Who’s Who in Fine Chemicals

An Analysis of the Industry’s Top 10 Players

-

Jan Ramakers, Jan Ramakers Fine Chemical Consulting Group

Jan Ramakers, Jan Ramakers Fine Chemical Consulting Group -

-

Looking back, moving forward - The fine chemical industry has gone through a few difficult periods in the last decennium. More recently, however, the market has improved quite a bit. In this article, we will have a look at the top 10 companies in the fine chemical market. In order to be able to put things in the right perspective it is interesting to look at the situation in the early 2000s first.

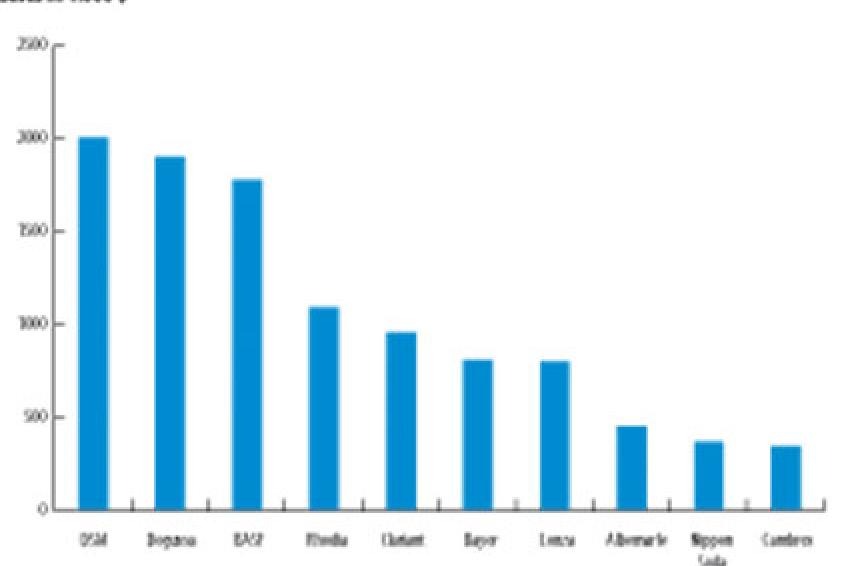

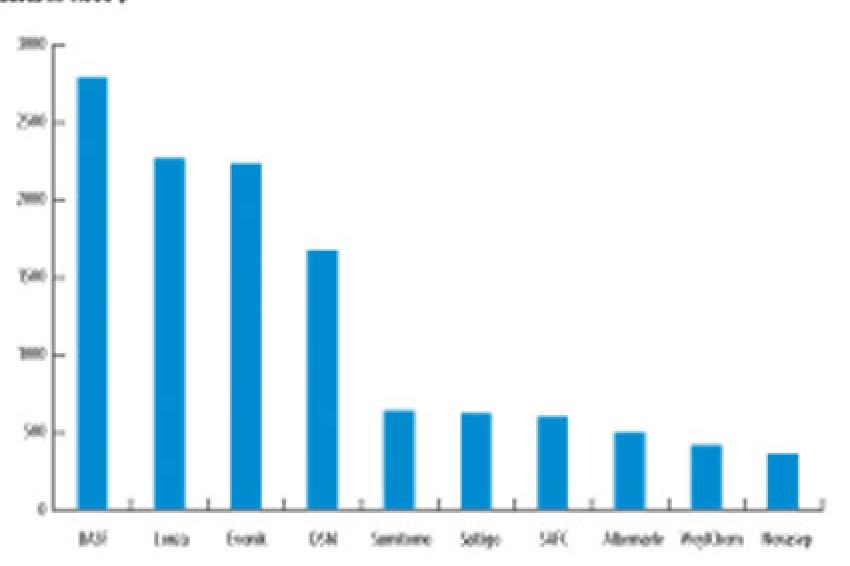

In 2001 (fig. 1) the three largest producers, DSM, Degussa, and BASF were very close to each other, each of them having fine chemical sales in the $1.8-2.0 billion range. Also in that year, the top five companies had a combined market share of 12.3%; the combined market share of the top 10 was 16.7%. Looking at the current situation (fig. 2) the first impression is that the industry has concentrated compared to eight years before.

However, closer look shows that this is not the case.

In 2009 the market share of the leading company was 3%, whereas in 2001 the market share of the leading company was 3.5%.

