Chemical Distribution Outlook Generally Positive

But What About Those Clouds On The Horizon?

-

Günther Eberhard, Managing Director,DistriConsult

Günther Eberhard, Managing Director,DistriConsult -

-

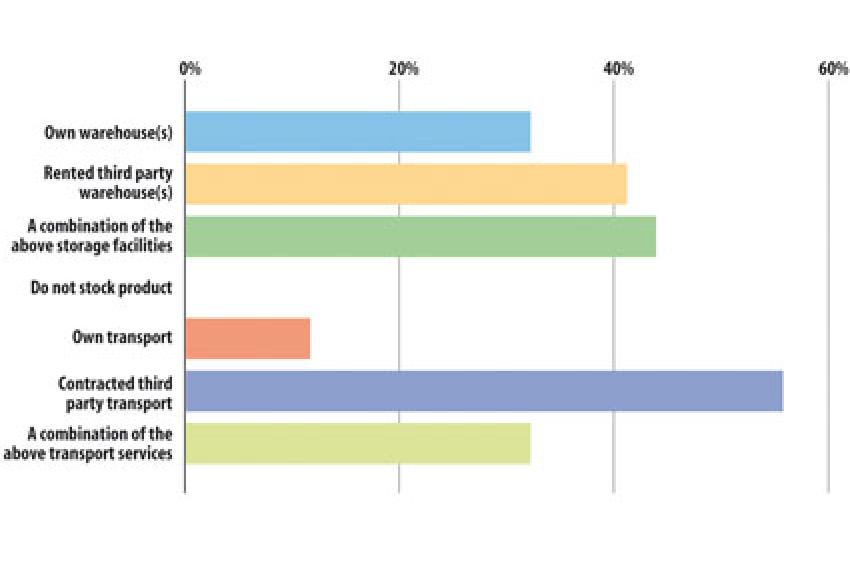

Warehouse and Transport Logistics in Specialty Chemicals © DistriConsult – Survey April 2011 (33 answers = 40% return rate; multiple answers possible)

Warehouse and Transport Logistics in Specialty Chemicals © DistriConsult – Survey April 2011 (33 answers = 40% return rate; multiple answers possible)

A Decent Start - When reading press releases of chemical distributors these days or when talking with their senior management, one can get the impression the economic crisis of 2008-09 is definitely a thing of the past. Sales volumes, turnover and profit figures for 2010 are across the board very satisfying and even in record territory for some companies. Also, companies in private ownership or controlled by financial investors that do typically not publish results will confirm in personal discussions that business was "very good indeed in 2010" and that 2011 has been off to a "very, very decent start."

In the next breath, however, many people will state that it is not easy to ensure the supply of products at the level that customers demand and when they want it. It appears that over the last 12-18 months, many marginal production plants were mothballed or decommissioned and scraped altogether. Sudden plant outages and unplanned maintenance shut-downs have led to availability problems every so often, so that a number of producers had to declare force majeure and go on allocation for certain products. This begs the questions as to whether the often-significant reductions of maintenance spending during the downturn - that may have helped profitability short term - were made at the detriment of the longer term outlook and viability of plants and their steady performance.

A Few Stumbling Blocks

For chemical distributors, this often results in the need to hold higher inventories than desirable under normal circumstances, in order to guarantee product availability at the customer level. This ties up additional working capital, on top of the higher raw material and product prices, which make replenishing stock more costly. The dramatic increase of crude oil price levels from about $65/barrel in the trough to more than $120/barrel in late April is to be felt with full effect here.

Cash flow calculations in quarterly or annual reports that show the cash consumption over the last year, talk a clear language here, despite all the efforts to optimize management of working capital, which were made at many companies. This is no easy task, as customers still keep ordering on short notice and/or in rather small lot sizes and deliveries. This is caused by their customers ordering late in the first place, but also by the fact that many small and mid-size customers find it hard to obtain financing in the run up to new and increased orders. The increase in cost of capital - that can be expected once central banks raise interest rates to keep inflation check - doesn't bode too well here.

So it's not all bright and shiny, despite the fact that particularly the industrial activity in Germany (and other "northern" countries in Europe) is "humming along nicely" as the Swiss daily "Tages-Anzeiger" wrote recently. During Q1 2011, Germany's annual gross domestic product rose by 5.2%, an increase not seen since reunification 20 years ago. On the other hand, the numbers don't look that good in other parts of Europe, and many economists warn of reduced growth, be it due to a continued rise in commodity prices or a general decline of the dynamics of the global economy.

Growth: Why Not Seek It Externally?

Besides internal growth driven by continued economic expansion, more and more distributors are considering external growth options. The larger M&A transactions reported in Q1 2011, however, were the closings of acquisitions that had already been published in 2010. Transactions that fall in that category are the MBO of the distribution activities of Ashland, which has been trading under the name Nexeo Solutions since the beginning of April; and Univar's acquisition of BCS and Quaron in Belgium and the Netherlands.

Nevertheless, there were also some "new" deals, such as the purchase of Quaron France by Kem (a 50/50 joint venture established for this purpose by German privately held distributors Overlack and Stockmeier); Univar's purchase of Eral-Protek in Turkey; UK-based Melrob's takeover of Japan's Chemiplus; the asset deal that Brenntag did with niche distributor Luwatec in southern Germany; and Azelis' acquisitions of Serbia's Finkochem and part of the S&D Group (Europe as well as Canada and India).

