Leaving the Patent Cliff Behind

Global Pharma Increases R&D Productivity; Report Forecasts Prescription Drug Sales of $1 Trillion

-

© hywards - Fotolia.com

© hywards - Fotolia.com -

Figure 1

Figure 1 -

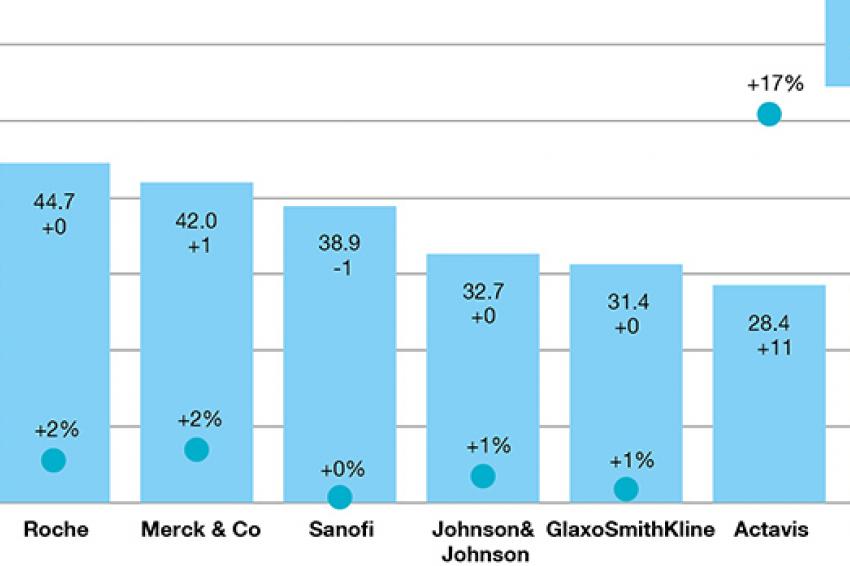

Figure 2

Figure 2 -

Figure 3

Figure 3

The pharmaceutical industry is entering a period of sustained growth. Prescription drug sales are set to advance at almost 5% a year until 2020, while worldwide prescription drug sales are expected to reach almost $1 trillion by 2020. This is the conclusion of the World Preview 2015 report from EvaluatePharma, a specialist in life science sector analysis and consensus forecasts.

The report, based on the company’s coverage of the world’s leading pharmaceutical and biotech companies and on consensus forecasts, says key prescription drug sales jumped 4.9% in 2014, driven by an 8.9% surge in US sales. In the same year, Europe returned to growth at 2.4%, while Japan slumped 2.6% in yen.

Increase in R&D Activities

In the view of the authors, the pharma and biotech industry is in very good shape. The patent cliff is firmly in the rearview mirror. Continued confidence in the sector is driven by a number of positive fundamentals including the recent increase in R&D productivity. The report mentions that worldwide pharmaceutical R&D totaled $141.6 billion in 2014, representing an increase of 3.1% on the previous year. Looking forward, R&D spend is forecast to grow 2% per year, compared with the compound annual growth rate of 3.4% between 2006 and 2014. The spend per new molecular entity (NME) was $2.7 billion in 2014, the lowest for at least the past seven years. This fall in spend per NME indicates increased productivity within the industry: Essentially, companies are containing R&D spend while achieving greater regulatory success.

EvaluatePharma highlights that this increased productivity has resulted in a big hike in drug approvals and the emergence of breakout drugs such as Gilead’s Sovaldi franchise. Excitement surrounding new products including Merck & Co.’s Keytruda, Bristol-Myers Squibb’s Opdivo and anti-PCSK9s from Amgen and Sanofi should ensure the sales momentum continues. The analysis company values the current total industry’s R&D pipeline at $493 billion. Within this, Gilead’s potential new combination hepatitis C product is seen as the most valuable drug.

The current industry feel-good factor has also been mirrored in the amount of money businesses are raising, the number of pharma and biotech companies floating on exchanges around the world, and the healthy appetite for M&A across the board.