The top five had a combined market share of 10.4%, which is less than the 12.3% they had in 2001. Also, the combined market share of the top 10 in 2009 was 13.2%, down from 16.7% in 2001 and only slightly higher than the top five in 2001.

So the net result of all the buying and selling of businesses and companies since 2001 has not really increased the degree of concentration of the fine chemical industry. On the contrary, instead of being more concentrated, the fine chemical industry is more fragmented now than it was eight years ago. The increasing importance of fine chemical producers from India and China is thought to be one of the main factors behind this development.

A Closer Look at the Top 10

- BASF

As the leading fine chemical producer in 2009, Germany's BASF also happens to be the largest chemical company in the world with production sites in 41 countries. The product portfolio of the company ranges from chemicals, plastics, performance products, agricultural products and fine chemicals to crude oil and natural gas. The company's main site in Ludwigshafen is the world's largest integrated chemical complex. Over the last decade, BASF has invested significant amounts of money into the development of its Verbund strategy: optimal integration of processes and businesses. This has created a highly integrated company. - Lonza

The second largest company is Lonza. This company is quite different from BASF, not only in size but also because it has always viewed fine chemicals as its core business. At the end of 2006, the company divested its polymer intermediates business and since then almost all of its revenues have been generated from fine chemicals. In recent years, Lonza has invested heavily in strengthening its position in the biotechnology area.

Biotech manufacturing facilities were built and/or expanded at the Visp, Switzerland, and Slough, UK, sites in 2004 and 2005, followed by a large number of acquisitions and investments in the biotech area, including: UCB Bioproducts, Cambrex's Bioproducts and Biopharma segments; Genentech's mid-scale mammalian biopharmaceutical production plant in Spain; large-scale commercial mammalian cell culture manufacturing facilities in Singapore; a large scale production plant for antibody drug conjugates; and some others. With that, Lonza has positioned itself as a leading player in the biotech/biologicals area.

In 2008, it entered into a partnership with Novartis for the development and manufacture of its biological pipeline, and into a joint venture with Teva, one of the largest generics companies for the manufacture of biosimilars.

Currently, the company is streamlining its organization. The focus of its small molecule manufacture will be increasingly shifted to Asia. - Evonik

The next company on the list is Evonik. Evonik's fine chemicals business is part of its Chemicals Business Area, which formerly traded as Degussa. The company positions itself as a producer of specialty chemicals. Its fine chemical operation mainly revolves around the custom manufacturing business. The company divested its Seal Sands, UK, site in 2008 and it acquired Eli Lilly's Tippecanoe, U.S., API manufacturing facility - including a long term supply agreement - in 2009.

In April 2010, Evonik opened a new plant for the manufacture of APIs in Nanning in the Guangxi province of China. The plant has been set up in collaboration with an (unnamed) European pharmaceutical company for which Evonik will produce various APIs under a multi-year contract. - DSM

DSM, the leading fine chemical company in 2001, has streamlined its fine chemical portfolio over the past few years, which included some divestments and site closures in the pharma area in 2004-2006. One of the major reasons for this was the extremely competitive situation that developed in the market for semi-synthetic antibiotics, mainly from Asian producers, which had a heavy impact on DSM's business in that segment.

In 2007, the company decided to focus more on Life Sciences and Materials Sciences; it has since divested several of its commodity chemicals businesses and closed down or divested some smaller fine chemical manufacturing operations.

In May 2010, DSM Biologics signed preliminary agreements to enter a partnership with the Australian government to design, build and operate the first major Australia-based mammalian biopharmaceutical manufacturing facility, which will be located in Brisbane.

DSM ranked fourth in 2009. - Sumitomo Fine Chemicals

Sumitomo Fine Chemicals, the highest ranking Japanese company, merged with the fully owned Sumitomo subsidiary Sumika Fine Chemicals in 2003. After that no other major acquisitions were made. - Saltigo

The next one on the list is Saltigo, formerly the fine chemical business of Bayer. The business has certainly benefitted from its independence, as well as the subsequent realignments. Being independent from Bayer, one of the leading pharmaceutical companies as well as one of the leading agrochemical producers, made it easier for Saltigo to attract custom manufacturing business from the agrochemical and pharmaceutical industries.

