The Chemical Industry in China and the Middle East

Cooperation Or Conflict?

-

Fig. 1: Schematic Value Creation Process of the Chemical Industry

Fig. 1: Schematic Value Creation Process of the Chemical Industry -

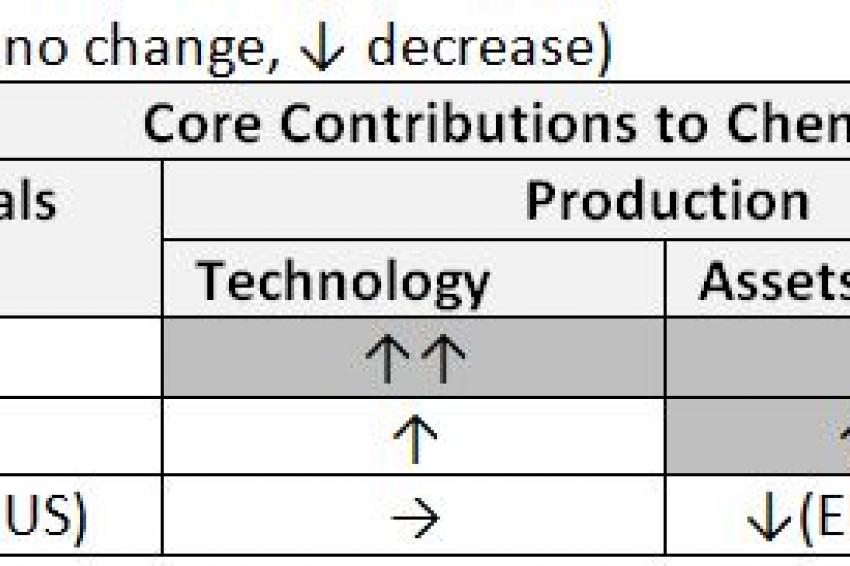

Table 2: Trends for core contributions to chemical industry by region.

Table 2: Trends for core contributions to chemical industry by region. -

Table 1: Current Core Contributions to Chemical Industry by Region.

Table 1: Current Core Contributions to Chemical Industry by Region. -

Dr. Kai Pflug, CEO, Management Consulting

Dr. Kai Pflug, CEO, Management Consulting -

The global chemical industry is no longer dominated by the Western world. Kai Pflug looks at the rise of China and the Middle East. © Picture: Anatoly Maslennikov - Fotolia.com

The global chemical industry is no longer dominated by the Western world. Kai Pflug looks at the rise of China and the Middle East. © Picture: Anatoly Maslennikov - Fotolia.com

Challenging The West - For most of the 20th century, the global chemical industry was dominated by the Western world (Western Europe, North America and Japan as an honorary member of the club). However, in the first decades of the 21st century, other countries and regions - in particular the Middle East and China - are challenging this dominance.

Simplistically speaking, the chemical industry turns raw materials into marketable products via industrial processes that require both physical assets and technological know-how (fig. 1). In this regard, the chemical industry does not fundamentally differ from other producing industries.

Strengths And Weaknesses

For the chemical industry, oil and gas will probably remain the most important bottleneck among the raw materials in the next few decades. Of course there are other important raw materials as well, particularly for inorganic chemicals and for specific areas such as fluorochemicals or rare earths, but generally these are either more evenly distributed globally, or of lower importance to the industry, or both. In addition, there are attempts to replace petrochemical value chains by those based on bio-sourced materials, but at current prices these are probably not fully competitive yet.

Among the three regions examined, the Middle East clearly has the best position regarding the most important chemical raw materials. The abundance of oil and gas is the region's main competitive advantage as these resources by far exceed the resources of these and related raw materials (e.g., coal) in other regions.

In contrast, China - though a big oil producer itself - strongly depends on import of petrochemical raw materials, and this is unlikely to change despite the strong political will to self-sufficiency and progress in coal chemistry and bio-based materials. The Western world is also generally a net importer of petrochemical raw materials, though the more recent developments in shale gas have reduced the dependency of at least North America on imports.

