Like their European counterparts, which had a negative experience with their transatlantic expansions in the 1990s, not all Indian overseas acquisitions were a sweeping success.

More recently, financial investors have begun acquiring mainly European fine chemical companies. International Chemical Investor Group (ICIG) has been particularly active. Since inception in 2004, ICIG, dubbed one of the most prolific buyers of fine chemical assets in recent years has acquired 16 independent chemicals and pharmaceutical businesses with total sales of approximately €700 million. The figure does not include ICIG's most recent acquisition, namely Roche's (formerly Syntex's) large fine chemical plant in Boulder, Colo. ICIG's portfolio of pharma and fine chemical companies is managed as CordenPharma.

How can traditional fine chemical companies succeed in this challenging competitive environment?

Peter Pollak: Organic chemical synthesis is a mature science. It did not evolve much beyond the substitution of wood by stainless or glass-lined steel as construction material for chemical reactors, where chemical reactions developed during the golden years of the dyestuff industry are performed. Except a few niche technologies, the capability to operate a GMP multipurpose plant is hardly a differentiator any more - with one notable exception: biotechnology. Especially mammalian cell technology has a big future. It is required for producing the modern big molecule APIs, dominating for instance the market for oncology drugs.

However, entry barriers are high. Existing facilities cannot be used and demand for containment has reached a new dimension. On the other hand, both exclusive synthesis of biopharmaceutical APIs for the innovator companies and production of APIs for the fledgling generic versions of biopharmaceuticals, the biosimilars represent an attractive opportunity for entrepreneurial companies with a full war chest. In the more distant future, stem cell technology could become a major tool in medicine.

It allows substitution of damaged human cells with new, healthier versions that could eventually lead to cure for many chronic diseases, from macular degeneration to Alzheimer, diabetes, heart disease and spinal cord injury.

In terms of size, mid-sized, family owned companies have several advantages. They are not afflicted by the imperative to show better financial results from quarter to quarter - in a volatile market!

The CEO gets involved in projects, visits customers and takes binding decisions. As the size of a production campaign for any given fine chemical rarely exceeds a few ten tons, there also is no economy of size in manufacturing. Fine chemicals have to be produced in campaigns in multipurpose plants regardless the size of the company. In a business, where "low cost" is more important than "over-the-fence" supply, the Asian fine chemical companies have a big advantage.

What is the single most important success factor for a fine chemical company?

Peter Pollak: A track record of successfully completed new product projects with several Big Pharma companies.

Contact

PP Consulting

Wachtweg 3

4153 Reinach

Switzerland

+41 61 7138158

+41 61 7138159