US Markets Drive Global Reallocation and Growth

Changing The Industry - The global chemical industry is in a state of flux. The Asian economies, which have been the growth engines of the chemical industry for the last decade, have recently seen some slowing down; meanwhile, the U.S. chemical industry is coming out of its slumber.

The advent of shale gas in the U.S. has been a game changer for the industry. Huge availability of cheap shale gas, used both as feedstock and fuel in the chemical industry, has created a competitive advantage for U.S. manufacturers.

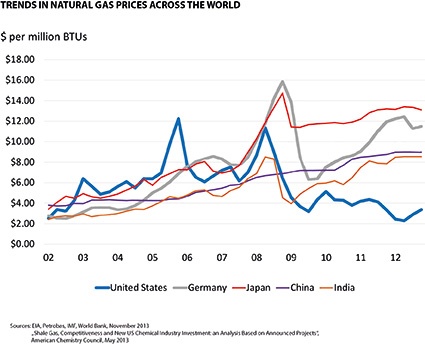

Natural gas prices in the U.S. decreased by 64%, from about $11 per million British thermal units in 2008 to less than $4/mmBtu in 2013. The sharp decline was largely due to increased supply from the discovery of vast shale gas reserves in the U.S. It is estimated that the increased supply can fulfill gas demand at current levels for about 200 years.

Abundant availability and consequently significantly lower gas prices have led players in the chemical industry to fundamentally reshape their long-term growth strategy.

Increasing Investment in U.S. Chemical Industry

Improved production costs for chemical companies have driven the reallocation of funds and resources to the U.S. A large number of greenfield and expansion projects have been announced. From 2010 through the first quarter of 2013, almost 100 chemical projects based on shale gas and valued at $71.7 billion were announced; about half of these investments are made by foreign companies, according to the American Chemistry Council.

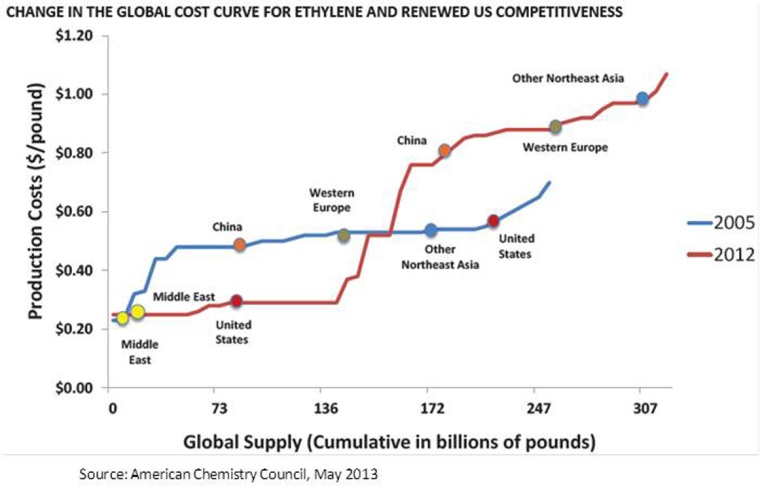

The majority of investments are being made around bulk petrochemicals, mainly ethylene and its derivatives - the major beneficiaries of the shale boom. Since 2005, the U.S. ethylene industry significantly improved its competitive position compared with China, Northeast Asia and Western Europe. From 2005 to 2012, U.S. production costs were halved and are now far below production costs in China, Western Europe and Northeast Asia.

The abundant supply of cheap shale gas is expected to enable the U.S. to maintain its production cost advantage for the foreseeable future. This has resulted in a large number of foreign companies entering the U.S. for shale-advantaged manufacturing. Nine new steam crackers in the U.S. have been announced with several more under consideration.

Focus On Sustainable Growth

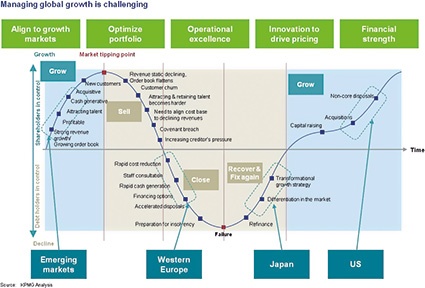

To ensure a transition toward a robust product and service mix, some companies have made mergers and acquisitions (M&A) while others are pursuing restructuring plans and have shed non-core assets. The U.S. growth trend evident in the number of acquisitions and non-core disposals is in stark contrast to Western Europe and Japan, where companies are in a more challenging phase focused on cost reduction.

