Change In China

Transformation of the Chinese Economy and Consequences for the Chemical Industry

-

China will undergo a quantitative and qualitative transformation in the next 10 to 20 years, which will affect the general chemical industry in China. © takau99 - Fotolia.com

China will undergo a quantitative and qualitative transformation in the next 10 to 20 years, which will affect the general chemical industry in China. © takau99 - Fotolia.com -

Dr. Kai Pflug, CEO, Management Consulting

Dr. Kai Pflug, CEO, Management Consulting -

Fig. 1:

Fig. 1: -

Fig. 2:

Fig. 2: -

Fig. 3:

Fig. 3:

Predicting Threats And Opportunities - The transformation of the Chinese economy is a major topic in the media, covered by publications as diverse as The Wall Street Journal, Al-Jazeera and the Xinhua News Agency. It is also a focus of high-level Chinese politicians such as Wen Jiabao and his successor as prime minister, Li Keqiang.

China will undergo a quantitative and qualitative transformation in the next 10 to 20 years, which will affect the general chemical industry in China. The economic transformation will have different consequences for specific segments of the chemical industry.

Analysis of this may provide industry participants with insight regarding the relative attractiveness of different chemical products and segments, and thus may be useful for strategic and investment decisions.

Quantitative Transformation of the Chinese Economy

Clearly there is a shift away from the high annual growth rates of gross domestic product in the recent past. While annual growth was between 9% and 12% from 2004 to 2011, growth in 2012 slowed to 7.8%, and the official growth target for 2013 is 7.5%. For the next decade or so, an annual growth of between 5% and 7% seems a much more realistic assumption than a continuation of the earlier growth. This in itself is not a reason to worry but rather a common global phenomenon: Economic growth slows down once a certain economic level has been achieved as the most promising improvements in production and other economic activities have already been implemented.

... And Effect on Chemical Industry

By now, the chemical industry as a whole is maturing. As a consequence, the difference between GDP growth and the higher growth of the chemical industry (approximately a difference of 4% in the past few years) is likely to shrink to possibly 2%. Combined with the reduced GDP growth, this will result in a chemical industry growth of about 7% to 9% for the years until 2020. This is still respectable growth, but obviously a lot lower than in the recent past.

Qualitative Transformation of the Chinese Economy

The lower growth rate of the Chinese economy is widely regarded not only to be a threat but also an opportunity to increase the quality of growth.

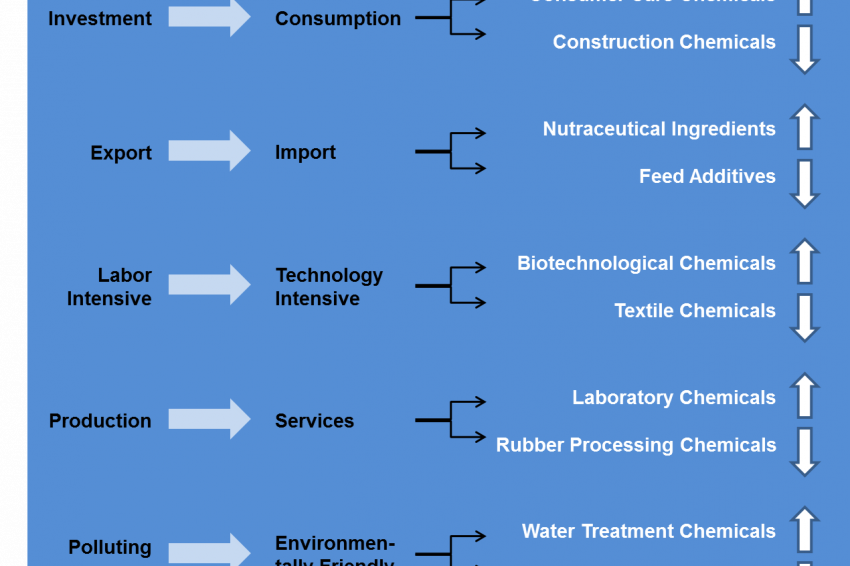

Five main areas can be identified in which a qualitative transformation of the Chinese economy is both a target of the government and to be expected:

- From investment to consumption: While the Chinese economy has long been driven primarily by fixed investment, private consumption will now grow in importance. As the disposable income of the Chinese rises, they will be able to spend more. Recent government initiatives in this area include boosts in the minimum wage and support for the expansion of consumer credit. Further potential lies in strengthening the Chinese pension and health-care system, encouraging the Chinese population to spend money rather than to save it for the future. Correspondingly, those industries that primarily serve investment purposes (e.g., producers of construction machinery) will experience slowdowns.

- From export focus to increased imports: Along with investment, exports were the other main driver of the Chinese economy in the past. However, as export markets in Europe, the U.S. and Japan have slowed down while the Chinese economy is still expanding, imports will likely increase at a faster pace than exports.

