The Expanding Role of Contract Manufacturing

In the shifting pharmaceutical landscape, contract manufacturing organizations (CMOs) and big pharma could see significant benefits. The findings of a new A.T. Kearney study can help pharma companies unlock value beyond lowering costs and enable CMOs to become competitive international players, far beyond their role as an extended workbench.

Three trends are shaping the CMO industry:

- Demand for CMOs in regard to service offerings and technological requirements is growing. Historically, pharma companies turned to outsourcing for chemical active pharmaceutical ingredients (APIs) and simple finished dosage forms (FDFs), primarily in generics and consumer health. Now, they are outsourcing high-potency APIs, bio-APIs, biopharmaceuticals, advanced bulk, and new molecular entities (source: PharmSource).

- CMOs are evolving from service providers to strategic partners. CMOs now cover the entire value chain of pharma production, including specialized services such as R&D. New agreements and stronger partnerships are emerging, with CMOs buying manufacturing sites or taking on construction projects to support manufacturing requests.

- M&A activity in the fragmented CMO landscape is spiking. This is leading to plans for geographic expansions and upgrading of technological capabilities.

Market, Technology, and Geographic Overview

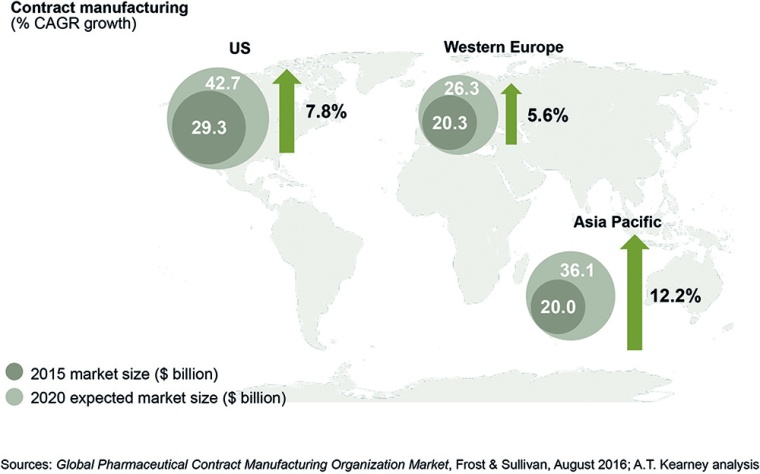

The global CMO market had $72.7 million in revenue in 2015. By 2020, it could surpass $108 million. The US is the largest market, but Asia Pacific is expected to see double-digit growth, and Europe will remain a CMO hub.

The market is divided into three segments: APIs, intermediates (bulk), and FDFs, which include solids, semi-solids, liquids, and injectable doses. The largest segment is API and intermediate CMOs, with around 80% of the market and predicted growth of 8% until 2020. 95% of revenue is generated by CMOs that focus on chemical APIs. However, by 2020, CMOs focusing on biotech APIs will increase their revenue share to 9.5%, and generic APIs will make up 65% of the market (source: Frost & Sullivan). FDFs are predicted to grow at 9% until 2020, mainly due to the need for oncology and immunology products.

