Agrochemical’s Role in Creating World Peace

Industry Must Deliver Safe Innovative Products

-

© James Thew - Fotolia.com

© James Thew - Fotolia.com -

Dr. Nigel Uttley, Enigma Marketing Research

Dr. Nigel Uttley, Enigma Marketing Research -

Fig. 1: Relationship between rising population and available arable land

Fig. 1: Relationship between rising population and available arable land -

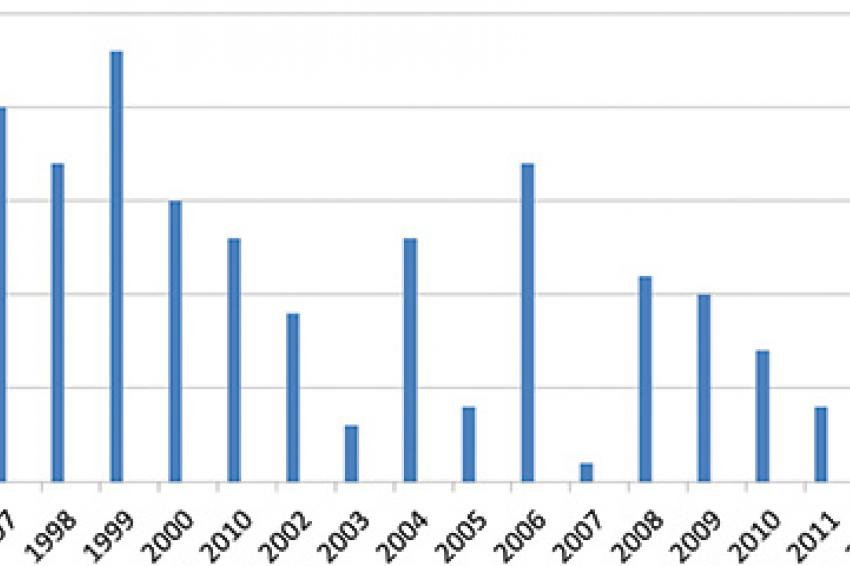

Fig. 2: Rate of new active ingredients reaching the market.

Fig. 2: Rate of new active ingredients reaching the market. -

Fig. 3: Sales of the crop protection market by sector based on IPR.

Fig. 3: Sales of the crop protection market by sector based on IPR. -

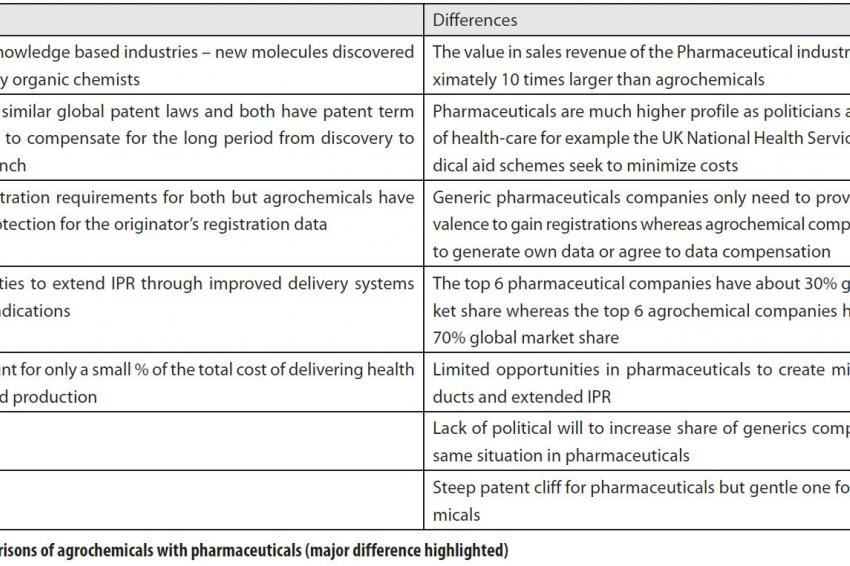

Fig. 4: Comparisons of agrochemicals with pharmaceuticals (major difference highlighted)

Fig. 4: Comparisons of agrochemicals with pharmaceuticals (major difference highlighted)

Finding The Balance - The global food supply and global peace are interlinked. Agrochemicals play only a small part in the cost of food production and other factors such as food wastage, other inputs such as fertilizers and machinery and delivery infrastructure are all contributors. Nevertheless, agrochemicals have over the last 60 years made significant contributions to improving yields.

Dr. Nigel Uttley of Enigma Marketing Research analyzes the balance between innovator and generic companies and looks at how the regulatory system can be used to encourage generics rather than a deterrent as exists at present.

Since 2007 the global crop protection market (excluding GM seed, conventional seed or non-crop market sectors) has grown from $33 billion to $47 billion in 2012, an average rate increase of 7% per year. Future growth predictions will depend on issues such as: population growth and the resulting decrease in available land for agriculture (fig. 1); increasing sophistication of eating habits - a meat based diet requires greater use of pesticides than a vegetarian diet; consumption of major commodities is rising faster than population growth; and rising crop prices.

There will inevitably be a greater use of agrochemicals and the need to deliver safe innovative products, increase yields and to counter resistance problems in a cost effective way will be just as, if not more, important than ever. There needs to be a balance between the innovator companies reaping the rewards of providing such new products and a healthy generic sector which contributes to driving the cost of pesticides down.