In May 2010, Saltigo entered into a cooperation agreement with Syngenta, a leading agrochemical company. Syngenta is investing some €50 million in expanding several Saltigo facilities in Leverkusen to significantly enhance its capacity for manufacturing active agrochemical ingredients. Saltigo supplies the active ingredients and intermediates produced in those facilities exclusively to Syngenta. - SAFC

SAFC, the fine chemicals business of Sigma-Aldrich and the seventh largest producer of fine chemicals in 2009, has a clear focus on the pharmaceutical market. The company has shown a rapid growth to its current sales level over the past few years, largely as a result of a number of acquisitions. In 2004, it acquired Ultrafine (UK), a chemical contract services provider for drug development, and Tetrionics (U.S.), a specialized producer of high-potency pharmaceutical intermediates and APIs (HPAPIs). In 2005, it invested in the high potency plant, almost doubling its size.

In the same year it acquired JRH Biosciences (U.S.), a supplier of cell culture and sera products to the biopharmaceutical industry, and Proligo (U.S.), involved in nucleic acids and oligonucleotide synthesis. 2006 saw the acquisition of Iropharm (Ireland), involved in the manufacture of APIs, and Pharmorphix (UK), involved in research services for the pharma industry. In 2007, the company acquired Epichem (UK), involved in high-purity chemicals for the electronics industry. The Pharmorphix facility was expanded in 2007. Since then, the HPAPI capability was expanded a few times as well as the biologics capability of the company. - Albemarle

Albemarle showed good growth in the first few years after 2001, partly fuelled by acquisitions: Atofina's bromine fine chemicals business in 2003 and DSM Pharmaceutical Products' generic API business that was operated out of South Haven, U.S., in 2006. After that, growth stalled for a while but recently the fine chemicals business seems to be picking up the pace again. - WeylChem

WeylChem was formed in 2005, when International Chemical Investors Group of Germany acquired part of Rütgers. The deal included the pharma fine chemicals business of Mannheim-based Rütgers Organics and its U.S. affiliate, which specialised mainly in agrochemicals. Since its formation, the company has acquired a number of other businesses, including Albemarle's Thann, France, facility; the Cork, Ireland, and Landen, Belgium facilities of Cambrex; Clariant's custom manufacturing business; and and Miteni. - Groupe Novasep

Last but not least, the number 10 on the list is Groupe Novasep. The company is organized in two strategic business units: Novasep Process (focused on purification engineering) and Novasep Synthesis (focused on chemical and biochemical synthesis)

Novasep uses the combined strength of the business units to manufacture advanced intermediates and API's for custom manufacturing services to the pharma industry and other fine chemical industries. Séripharm, part of Novasep Synthesis, is involved in the manufacture of highly potent compounds. In 2009, the company acquired Henogen (Brussels, Belgium), a contract manufacturing organization offering bioprocess development and manufacturing services ranging from cell bank to supply of clinical products.

Pharma Significant for Fine Chemicals

The pharmaceutical industry has been the main market for fine chemicals for many years. As a matter of fact, the relative importance of pharma for fine chemicals is still increasing, and in 2009, pharma accounted for some 66% of the fine chemical market. Consequently, developments in the pharma market have a large impact on the status and developments of the fine chemical market.

In recent years the number of highly complex APIs with multiple chiral centres on the market has increased significantly. Typically, the manufacture of the vast majority of these products requires one or more biotechnological steps. Obviously, companies like Lonza and SAFC seem to be in a very good position to benefit from this development.

Another interesting development in the pharma market is the increasing importance of high potency APIs, and SAFC's acquisition and expansion of one of the leading HPAPI producers has put them in a good position to benefit from this development.

Most of the companies in the top 10 are fairly heavily involved in custom manufacturing. After a period of decline, the market for custom manufacturing has emerged from the doldrums and started to grow again.

Bright Future

The future of the market for fine chemicals looks brighter now than it has done for quite a few years. Custom manufacturing options are improving, as are opportunities in biotechnology and at the biotechnology/classic chemistry interface. At the same time the competitive intensity is likely to increase further, mainly from the increasing number of producers from China and India. To be successful in this market the ability to form manufacturing partnerships with clients, rather than being a supplier, will remain of vital importance.

Jan Ramakers Fine Chemical Consulting Group is focused on the analysis of the global markets for fine chemicals and the companies that participate in those markets. The company produces The Fine Chemical Benchmarking Service, and also undertakes tailor-made consultancy projects including market, product or industry analysis; company strategy analysis; and assistance in M&A /due diligence projects.