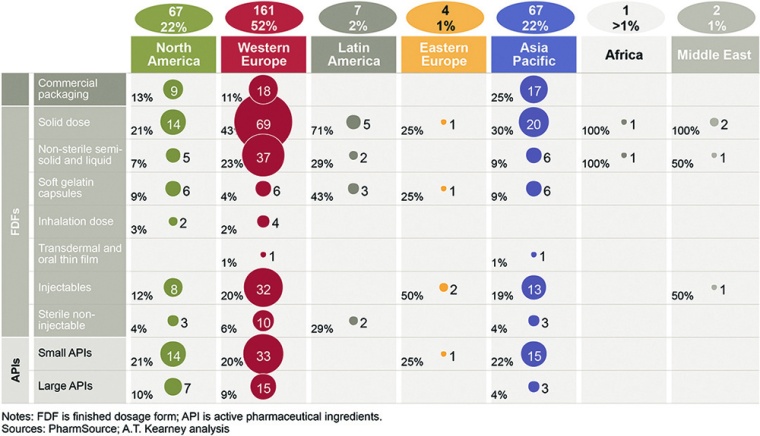

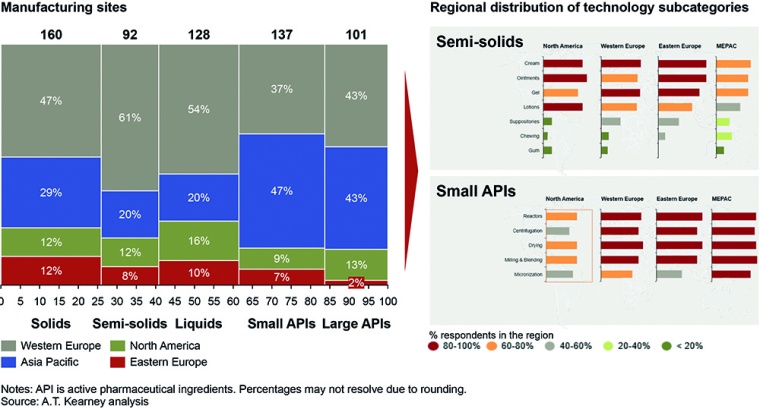

More than half of the top 30 CMO manufacturing sites are in Western Europe, and 22% are in North America and Asia Pacific (fig. 1). Europe is a hub for well-developed FDFs, including solids, non-sterile semi-solids, and liquids as well as injectable and non-injectable sterile products. Europe also leads in small and large API manufacturing, but in emerging markets, these players have marginal production capacities for APIs.

Our study of more than 300 CMOs sheds light on the technology distribution across regions, supporting the theory of Europe as a global hub and confirming Asia Pacific’s growing capabilities. Trends indicate outsourcing will occur for high-potency APIs, bio-APIs, biopharmaceuticals, and advanced bulk as well as new molecular entities. In particular, Europe and the US could benefit, thanks to advanced equipment, labor, and technologies. This will most likely balance out any short-term revenue losses from manufacturing low-cost off-patent molecules and low-end intermediates or solid-dose manufacturing in Asia Pacific. However, as Asian companies upgrade their facilities and focus on quality, manufacturing speed, equipment use, and product yield, the region will become more attractive.

The CMO Landscape

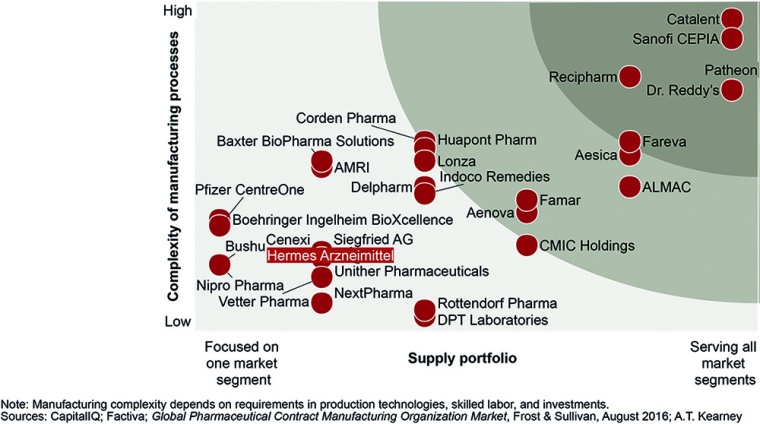

The landscape is highly fragmented, with more than 400 companies holding less than 2% of the market and as much as 49% of revenue coming from the top 10 CMOs (source: Frost & Sullivan). Suppliers differ in the variety and complexity of services they provide and the regions they supply.