In terms of production capabilities, some distinction can be made between physical assets (i.e., existing chemical plants) and production knowledge (both on a high level such as technologies for license and on the level of the skills of typical chemical engineers). However, in both aspects Western companies have a clear lead as they have both a much deeper base of intellectual property and related knowledge and a broader and more highly developed portfolio of production assets.

In contrast, the Middle East is comparatively weak regarding production capabilities and still primarily relying on Western expertise as the region historically lacks both experiences with production in general and a long-established education system to provide a sufficient number of qualified scientists.

China's expertise is already a bit more developed, but focused mostly on basic chemicals, particularly in the state-owned companies. In contrast, in high-value areas such as specialty chemicals, China still lacks the knowledge and assets to provide a broad and diversified portfolio despite strong political will to move in this direction. Overall, the West is still the key knowledge-carrier the rest of the world relies on, be it via imitation, licensing or hiring of expats.

As for customers and markets, the main development in the last decade has been China becoming the biggest chemicals market in the world. This is China's biggest asset, and it obviously includes not only those chemical products consumed by Chinese end customers but also those used for production of finished goods that are later exported from China. In contrast, the local chemicals markets of the Middle East are relatively irrelevant. Finally, the Western world is certainly an important market for chemicals, particularly for those focusing on higher-end market segments. Table 1 summarizes the relative contribution of the three regions to the global chemical industry.

Trends

In the medium term, these contributions are likely to change somewhat (table 2). China is likely to develop much stronger production capabilities both on the level of assets and the level of know-how, while the Chinese chemicals markets will also further increase in importance. (Despite the recent slowdown of the Chinese economy, growth is still much higher than in most other regions).

The Middle East is massively expanding its production assets, trying to move downstream in the chemicals value chain to capture a larger share of the overall value created in petrochemicals. However, in the near future this shift will be more on the level of assets (which can be established in a few years) than on the level of knowledge on all relevant levels (which will probably take decades or more).

For the Western world, shale gas will lead to a divergence in development between the U.S. on one side and Europe/Japan on the other side. Shale gas increases the raw materials supply in the U.S. and will therefore also lead to higher investment in production assets while the larger scarcity of suitable raw materials in Europe and Japan will probably lead to a long-term loss in production assets there.

Consequences

Currently each of the three regions has a fairly specific contribution to the overall global chemical industry: raw materials (Middle East), markets (China) and production technology (West). This opens the way for collaboration between the regions, which has already begun, for example the three-way cooperation between Shell, PetroChina and Qatar Petroleum to build a refinery in Zhejiang.

In the long run, given the developments anticipated in table 2, there is also a distinct possibility for cooperation only between the Middle East and China. As both these regions (and particularly China) increasingly develop production technology and assets, the current role of the West as a contributor will be threatened. For the resulting two-way cooperation between the Middle East and China, the technology component will probably determine the stronger position as the advantage in raw materials will always stay with the Middle East while China will always have better market access. The most likely outcome is a situation in which most of the upstream technology up to base chemicals lies with the Middle East and the downstream/specialty technology with China. However, it is not clear whether this will be acceptable for the chemical state-owned enterprises, whose current strength is more on basic chemicals technology.

In conclusion, both the Middle East and China need each other as their strengths in raw materials and market access complement each other. Cooperation may be facilitated by the somewhat similar governance status of the key companies on both sides - the respective governments heavily dominate both.

Conflicts may arise over where exactly to hand over the value-creation process from the Middle East to China. This will be decided both by the alternatives both parties have (and thus their respective bargaining positions), and their technology level. Very high-volume bulk chemicals will likely be more suited to production in the Middle East while highly specialized or customized, low volume, labor- and research-intensive chemicals are more suited to production in China. Chemicals somewhere in between will be the most interesting to watch.

Contact

Managm. Consult. Chemicals

RM1302, 13/F CRE Bldg.

Wanchai, Hong Kong

China

+86 1368 1873992