The Biggest Players

EvaluatePharma finds that Novartis will remain the No. 1 pharmaceutical company through 2020 with total prescription drug sales of $53.3 billion, representing a 5.4% share of the entire world market. Actavis’ prescription drug sales are forecast to almost triple between 2014 and 2020, primarily as a result of its acquisition of Allergan in March 2015 and Forest Laboratories in July 2014. Celgene is forecast to debut in the top 20, rising nine places, by 2020 with its anti-cancer therapeutic Revlimid and its immunosuppressant Otezla adding a combined $6.6 billion to its 2020 prescription drug sales. Overall, global prescription drug sales are expected to grow, on average, 5% per year between 2014 and 2020 and reach almost $1 trillion by 2020.

Encouragingly for drug developers, despite the increased number of drugs approved, the quality of new drugs did not slip. Eight of the top 10 drugs approved in 2014 are forecast to have sales of more than $1 billion five years after launch.

Biologics On Its Way

The industry as a whole is expected to enjoy the benefits of the move toward biological drugs. Despite setbacks from some approved and clinical biological drugs depressing the speed of change, the global sales contribution from biologic drugs is forecast to jump from 23% in 2014 to 27% in 2020.

EvaluatePharma says these drugs have traditionally enjoyed greater patent protection than their small-molecule relatives, but the landscape is changing with the approval this year of the first US biosimilar.

Zarxio was given the green light in March but has yet to make it into pharmacies thanks to ongoing challenges from originator Amgen. Industry and legal experts also believe that navigating a legal pathway through the less than perfect US biosimilars legislation could hold up launch for several more months if not years.

Given the legal wrangling that is set to occur for biosimilars, and unresolved issues around substitution, analysis continues to show that the effect on branded products will be much softer than that of small-molecule generics. Thus biologics remains an attractive space for drug developers.

Oncology Largest Segment

EvaluatePharma finds that oncology will remain the largest segment in 2020 with an expected annual growth of 11.6% per year, reaching $153.1 billion in 2020. Growth from in-line products, and potential new entrants such as drugs targeting the PD-1 pathway, is expected to more than compensate for a number of key patent expiries between 2014 and 2020. Anti-diabetes is forecast to be the second biggest therapy area with sales of $60.5 billion in 2020, less than half that of oncology.

Humira Remains Top-Selling Product

Based on the authors’ opinion, AbbVie’s Humira will remain the No. 1 worldwide product in 2020 with sales of $13.9 billion. However, the threat of biosimilars has tempered the growth of the product with sales forecast to peak in 2017 at $16 billion. While Sovaldi debuts at No. 2 with sales of $10 billion, Opdivo, Bristol-Myers Squibb’s anti-PD-1 monoclonal antibody, leaps to third place in 2020 following its launch in 2014. Seven products currently in R&D are in the top 50, the biggest of which is Vertex’s Orkambi, a combination product for the treatment of cystic fibrosis, which is forecast to have sales of $5.1 billion in 2020. Collectively, Gilead’s hepatitis C franchise is forecast to sell $13.4 billion in 2020.

Some Clouds

The only clouds on what looks to be a sunny horizon for pharma and biotech are global pricing and market access. With many predicting that for the first time the industry could produce a series of real cures for previously intractable diseases, it is clear that these innovative drugs will come at a price. What is also clear is the growing reluctance of both government and private health-care providers to fund very expensive drug treatment regimens.

Recent pressure from health insurers in the US has seen pricing ground lost in both diabetes and respiratory drugs, with both GlaxoSmithKline and Sanofi reporting reimbursement hits. Gilead has also seen insurers trim the amount they are willing to pay for its pioneering hepatitis C drug. All this has led some to ask if we are seeing the end of pricing freedom in the US.

If the industry is to keep up the impressive growth of the last couple of years, which is predicted to continue, it will either have to accept lower prices for its products or persuade those who hold the purse strings that its products are indeed game changers and their benefits outweigh the cost of disease.

Contact

EvaluatePharma