Potential In Eastern Europe

The CEE and CIS Region Offers Benefits for API Manufacturing

-

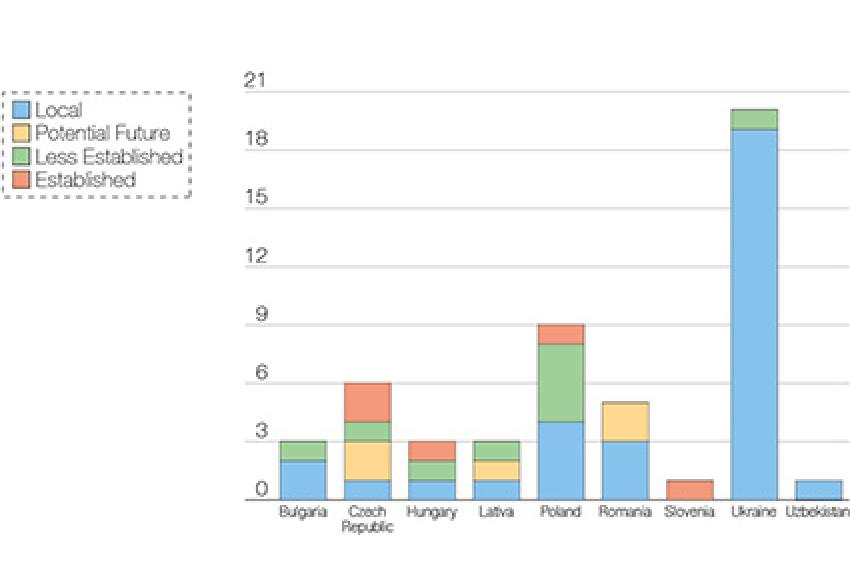

Figure 1: Number of API Manufacturers in CEE and CIS

Figure 1: Number of API Manufacturers in CEE and CIS -

Table 1: Recent Deals in CEE and CIS

Table 1: Recent Deals in CEE and CIS -

© Alex Yeung - Fotolia.com

© Alex Yeung - Fotolia.com -

Over the past five years, emerging markets have experienced some of the highest pharmaceutical market growth rates, a trend that is expected to continue. Central Eastern Europe (CEE) and the Commonwealth of Independent States (CIS) countries that, combined, make up Eastern Europe, offer a mix of developed as well as emerging opportunities for many companies looking to expand their global presence.

These countries also provide a cheaper alternative than their western EU counterparts for clinical trials and API manufacturing, while following a similarly defined regulatory pathway. Although the growth potential differs between regions like CEE and nations in the CIS, investment from outside the region is becoming more frequent, thereby allowing companies to gain access to new distribution channels and patient populations that favor branded generic medicines.

CEE versus CIS

Countries that make up the CEE are expected to have limited market growth in the coming years, but the highest rates will most likely come from Romania, which is expected to have a strong market with a compound annual growth rate (CAGR) of 6% in pharmaceutical sales growth. Hungary and Poland will have the lowest expected growth with a 2%-4% increase in pharmaceutical sales. Lastly, the Baltic States will be expected to round out the middle at an estimated increase of 4%-5% growth in pharmaceutical sales.

In terms of manufacturing, the region offers strong biopharmaceutical capabilities in biotech and vaccine production along with a talented pool of chemists due to its extensive history of research that stems from the Cold War. Among countries in the region, Poland and Hungary in particular are looking to expand upon key areas in genomic and preventative medicine and protein engineering by increasing the number of biotech cluster cooperatives, funding and links to academia.

The CIS nations, along with Ukraine, are expected to have the highest growth rates, with a CAGR in pharmaceutical sales at roughly 8%-9%, but the risk associated may prove to be a deterrent for parties interested in these countries. The Russian devaluation of the ruble and Ukraine's hryvnia could increase if ongoing tensions further escalate. It could also increase the cost of imports into these regions and further drive up prices, hindering foreign interest to set up local production.

Some of the most prominent and growing therapeutic areas in the region include oncology, diabetes, antibiotics, as well as the vitamins and minerals segment for many of the CIS countries. In contrast, the CEE will rely less on some of the consumer over-the-counter (OTC) areas but have some notable crossovers as interest in specialty drugs, oncology, diabetes, and asthma/chronic obstructive pulmonary disease medications will continue to increase.

