Boston Consulting Group On Global Megatrends

Differentiating Success Factor or Just a Hollow Phrase?

-

The word “megatrend” is a beloved buzzword — but what implications will these trends have on the chemical industry? ((C) Goenz/Pixelio.de)

The word “megatrend” is a beloved buzzword — but what implications will these trends have on the chemical industry? ((C) Goenz/Pixelio.de) -

Udo Jung, Senior Partner, Global Leader Chemicals Sector, The Boston Consulting Group

Udo Jung, Senior Partner, Global Leader Chemicals Sector, The Boston Consulting Group -

Figure 1

Figure 1 -

Figure 2

Figure 2 -

Figure 3

Figure 3 -

Figure 4

Figure 4

Just A Word? - The word "megatrend" is a beloved buzzword - but what implications will these trends have on the chemical industry? The Boston Consulting Group's Udo Jung examines value creation in the industry and offers this warning: "Chemicals companies will not differentiate themselves with colorful pictures in their annual reports and glowing accounts of megatrends' assumed automatic benefits for their businesses."

The term "megatrends" refers to fundamental changes with concrete and lasting impact, both on the lives of individuals and on the macro-economic development of entire nations and regions. The list of megatrends is long. Typically, the following are in the foreground:

- Demography and strongly divergent population development in different regions of the world

- The wide divergence in anticipated growth rates among individual regions among the regions of the world, which we describe as a "global two-speed-economy."

- Resource constraints (of energy sources, water, agricultural land, and food), with the resulting necessity of considerably more efficient use of resources

- Continuously increasing mobility combined with simultaneously drastically lower costs of information processing, transmission and documentation

- After the end of the Cold War era, the transition to a multipolar world, including intensified regional conflict and terrorist activities and consequently higher security needs.

The list goes on and could be further elaborated with details. Megatrends will have a serious impact on the world economy and on all sectors of industry, including, of course, the global chemicals industry. Individual megatrends can be translated very concretely into demand for chemicals products or for end products that require specific chemical primary products. For instance, the megatrend resource efficiency leads to concrete demand for chemicals products: e.g. use of weight-reducing high-performance materials (plastics, composites, etc.) in automobile manufacturing, with the goal of reducing fuel consumption (fig. 1).

Therefore, it comes as no surprise that nearly all chemicals companies are emphasizing the connection between global megatrends and their own growth opportunities: Megatrends as drivers of growth. But the relevant terms and catchwords often seem generic and interchangeable. Why a particular company should profit more from a specific megatrend - as relative to its competitors - often remains unexplained, and it is almost never stated which strategies are relevant to make the most of megatrends for a certain company.

Long-Term Value Creation by Global Chemicals Companies

Which chemical companies, in which regions and segments, have really created value in the past five, 10, or 20 years? What do chemicals companies with long-term successful track records have in common? Do megatrends play a role here? Every year, The Boston Consulting Group analyzes value creation by publicly listed companies on a global basis using total shareholder return (TSR, or the annual change in the price of a share including dividends).

For companies in the high-investment chemicals industry, multi-year comparisons are particularly revealing: Per year, by what percent did the TSR of a company change on average over the last five, 10, or 20 years (fig. 2)?

BASF, for instance, improved its TSR by an average of 17% per year over the last 20 years and is thus among the top quartile of the 83 chemicals companies that have been listed for the last 20 years. Over the last five years, BASF raised its TSR by 17.9% per year on average, putting it in the second quartile of the 131 analyzed companies that have been listed for at least 5 years.

A Look At The Facts

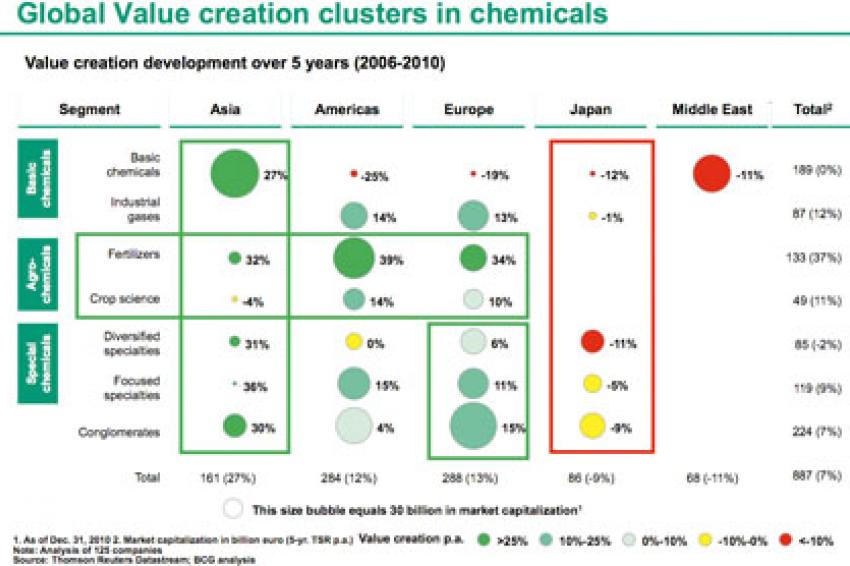

Can any patterns be discerned in long-term value creation by chemicals companies? Figures three and four show the first results of our analysis.

