Global CMO Market

Emerging Locations and Competitor Analysis

-

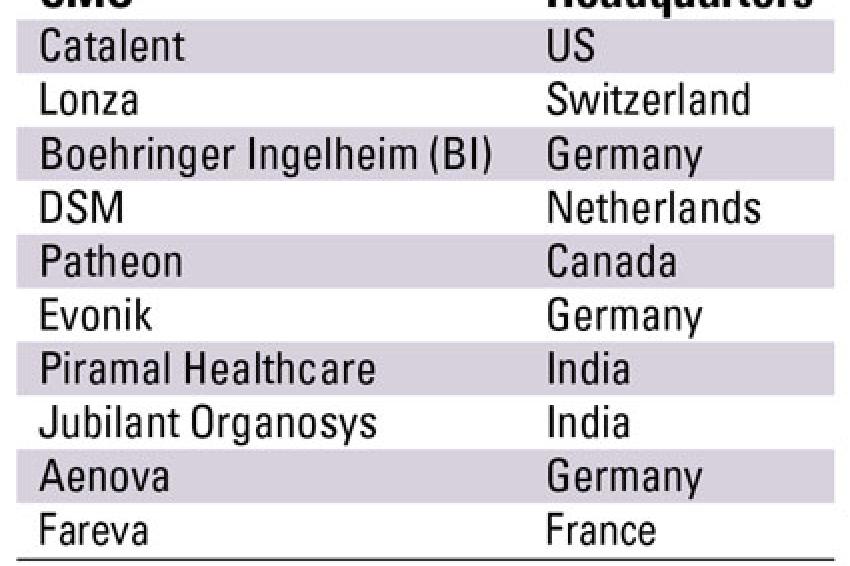

Fig. 1: Lists the world´s top ten CMOs

Fig. 1: Lists the world´s top ten CMOs

Over the years, pharmaceutical outsourcing has evolved from being a tactical activity to achieve a more strategic focus. Pharmaceutical companies are diligently evaluating their business models to create a mix of in-house and external outsourcing for long-term cost advantages and resource management.

In this context, emerging markets within Latin America, Eastern Europe and Asia look promising. The Asia-pacific region in particular, is fast emerging as the epicentre of pharmaceutical contract manufacturing activities with its inherent advantages. Locations such as India, China and Singapore are fast becoming the preferred locations for outsourcing manufacturing activities for a variety of reasons. Over the past few years large pharmaceutical companies have been involved in manufacturing downsizing either by shutting down redundant facilities in the U.S. and the EU, or shifting them to the Asia-pacific region. Subsequently, contract manufacturing organizations (CMOs) in these regions have successfully capitalised on this opportunity by leveraging their lower production, investment, labour costs and highly skilled manpower. This article aims to evaluate a few of the most attractive locations for CMO activities and demystify the reasons behind their position in the global pharmaceutical market.

India: Future Growth Subject to IPR Improvements

India's success in the drug manufacturing space is primarily attributed to its reverse engineering expertise. With several years of generics manufacturing experience behind it, India has gradually moved up the value chain by building its synthetic chemistry and custom production skills. The availability of trained manpower to meet this demand is also one of India's key advantages. It is estimated that the country has more than four times the drug manufacturing staff than the U.S. and more than twelve times that of the UK. Outside of the U.S., India has the largest number of FDA certified manufacturing units. India also leads the way in DMF filings in the U.S. market. Although the manufacturing of active pharmaceutical ingredients (APIs) and intermediates is India's biggest strength, the development of finished dosage forms is also emerging as a key growth area for the future. As a testimony to these skills, Indian CMOs such as Piramal Healthcare, Dishman Pharma, Divi's Laboratories, Jubilant Organosys, Shasun Chemicals and Biocon have partnered with big pharmaceutical players such as Astrazeneca, Eli Lilly, Glaxosmithkline, Merck and Pfizer, and are establishing themselves as a serious competition for Western CMOs.

One of the biggest reasons for an increased interest from Western players in the Indian market was the product patent act of 2005. However, the patent law has certain loopholes with regard to clinical trial data protection and overall patentability standards, which have cast doubt on the overall intellectual property (IP) climate. A case in point is the recent high-profile patent litigation ruled against Novartis. Surveys conducted by leading consultancies Ernst and Young in 2005, and Pricewaterhouse Coopers in 2007 revealed that over 60 % of multinationals in India mentioned insufficient IP protection as the biggest business risk. Certain Western companies outsource only the raw material and intermediate manufacturing to CMOs, while retaining the final critical stages in-house. Thus, although the overall perception about India as an outsourcing destination is highly positive, regulators will have to make efforts to enforce international IP laws to further increase investor confidence.