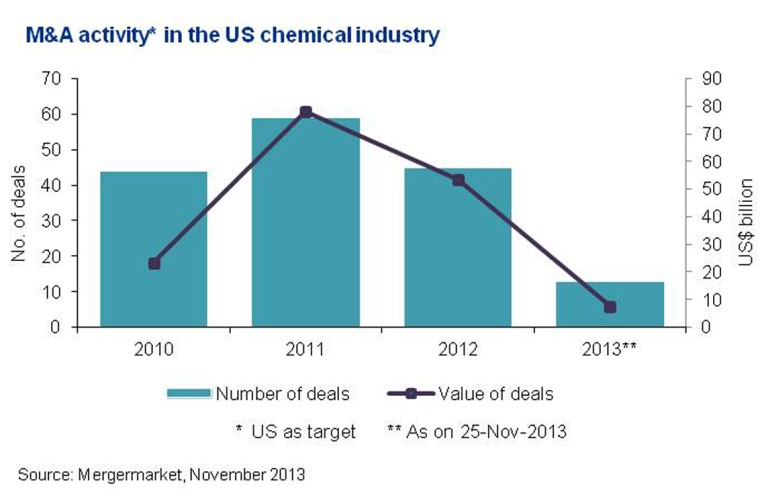

M&A Activity in U.S. Chemical Industry

Domestic and international chemical companies increasingly focus on achieving a disciplined product portfolio and streamlining operations in the U.S., which has led to renewed interest in M&A activity in the country. However, deal activity in the past few quarters has been limited - as a result of economic slowdown in Asia, continued weakness in Europe and uncertainty surrounding U.S. economic policies.

Shale-based M&A activity has started to pick up. Early in 2013, Georgia Gulf Corp. completed its merger with PPG's commodity chemicals business, creating Axiall Corp. - a company that integrates chemicals and building products. Axiall Corp. benefits from North America's natural gas cost advantage as well as the recovery of the U.S. housing market. In addition, opportunities in fracking services are driving interest in the gas extraction market. Chemical producers, active in this area, plan to strengthen their position in the energy services market. Solvay's $1.3 billion acquisition of Chemlogics and Ecolab's $2.3 billion acquisition of Champion Technologies are recent examples.

While large chemical producers in the U.S. focus on domestic investments for attractive returns due to low-cost raw material, foreign players are inclined to acquire specialty chemical assets to boost their growth in the U.S. During the last few months, Altana, a European specialty chemicals company, has made several acquisitions of U.S. chemical companies - for instance, the $635 million acquisition of Rockwood's Performance Additive segment and the acquisition of Henkel's Specialty Coatings business.

Moreover, the revival of the U.S. construction market is expected to support M&A activity in the building and construction space of the chemical industry - coatings, adhesives and sealants. The U.S. construction industry is expected to grow 9% in 2014, compared to an estimated 5% in 2013.

Private Equity Buyers Will Also Be Active

In the U.S., private equity (PE) investors have been active in the commodity chemical industry as evidenced by some recent large purchases, including Carlyle Group's $4.9 billion acquisition of DuPont's powder-coating business. There is limited activity in the specialty chemicals area; given the high-deal multiples, strategic buyers can better price and leverage synergies. Recent examples in the specialty chemicals space include Platform Acquisition Holdings' $1.8 billion acquisition of MacDermid Inc.

Conclusion

The U.S. economy has yet to overcome its difficulties, and regulatory uncertainty persists. Recent signs of slowing growth in Asian economies, particularly China, and a subdued economic environment in Europe may affect the revival in global chemicals demand.

However, on the back of significant cost advantage in fuel and early signs of economic revival, the U.S. chemical industry is witnessing a vibrant phase. The low cost of manufacturing and abundant supply of raw material has resulted in global companies shifting their manufacturing bases to the U.S. This has led to both organic and inorganic growth opportunities for the chemical companies and has driven M&A activity in the industry.

Company

KPMG AG Wirtschaftsprüfungsges.Tersteegenstr. 19 -31

40474 Düsseldorf

Germany

most read

Dow to Shut Down Three Upstream European Assets

Building on the April 2025 announcement, Dow will take actions across its three operating segments to support European profitability, resulting in the closure of sites in Germany and the UK.

Merck Acquires Chromatography Business from JSR Life Sciences

Merck to acquire the chromatography business of JSR Life Sciences, a leading provider of CDMO services, preclinical and translational clinical research, and bioprocessing solutions.

Novo Nordisk to Cut 9,000 Jobs Globally in Major Restructuring

Novo Nordisk announced a global workforce reduction of approximately 9,000 positions to streamline operations and reinvest DKK 8 billion (€1 billion) in growth opportunities for diabetes and obesity treatments.

BASF Sells Majority Stake in Coatings Business

BASF sells a majority stake in its coatings business to the investor Carlyle.

VCI Welcomes US-EU Customs Deal

The German Chemical Industry Association (VCI) welcomes the fact that Ursula von der Leyen, President of the European Commission, and US President Donald Trump have averted the danger of a trade war for the time being.