Rethinking Carbon

How Europe’s Chemical Companies Can Win their Commercial Future

-

Laut einer aktuellen Studie von Simon-Kucher haben Führungskräfte der chemischen Industrie der Nachhaltigkeit höchste Priorität eingeräumt. | © Antony Weerut - stock.adobe.com

Laut einer aktuellen Studie von Simon-Kucher haben Führungskräfte der chemischen Industrie der Nachhaltigkeit höchste Priorität eingeräumt. | © Antony Weerut - stock.adobe.com

The European Chemical industry is facing a triple threat: Inflation, recession, and energy crisis. As a consequence, chemical companies are beginning to shift production and investments to North America or China. How can this be reconciled with the goal of maintaining production and jobs in Europe in the long term?

According to a recent Simon-Kucher panel study, environmental sustainability is now the priority for executives in the European chemical industry. How a company makes the transition from fossil fuels and feedstocks to alternative sources will determine its financial viability, competitive advantages, and ability to back up its sustainability claims with tangible improvements.

Rethinking carbon is not only an innovation challenge, but also a marketing challenge. Innovation will require time, engineering capacity, and top talent to shift companies away from an asset base that consumes too much expensive energy and emits too much carbon. Successful marketing will require strong value propositions anchored in quantifiable claims rather than high-level promises.

Four Actions that Leaders Need to Take

Leaders in the chemical industry should initiate these four actions as they rethink the role of carbon in their business.

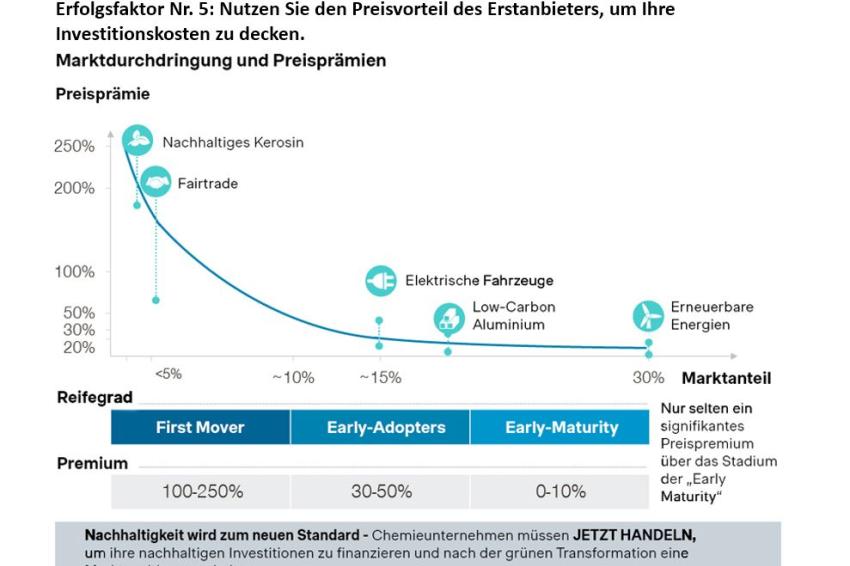

- 1. Pursue the green price premium as long as it exists

High premiums still exist for first movers to capitalize on in sustainable growth markets, as shown in fig. 1. Our experience determines that a premium of 20% is a reasonable target; up to 30% is also feasible in urgent situations.

The opportunity of achieving these premiums to diminish rapidly after the early maturity stage, as green becomes the new standard.

However, the positive effects of moving first extend beyond the purely financial advantages and flows toward innovation. The faster and better the upstream companies can innovate, the more opportunities their customers will have to innovate as well. This creates a vast opportunity for companies with the talent, infrastructure, and traditional expertise to assume the role of technological leadership. Germany, for example, has advantages in human capital that can outweigh current disadvantages such as access to reliable clean energy.

Energy-intensive production of fossil-based chemical commodities may continue to move to North America, the Middle East, or Asia. But European companies can still maintain their advantages in the development and production of innovative chemicals and materials.

- 2. Translate engineering performance into superior perceived value for customers

Enhancing lifecycle value propositions is a top priority requiring concrete and ambitious targets for physical emission reductions (Scope 1,2,3) and beyond.

Top managers plan to allocate around 20% of their time to drive R&D and investments. In contrast, they are spending less than 15% of their time on pure brand marketing campaigns. This reflects the idea that customers and consumers want actions with quantifiable impact rather than high-level messages that raise the risk of greenwashing. So, having a strong value proposition is more essential than ever, but it should be anchored in quantifiable claims rather than bold, high-level promises. This means educating customers on carbon footprints and emissions savings rather than making general claims.