The last three transactions in particular show that the larger groups like Brenntag, Univar, Azelis and IMCD are more or less constrained to "bolt-on acquisitions" of comparatively small companies in Europe. Larger transactions would possibly lead to difficulties when trying to get clearance from EU or national competition authorities. It is therefore to be expected that these companies will increasingly focus on geographies like Asia Pacific or Latin America for their next M&A projects, a move that has also been confirmed by senior representatives of these firms in recent interviews.

M&A In Europe

This doesn't mean that nothing will happen in Europe regarding M&A. More and more privately held companies are considering acquisitions. Their shareholders, often families that have successfully managed generation changes and succession issues over the last few years, follow a long-term strategy that calls for reinforcement of core business activities and broadening their geographic footprint. These companies have reached a size bracket that, on one hand, allows them to manage mid-size transactions without undue financial strain; and, on the other hand, they are not yet too big, so that approval by competition authorities should not be an issue. What needs to be kept in mind, however, is that these companies are very circumspect, if not cautious, so that valuations will possibly be on the conservative side of the spectrum seen lately.

Distributors controlled by private equity investors are also good for flashy headlines at times.

One example is Azelis, where several media outlets recently reported that the owners, 3i, had commissioned an investment bank to explore "strategy options." Some industry watchers even suggested that a sale was imminent. This could very well be the case, or it could not! The only thing that can be said about private equity sponsors in chemical distribution (as opposed to other categories of shareholders) is the fact that there will ultimately be a sale. An exit is the only way to realize the value of the investment. When that exit will be in a particular case, however, is very difficult to predict from the outside, as there are many factors that influence such a decision. Not all of these are to be found on the level of the investment, i.e. the distribution company. Much more often, considerations regarding the portfolio of the investor and the funds that were used to make the investment in the first place play a significant role here.

Service Offering as the Main Differentiator?

While industrial chemicals distributors had to invest into storage tanks as well as blending and filling equipment all along, the case has been different in specialty chemicals. There it has been quite possible to run the business from a leased office, having just a third-party warehouse for packed goods to manage the supply-chain. The actual "investment" according to this business model was predominantly in human assets, hiring technically competent employees who had detailed product knowledge and an in-depth understanding of the target applications and/or industry segments.

Now there might be changes on the horizon as more and more customers are looking for enhanced services from their suppliers, which a distributor can only provide with an in-house laboratory infrastructure. Examples can be found in the cosmetics and the food industry, where new trends and developments need to be made accessible via an on-the-spot feel, smell or taste of a formulated product in front of the purchaser or the developer in order to generate sufficient interest for new additives and ingredients. But this also applies to certain technical applications. Add to that the fact that the application labs of the typical non-European producers are just too far away for a speedy turnaround of customers' technical problems and one can easily appreciate the fact that distributors must step in here. A number of companies are considering an investment in this area, as DistriConsult recently found out during a survey of specialty chemical distributors.

To build these often application-specific laboratories is a considerable investment, which makes significant demands on the financial capacity of a distribution company. Amortizing the investment within a reasonable pay-back time requires in turn a sufficiently big business volume. This can easily be generated by medium to large-sized companies, with activities across several countries. Small companies often only have the option to focus on a selected core industry sector or to abstain from providing this type of service altogether.

The survey mentioned above also yielded the result that when it comes to warehouses, the two models of in-house and third party facilities are equally used. Hybrid forms are also possible. The transport logistics, however, are outsourced almost completely to third-party logistics providers. The few cases where own trucks are used can be attributed to companies that have a significant activity in industrial chemicals, where often customized tank trucks are needed and are not easily contracted in from logistics companies in the open market.

Will The Consolidation Continue?

The general economic outlook can be considered as rather good, apart from the possibility of a sudden deterioration of the political situation in North Africa or the Middle East and any resulting dislocations in the global economy. However, further price increases for raw materials and petrochemicals and an accelerating inflation could increasingly cause problems, as there would be a dampening effect on demand. Product availability constraints and short-termism seen in customers' order patterns place high demands on distributors' infrastructure.

As an industry, chemical distribution will experience continued growth, since outsourcing of non-core activities by producers is likely to continue, a trend that opens further opportunities. It appears that also for specialty chemicals, additional services will be required by customers, be it the support through application development laboratories or customer specific blends and formulations, beyond what is already common in industrial chemicals. Reasons for that are that customers do not want to (re-)invest in the associated facilities or that producers continue outsourcing of small volumes handling and customised products, which are often blends of standard grades.

All this in turn requires distributors to show a willingness to invest in infrastructure. Not every company owner can or wants to do this. It is to be expected that a further round of consolidation will be triggered. It remains to be seen what type of distribution company will drive this. We expect the larger and more capable companies from the "Mittelstand" (SMEs) to eagerly seize the resulting opportunities across Europe.

Contact

DistriConsult GmbH

Säntisstrasse 69C

8820 Wädenswil

Switzerland

+41 44 680 1431

+41 44 680 1432