Figure 3 shows average annual value creation for 125 chemicals companies over the last five years, both by region and by the segment of the chemicals industry. The figure also shows the range of annual value creation within the categories.

In many segments, the range is wide: Value creation is determined by specific portfolio momentum, business model and the quality of the company's management. But its regional and segment-specific positioning are also relevant.

In figure 3, regions and segments are displayed by decreasing annual value creation. The first patterns become visible: Asian chemicals companies (except in Japan) achieved higher value creation on average than their American or European counterparts. As far as segments are concerned, the value creation "hit list" is led by fertilizers, basic chemicals (other than in Japan), industrial gases, and agrochemicals.

(Exactly the same four segments are on top in 10-year value creation as in five-year value creation!) Additional insights are derived when the regional and segment views are combined.

Global Megatrends and Ranking of Value-Creation Clusters

Figure 4 shows that there is a connection between major - and already long present - global megatrends and the ranking of value creation clusters.

- In terms of yearly average, Asian chemicals companies (with the exception of Japan) created more value by far than chemicals companies in other regions. Here, we can see that demand for chemicals in many Asian countries has benefited especially basic chemicals and numerous polymer applications (polyolefins, rubber, and high-volume engineering plastic).

Drivers of this growth in basic chemicals are the massive growth of processing industries in Asia; emerging countries' significant investments in the improvement of infrastructure; and the fact that especially in countries such as China and India, but also in the densely populated countries of Southeast Asia, the rise in disposable per-capita income has enabled and will continue to enable millions of people to become active consumers for the first time ever. - The value creation clusters fertilizer and agrochemicals have links with the megatrends demographics (with the resulting strong increase in demand for, e.g., meat and processed foods) and resource shortages - in this case, arable land.

- The negative value creation of basic chemicals companies in the Middle East is, first of all, not particularly significant, due to the low number of companies (three). But it is also an indication that major investments in future business (including acquisitions, but especially new production capacities) in the service of long-term strategies - derived to some extent on the development goals of the respective economies - have not yet become profitable.

- Typical for the European chemicals industry are special chemicals companies and companies with broad business portfolios. Value creation in these clusters is at least as good - and often better - than in other regions. Is this surprising? Will it last? We are not surprised, and we believe that European chemical companies will continue to represent a central and value-creating cluster among their peers worldwide: They are currently in the process of positioning themselves globally and often have an edge over American and especially Japanese chemical companies.

But there is another relevant factor that we feel is extremely important: Our analyses showed that European chemicals companies have "learned" to create value in very different and differentiating chemicals segments. This ability to manage various business models under one roof is one of European (and leading American) chemicals companies' strengths. Businesses that have a "complexity requirement" achieve customer retention and provide a basis for innovation. Non complex management of complex businesses- this is the key.

Megatrends and Value Creation in the Next Decade

What hypotheses can be derived for the future from our considerations so far? What should individual chemicals companies do to get the most benefit and value out of the described megatrends? Some of these megatrends, or their effects, will gain dramatically in importance. One example: By 2030, about 85% of the total increase in consumption spending in Germany will come from people over 55!

What demand for chemicals products will result from this? Over two thirds of the global growth of the chemicals industry through 2020 will take place in Asia. Efficient use of resources and the attendant requirements-including the relevant regulatory requirements and costly sanctions for inefficiency-will gain hugely in importance.

Chemicals companies will not differentiate themselves with colorful pictures in their annual reports and glowing accounts of megatrends' assumed automatic benefits for their businesses.

Chemicals companies will differentiate themselves with the concrete measures they take and which structural changes they realize to achieve real and lasting advantages from megatrends. In 2020, almost 50% of the global demand for chemicals will come from Asia. The center of gravity for growth and demand will shift. European chemicals companies are in the process of establishing production sites "in Asia, for Asia." Is this enough? Research and product development also often belong in Asia, for Asia.

Companies have to do even more: Their own centers of gravity have to be more closely aligned with global chemicals markets and market growth. This applies not only to sales markets and production networks, but also to global chemicals companies' decision-making centers and processes (are they close enough to the market?

Are the people making the decisions familiar with the respective growth markets' cultures, attitudes, and languages? Is the available market knowledge on a par with the importance of the respective market? Often, mature but stagnating markets are subjected to "micromarketing," while highly diverse market segments in China and India are all thrown into the same pot).

And there's another megatrend that applies here: Fast-growing companies in emerging markets (an obsolete term, since these markets have long since emerged; it's more applicable to say "rapidly developing economies" or RDEs) are driving their own globalization from Asia - with a level of ambition, energy, and long-term outlook that American and European incumbents often tend to gravely underestimate.

Contact

The Boston Consulting Group

An der Welle 3

60322 Frankfurt am Main

Germany

+49 69 915020

+49 69 5964793