- From labor-intensive to technology-intensive production: China is now a middle-income country and no longer has the advantage of cheap labor. This trend will continue as the number of workers in China's workforce will start to decline in the next few years, putting additional pressure on employers to lift wages. In fact, some industries with a focus on low salaries, such as textiles, are already moving away from China. At the same time, Chinese policymakers state their intention toward a more innovation-driven economy. In 2013, China will spend an estimated 2% of GDP in research and development, a level achieved only by the most R&D-intensive countries in the world.

- From production to services: Currently, the service sector accounts for only about 45% of Chinese GDP compared with 80% in the U.S., indicating a great improvement potential. Rising consumer spending is likely to benefit services such as software, entertainment and tourism more than the production of physical goods.

- From polluting to more environmentally friendly processes: Rising incomes make the Chinese population less tolerant of environmental pollution and more willing to accept a somewhat slower growth if the quality of growth is higher. The 12th Five-Year Plan strongly supports the idea of sustainability, and individual provinces such as the Guangdong government have already enacted fairly ambitious targets for reducing energy consumption and carbon dioxide emission per unit of GDP. There, the government has stated its willingness to slow the growth of industries with high energy consumption in order to reduce the release of pollutants.

... And Effect on Chemical Industry

These five transformations do not affect all chemical segments in the same way. Before carrying out a more detailed segment analysis, there are some general observations on this.

The shift from investment to consumption will benefit those chemical segments supplying mainly consumer products, for example consumer care chemicals. In contrast, chemical segments such as construction chemicals - which naturally depend on investment in infrastructure and buildings - may suffer.

Reduced exports are likely to negatively affect segments with export-oriented end customers such as textile chemicals, textile dyes and leather chemicals. On the other hand, chemical multinational companies with a strong China presence may benefit by increasing their imports of high-end specialty chemicals and materials.

The transformation toward technology and innovation is already quite visible in the many R&D centers that have been established particularly in the Shanghai area in the past 10 years. It is likely to continue, with smaller and second-tier foreign companies as well as bigger domestic companies also increasing their R&D work in China.

The shift from production of physical products to services is one that will have a marginally negative effect on most chemical segments, as the chemical industry by definition focuses on physical products.

Finally, growing awareness of environmental issues will benefit a few chemical segments such as water treatment chemicals while at the same time negatively affecting others (such as leather chemicals, pigments and dyes), similarly to the segment shift experienced in Europe and the U.S. a few decades ago.

Effect on Key Chemical Segments

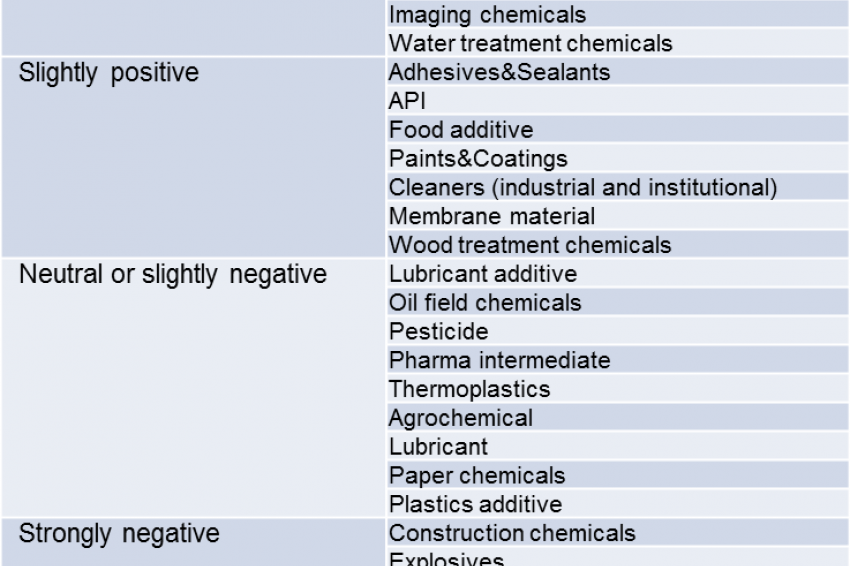

For this categorization, each segment was examined for each of the five transformation factors. For each segment/factor combination, the effect was either judged to be positive (i.e., the transformation factor will favor the growth of the chemical segment), neutral (the transformation factor will not have a major influence on the growth of the chemical segment) or negative (the transformation factor will negatively affect the growth of the segment). All evaluations were then weighted and aggregated, resulting in four groups of chemical segments:

- Some chemical segments experience strong additional growth as a result of the transformation of the Chinese economy.

- Some chemical segments experience minor additional growth.

- Some chemical segments experience a minor reduction of growth.

- Some chemical segments experience a major reduction of growth.

In summary, the transformation of the Chinese economy will have a substantial effect on the chemical industry. However, the effect depends much more on the specific chemical segment than on the general properties of the chemical industry.

Contact

Managm. Consult. Chemicals

RM1302, 13/F CRE Bldg.

Wanchai, Hong Kong

China

+86 1368 1873992