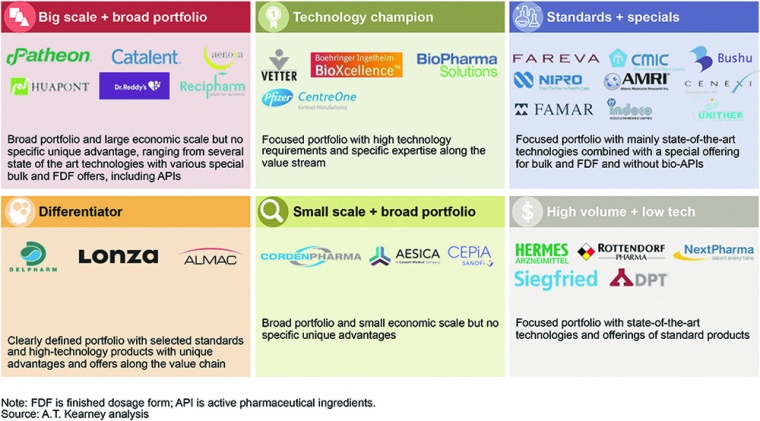

Our research reveals six categories of CMOs, based on the following criteria (fig. 2):

- Portfolio broadness. The number of types of API, bulk, and FDF capabilities. (Note: A supplier that covers more than three of five categories—solids, semi-solids and liquids, injectables, small APIs, and large APIs—is considered to have a broad portfolio.)

- Technological fitness. The high-tech technologies the CMO offers: large-molecule APIs, special products, or sterile products (bulk and FDF)

- Economic scale. Company revenue (US dollars) and revenue growth (CAGR)

- Ownership. Private-equity owned, publicly traded, or family owned

Because suppliers in the same category have similar predispositions, CMOs can use our categorization to inform decisions about factors such as M&A, partnerships, and technology while pharma players can use it to find a CMO that fits their needs.

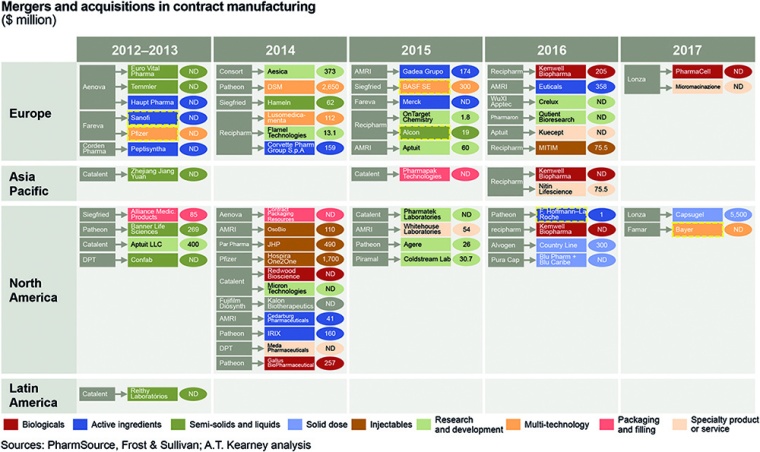

M&A Activity

The top CMOs have been on an M&A splurge, with 2016 and 2017 seeing massive deals. Most acquisitions by big CMOs between 2012 and 2017 were in Europe, followed by North America. Despite Asia Pacific growth predictions, most CMOs have not targeted Asia or India. However, there have been acquisitions of Indian (Piramal) and Chinese (WuXi AppTec) players in Europe and joint ventures in the US, including Bioepis’ partnerships with Samsung and Biogen. Most of these acquisitions aim to add either value to the portfolio or services across the value chain.

In addition, 2015 and 2016 saw acquisitions in contract research and contract development and manufacturing organizations, underscoring the fact that players are aiming to cover more of the value chain. This has disrupted the CMO landscape. Despite being a regional industry 15 to 20 years ago when pharma outsourcing began, many CMOs are now international and tech-savvy. A handful are reaching the scale of big pharma and poised to become true partners; others are deciding whether to focus on technologies or regions or to cover more of the value chain (fig. 3).

Novel Business Models and Partnerships

Despite their strategic importance, CMOs are not always seen as true partners. We believe three business models will transform CMO–pharma relationships:

- Value-chain expansion. CMOs become strategic partners, offering pre-clinical development and research services to create a one-stop shop that covers the entire value chain of a product group.

- Flexible capacity. CMOs invest in equipment and facilities to build dedicated capacity and offer flexible production capacity with full-service capabilities for a specific product group.

- Risk sharing. CMOs reduce their prices but gain benefits if the product is successful (mostly small, virtual pharma players seeking to improve their credibility).