While these countries may have fewer active pharmaceutical ingredient (API) manufacturers than India and China, they do have established companies like Zentiva, Polpharma, Gedeon Richter, Teva's Croatian arm Pliva, and Krka, among others, that are able to supply their markets and others with generics. According to Thomson Reuters Newport Premium, the Czech Republic and Poland have the highest number of companies within Eastern Europe with significant experience supplying API into regulated markets. Although Ukraine has a high number of total API manufacturers, many are designated as local companies supplying to their local and or other less-regulated markets, as seen in Figure 1.

Quality Of Medicines

Variations in how good manufacturing practices (GMP) are interpreted and implemented are important to note, as they may not be the same among this diverse set of nations. However, strong foundations like the Falsified Medicines Directive (FMD), and external organizations, like the Pharmaceutical Inspection Convention and Pharmaceutical Inspection Co-operation Scheme (PIC/S), will further promote quality API production and harmonization in many regions.

Many of the EU member states now require a written confirmation from the country of origin's authorized regulatory agency to ensure that API imports meet EU or equivalent GMP standards. Along with this, last year Poland signed a cooperation agreement to share GMP inspection outcomes with the FDA. Furthermore, the Czech Republic has seen an increase in local manufacturer inspections, which resulted in their State Institute of Drug Control suspending a marketing authorization after a non-compliance report was issued in April.

Recent legislative initiatives in Hungary have shown an increased focus on quality. Newly passed regulations allow unannounced inspections for monitoring the quality of medicines, as well as a new requirement for authorization holders to keep a minimum stock of certain medications deemed essential to mitigate shortages. In Kazakhstan, even, the State Program of Forced Industrial-Innovative Development is making the updates needed for facilities to adhere to EU GMP mandatory by the end of 2014. This may get postponed however, as Russia has had to extend its locally made API GMP deadline out until 2016.

Recent Investments and Their Implications

Investments into these regions usually take shape in the form of foreign multinationals partnering with local distributors or active ingredient manufacturers (Table 1). This is to manufacture the API, commercialize, or license products that are still patented in the US or the rest of Europe. This practice also takes advantage of the regional distribution channels that are already in place. Countries like Lithuania, Ukraine and Belarus provide gateways between Western Europe and Russia that are optimal for securing supply chains between the regions.

Lupin, Dr. Reddy's, Glenmark and Ranbaxy were some of the first Indian companies to pursue entry into the Ukraine and the CIS, and all hold strong positions in these regions. Other Indian companies looking to get more involved in these markets include Macleods and Cadila Pharmaceuticals. Having a local presence can be utilized to try to circumvent any protectionist measures, as well as make tech transfers and registration processes run more seamlessly. There is also considerable importance for Indian companies, including Cipla and Hetero, who have acquired or partnered with local distributors and chemical producers and have already funneled money into the region. For example, Cipla acquired Croatian-based Celeris d.o.o., while Hetero has a joint venture with Russian Makiz Pharma for the tech transfer and API production of its anti-retroviral product suite.

Using the skills of local talent at a cheaper cost than their Western counterparts, biopharma parks are getting attention in many of the CEE and CIS nations - including in Debrecen, Hungary, where Teva and Gedeon Richter have set up facilities. There is also an ongoing effort between Lithuania and India to develop a shared park in Lithuania's free economic zone at a plant that will be EU GMP-compliant. This can be done to encourage partnerships, licensing strategies, and shared resources needed to carry out R&D.

However, the potential interest in investing in these countries is juxtaposed by companies looking to also exit these markets. GSK announced it had a few curious buyers for its Romanian plant in Brasov, only to announce later that it would be closing the plant. The driving factors surrounding entry into the CEE and CIS markets are complex, and depending on future growth and generic penetration, the pursuit of these markets could sway in either direction, but the region does offer valuable benefits for API and generic medicine production.

Contact

Thomson Reuters

215 Commercial Str.

Portland, Maine 04101

+1 207 8719700

+1 207 8719800