China: Preferred Destination for Bulk Drug Sourcing

Although China is not strong in the areas of finished dosage forms or high-end APIs, its biggest strengths lies in the cost-effective production of bulk drugs and API raw materials. China exports to markets such as the U.S., Japan, Germany, the Netherlands and even India. For instance it is the largest manufacturer and exporter of off-patent APIs such as beta lactame antibiotics. The Chinese pharmaceutical market is currently the eighth largest in the world and is expected to be the largest market by 2020, if current growth rates continue.

China continues to be an attractive destination for Western manufacturers for a variety of reasons. Firstly, its low-cost scientific talent, labour and raw materials enable it to produce drug substances at virtually 10 % of the cost in developed markets. Secondly, China has an excess manufacturing capacity which enables it to manufacture drug substances in huge volumes using economies of scale. One of the biggest drivers to outsourcing in China has been an increased interest in off-shoring of CMO activities. In 2006, Pfizer entered an alliance with Shanghai Pharmaceutical Group making it one of the first deals of its kind. Moreover, several other multinationals are also expected to follow suit in the coming years.

Despite its low-cost advantages, China does not have such an enviable track record with respect to quality and safety. The 2008 Baxter Heparin scandal which led to the death of several people, dented China's reputation as an emerging outsourcing destination and highlighted the safety risk. Yet another risk in outsourcing to China is IP protection. While China does have patent laws in place, Western manufacturers have to realise that a clear understanding of the legal system is absolutely essential for the enforcement of these laws. Finally, several Chinese CMOs largely follow the national good manufacturing practice (GMP) guidelines which are below the normally accepted cGMP or EU GMP standards, increasing the regulatory risk. However, China has been increasingly working towards improving the regulatory environment by focusing on aspects such as reducing the overall drug approval time, and procurement of State Food and Drug Authority (SFDA) certification.

CMO Competitor Analysis

The pharmaceutical contract manufacturing industry is highly fragmented with the top ten CMOs occupying less than 30 % of the overall market share. Out of these, the top three players - Catalent, Lonza and Boehringer Ingelheim - generated contract manufacturing revenues in excess of $1 billion over a three year period whereas the rest were in the sub $1 billion range.

Catalent, the largest CMO, offers a diverse range of services such as oral and sterile dose manufacturing and even packaging. With almost all the leading pharmaceutical and biotechnology companies as its clientele, Catalent's biggest strength is its diversity of offerings. However, the CMO depends heavily on the U.S. market for its revenues and the current economic climate might affect its future performance. Lonza, the second largest CMO is the preferred service provider for biopharmaceutical manufacturing. Its strategy of increasingly focusing on capacity expansion particularly in emerging markets such as China and the Czech Republic is expected to help it retain its position as a leading CMO. Boehringer, another leading biopharmaceutical CMO, experienced a slump in both its revenues from pharma chemicals as well as biopharmaceuticals.

Historically, the CMO industry has been dominated by European and North American players. However, over the past few years Indian CMOs such as Piramal Healthcare and Jubilant Organosys have emerged as serious competition to leading CMO players. Over the past three years, Piramal Health recorded phenomenal growth, particularly in its APIs and formulations segment. It has also made forays into the injectables market through its 2008 acquisition of Healthline. With their strong API and generics background, Indian companies are expected to further strengthen their position in the global CMO market.

Conclusion

As their regulatory and IP climate improves, emerging markets such as India and China are expected to become increasingly favourable destinations for outsourcing and offshoring. Moreover, CMOs from emerging markets are likely to further challenge their larger Western counterparts. Despite the challenges, Western CMOs have an opportunity to leverage the vast resources and superior cost-advantages that emerging markets offer to give themselves a strong competitive advantage.

Frost & Sullivan's, Growth Partnership Service provides the CEOs and their teams with disciplined research and best practice models to drive the generation, evaluation, and implementation of powerful growth strategies. To join our Growth Partnership, please visit http://www.frost.com.

Contact

Frost & Sullivan

Clemensstr. 9

60487 Frankfurt

Germany

+49 69 7703343

+49 69 234566