Several companies are already using these models. For example, Patheon has a flexible capacity partnership with Flexion Therapeutics and is responsible for building a manufacturing site, installing and validating equipment, and manufacturing Flexio’s FX006 drug. And Catalent has entered a value-chain expansion partnership with Mitsubishi Gas Chemical Company to promote Catalent’s GPEx technology in Asia. Catalent will engineer the cell lines and carry out development, and Mitsubishi will provide phase III and commercial manufacturing and use GPEx technology to offer biosimilar cell lines to pharma partners.

Charting a Path Forward

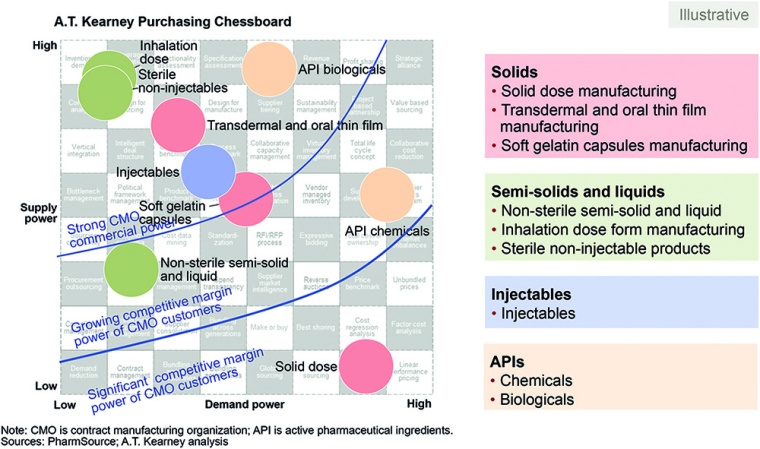

Strategic partnerships can yield an array of benefits, from lowering costs to improving production and supply chain performance. In addition, our Purchasing Chessboard sheds light on the demand and supply position of CMOs compared with the demand position of pharma companies (fig. 4). The top left quadrant shows where CMOs have a strong negotiating position; the bottom right shows where pharma companies can capitalize on competition among CMOs.

Based on our study and our project experience, we offer the following recommendations.

CMOs

- Evaluate your risks as a hybrid CMO. An unclear focus, such as on geographic reach or the technology portfolio, puts profitability at risk. As the market consolidates, smaller and hybrid CMOs are merging with other CMOs to control costs.

- Focus on profitable segments, or grow in scale. Concentrate on areas where you have the strongest supply power. CMOs with a focus on areas such as solid dose will need to improve their capacities quickly because price is a differentiating criteria and competition is high.

- Know your peers and their financial resources. No longer does outsourcing automatically lead to more CMOs. Pharma is now on the radar of large private equity firms that bet big on growth, as seen with Aenova and Stada.

Pharma Companies

- Know your partner and its network. Our Purchasing Chessboard can help you choose the right partners. Applications in the bottom right quadrant require partners with similar capabilities to compare prices, set up shorter contracts with regular price checks, and leverage the supply base in each geography. Those in the top left must monitor dependency, e.g., with regular market tests and a review of supply and quality performance.

- Watch emerging markets, especially in Asia Pacific. For new products ready to be launched in Asia, secure the supply with flexible CMOs that deliver products to the markets. CMOs are seeing growth in Asia, which pharma companies can secure by setting up or redesigning their Asian footprints.

The authors would like to thank Marc Berenbeck for his valuable contributions to this article

most read

US Tariffs Fatal for European Pharma

Trump's tariff policy is a considerable burden and a break with previous practice.

Q1 2025 Chemical Industry: Diverging Trends

The first quarter of 2025 highlights a continued divergence between the European and US chemical industries.

20 Years of CHEManager International

Incredible but true: CHEManager International is celebrating its 20th anniversary!

Pharma 4.0 – the Key Enabler for Successful Digital Transformation in Pharma

Part 1: Building a Business Case for Pharma 4.0

ISPE Good Practice Guide: Validation 4.0

The Validation 4.0 Guide provides a comprehensive approach to ensuring product quality and patient safety throughout a pharmaceutical product's lifecycle.