Intellectual Property Rights (IPR)

The basic goal of the innovator companies over the last 60 years has been to introduce more effective active ingredients to replace older products especially as patent protection expires and thus maintain market share. Over the last 10-15 years, there has been a decline in the rate of new active ingredients and new chemical classes reaching the market (fig. 2), however, this does not mean that there is a decline in innovation; in fact, there has been a substantial increase in the introduction of new products primarily achieved by: mixtures of two or more active ingredients; improvements in delivery systems; and new improved formulation additives.

Such innovations can also result in products with IPR beyond that of the basic active ingredient and hence extend market exclusivity. The pharmaceutical industry has limited opportunity to develop mixture products although changes to formulation can lead to significant IPR opportunities and delay the patent cliff.

Based on IPR of the active ingredient the market is split into three product types (fig. 3).

- A patented product, where the active ingredient(s) is protected by a granted patent

- A proprietary off-patent product

- A generic product, where there is true competition in the market place and generic companies have registered products based on their own data and are not beholden to the main or original data holder

The proprietary off-patent products category arises when the active ingredient is off-patent but the final formulated product has some proprietary technology such as a new delivery system; is linked to GMO crops; is a mixture product which may contain a patented active ingredient or which can be patented; or has data protection issues that will restrict generic manufacturers entering the market.

The proprietary off-patent sector is the largest, and it is this sector which is the real battle ground between the innovator companies and generic manufacturer - a battle which the innovator companies are winning by introducing many mixture products, this segments the market and reduces the available market for generics to target. About 60-70% of the market is controlled by the top six companies, yet only about 20% of all active ingredients have patent protection.

In the generic sector, there is a small number of large companies with sales in excess of $500 million and sales in all the major global markets. When it comes to new products, these generic companies can also be innovative through the development of new formulations and mixtures. There are many hundreds of small generic manufacturing companies (mainly in India and China) with sales of less than $50 million per year. Many of the small companies have relied on the local market to provide the majority of sales and have sought export markets where registrations are relatively quickly obtained and inexpensive.

However, as registration requirements in all countries become harder and more expensive, it will be necessary for serious, long-term generic players to enter the large well-protected markets of Europe and the U.S. in order to spread the cost of registrations over as many markets as possible.

In order for these companies to grow and take advantage of the increasing market share taken by off-patent products, it is necessary to invest larger sums of money in product registrations and/or find partners with which to share the costs. To date, only a relatively small percentage of Indian and Chinese companies have managed to develop European and/or U.S. registrations.

The introduction of new active ingredients has declined from 20 per year to 5-7 per year; however, if we look at the 196 agrochemical patent applications filed in 2012 in the EU and U.S., 85% of filings were from the major innovator companies: Syngenta: 59; Bayer CropScience: 52; BASF: 29; Dow AgroScience: 15; DuPont: 11. The majority of these patents are not for new active ingredients per se but are mainly for mixture products.

In addition to the technical benefits of mixture products, commercial benefits also result. For example, mixtures segment the market creating a greater number of branded products, thus making it harder for generics to take market share. The use of patent-protected active ingredients restricts market entry by generics - if one of the mixture's active ingredients is patent protected, generic companies will not have access to this active ingredient, and therefore cannot enter this segment of the market until all intellectual property rights have lapsed. Also, many mixture products have received patent protection in their own right.

As a pharmaceutical loses patent protection and generics enter the market, prices will fall rapidly, which can seriously affect the share price. However, for agrochemicals, the ability to create new mixture products and/or new formulations means that the patent cliff isn't as steep and significantly delayed in many cases.

Registration Of Agrochemicals

The registration of agrochemicals is mandatory prior to sales; different countries/regions have different systems and some are stricter than others. All systems are becoming more regulated to ensure food quality is high and agrochemicals are delivered safely to the crop. In the pharmaceutical industry (fig. 4),

a generic company only needs to prove bioequivalence of its product with that of the innovator's product and can then cite the innovator's registration data file to gain registrations. Thus, the cost of market entry is significantly reduced and results in an erosion of prices. In the U.S., the first generic to market is further rewarded by a six-month period of exclusivity prior to market entry of other generics. Encouraging the generic pharmaceutical sector is a result of lobbying by large private and public health-care providers.

In agrochemicals, no such lobbying or political initiatives exist, and generic companies have to generate their own registration data or agree to data compensation with the data holder. This puts the generic agrochemical company at a massive disadvantage compared to its pharmaceutical counterpart, as the ratio of cost to market entry compared to potential market gain is considerably higher for generic agrochemical companies.

If it is recognized that global food security is a key element for global peace, then this is the one key area where politicians can contribute to driving down agrochemical input costs by making access to registrations cheaper for generic companies. Global harmonization of registration systems will also help drive down the cost for all companies.

Global food security is a key element for global peace and the growing population; increased sophistication of eating habits will put severe pressure on food supplies and will fuel demand for larger volumes of agrochemicals resulting in increased sales. The agrochemical industry will continue to play a key role to increase yields and if this is to be at affordable prices then the generic sector needs to be encouraged by making market entry easier.

Contact

Enigma Marketing Research

2 Woodlands Drive

Goostrey,Chesh. CW4 8JH Westfield House

United Kingdom

+44 1477 544056