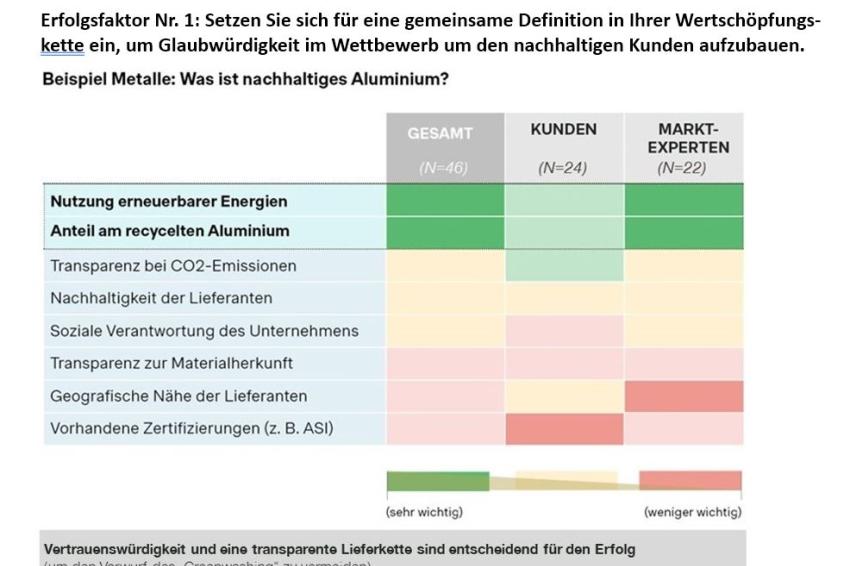

A leading aluminum producer wanted to strengthen its value proposition and asked customers which dimensions of sustainability were important and which were hygiene factors.

Certifications, claims of social responsibility, and geographical proximity of suppliers play a less important role for customers than information on how much renewable energy and how much recycled aluminum the company uses.

Managers also expect to spend about a third of their time on establishing a transparent, trustworthy chain of custody of material and reduce their own Scope 3 emissions through alternative, low-carbon feedstocks. Beyond increasing operational flexibility, they will focus over 40% of their time on value chain reconfiguration and feedstock transformation.

- 3. Capitalize on the synergies from sustainability and digitalization

Digitalization has always had the immense potential to enable cost savings and drive revenue growth. Sustainability will not supersede digitalization. In fact, digitalization will play an essential role in helping companies communicate transparently on emissions and collaborate with customers and suppliers on sustainability objectives.

Let’s look at two examples of the synergies of sustainability and digitalization:

Enabling cost savings: Several German automakers have formed a new cloud-based platform called Catena-X to help reduce CO2 emissions and make resource consumption more efficient. The platform will use a digital supply chain to determine the CO2 emissions in the production of a vehicle.

Driving revenue growth: Some 88% of participants believe that transforming to a more data-driven business will enable their company to capture revenue growth opportunities. One example is metals company Klöckner’s ability to precisely calculate product carbon footprint and document tangible CO2 reductions. Customers can incorporate the emissions data and comply with regulatory requirements, measuring their own sustainability targets.

The rationale is that increased visibility and communication make it easier for chemical companies to do business with their customers. Around 74% of the respondents observe that customers are increasingly expecting a more digital and more seamless buying experience.

- 4. Achieve energy security and diversity

Electricity prices have remained persistently high in Germany throughout spring 2023. While many companies can tolerate prices that are higher than historical average, these increased prices may do much more than suppress short-term profits. They can also act as a brake on the long-term investments the chemical sector in Germany and other European countries urgently need.

In a press release in May, Lanxess CEO Matthias Zachert stressed the importance of “competitive energy prices” as well as faster approval procedures, better infrastructure, and an industry-friendly attitude. Emphasizing the prevailing conditions in Germany, Zachert added that “[if] we want our home country to be able to compete internationally in the future, we have to act now. Create the right framework conditions now. Only then can we as an industry also make a powerful contribution to maintaining our nation’s prosperity.”

Sufficient, reliable, affordable, and stable supplies of electricity and hydrogen from renewable sources will underpin the economic transition to new carbon platforms. Energy security and diversity are ways for European suppliers to increase resilience and to confidently make the first moves to finance their green transition and meet customer demands.

Volatile supply dynamics are expected to accelerate the push to diversify energy sources — and toward renewables in particular — faster than regulatory frameworks will require. In other words, the accelerated shift becomes a source of competitive advantage and not merely a compliance obligation.

The Time to Act Is Now

There’s never been a more apt time to act than now when the chemical industry is reeling under the triple threat of inflation, recession, and energy crisis. Executives recognize that accelerating the green transition can become a “win-win-win” opportunity to meet new demand, increase resilience, and improve margins. It is about accelerating growth and mitigating cost risks at the same time.In other words, waiting is not an option.

As BASF CEO Martin Brudermüller said in an interview with the German newspaper Handelsblatt, “Protecting the environment affects each and every one of us. It is clear what is happening and there is not much time left. And that is a huge opportunity.”

Jan Haemer, Partner Chemicals & Materials, Simon-Kucher,

Frankfurt am Main, Germany;

Andrea Maessen, Senior Advisor Chemicals & Materials,

Simon-Kucher, Cologne, Germany

-

Abb. 1: Preisaufschläge schaffen einen starken Anreiz für Chemieunternehmen, jetzt zu handeln. | © Simon-Kucher

Abb. 1: Preisaufschläge schaffen einen starken Anreiz für Chemieunternehmen, jetzt zu handeln. | © Simon-Kucher -

Abb. 2: Faktenbasierte Wertversprechen schaffen Vertrauen. | © Simon-Kucher

Abb. 2: Faktenbasierte Wertversprechen schaffen Vertrauen. | © Simon-Kucher

-

Jan Haemer, Simon-Kucher | © Simon-Kucher

Jan Haemer, Simon-Kucher | © Simon-Kucher

-

Andrea Maessen, Simon-Kucher | © Simon-Kucher

Andrea Maessen, Simon-Kucher | © Simon-Kucher