New Biologics and Advanced Therapies

The pharmaceutical market is undergoing a profound transformation, driven by innovation among biologics and advanced therapies (ATs). This shift is not only redefining the treatment landscape but also presenting new opportunities and challenges related to the drug development and manufacturing value chain.

The pharmaceutical market is undergoing a profound transformation, driven by innovation among biologics and advanced therapies (ATs). This shift is not only redefining the treatment landscape but also presenting new opportunities and challenges related to the drug development and manufacturing value chain.

With this backdrop, contract development and manufacturing organizations (CDMOs) play a pivotal role in enabling sponsor companies to bring groundbreaking therapies to patients.

The Dynamic Growth of Biologics and ATs Market

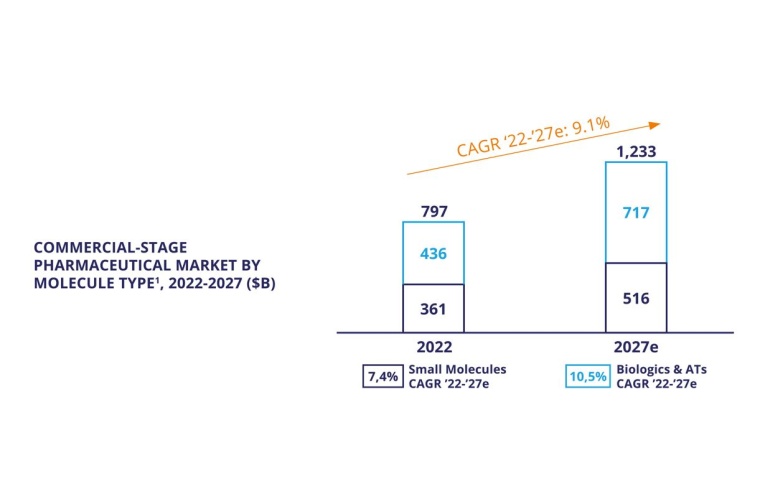

In recent years, the biologics and ATs market has experienced substantial growth, driven by intensive R&D efforts and breakthroughs in expression systems and manufacturing techniques. Challenges remain, especially the need to scale production to meet the large commercial opportunity. Forecasts suggest the biologics and ATs market will exceed the market for small molecules by $201 billion by 2027, supported by a projected 10.5% compound annual growth rate (CAGR) from 2022 to 2027. Note that all data are from Alira Health’s “2023 Biologics & Advanced Therapies Contract Manufacturing Report.”

Unveiling Market Dynamics: Trends by Therapeutic Class

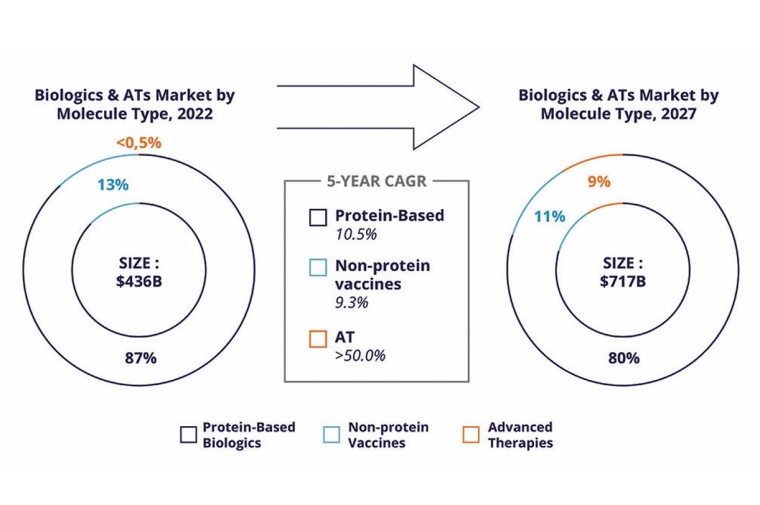

As of 2022, protein-based biologics made up the majority of commercial biologics and ATs, comprising 87% of the market ($376 billion), followed by non-protein vaccines at $58 billion and ATs at $2 billion.

The rapid development and market release of Covid-19 vaccines has been a transformative force in the biologics and ATs landscape, driving momentum for the regulatory approval of non-Covid-19-related innovative therapies. Despite pandemic-related challenges, the United States (US) and the European Union (EU) maintained or increased annual approval rates for biopharmaceuticals in 2020 and 2021, showcasing industry resilience. The effectiveness of biologics and ATs against Covid-19 has continued to drive investments in R&D. This trajectory is projected to drive a substantial $281 billion growth in the biologics and ATs market over the five years from 2022 to 2027. Looking ahead to 2027, protein-based biologics are likely to maintain dominance with 80% of the market, while ATs are expected to grow to 9%. A notable trend is the rising demand for viral vector manufacturing, prompting considerable investments by CDMOs and transformative acquisitions.

The Evolving Landscape of Research and Development

The innovation pipeline for biologics and ATs is deep, with 23,718 therapies in development. Early developmental assets, including both discovery and pre-clinical stage, make up 67.1% of this array 15,924 products. Notably, antibodies and cell and gene therapy products take the lead as extensively developed therapies, contributing to over half of pipeline products across various stages, signifying their role in advancing medical treatments.

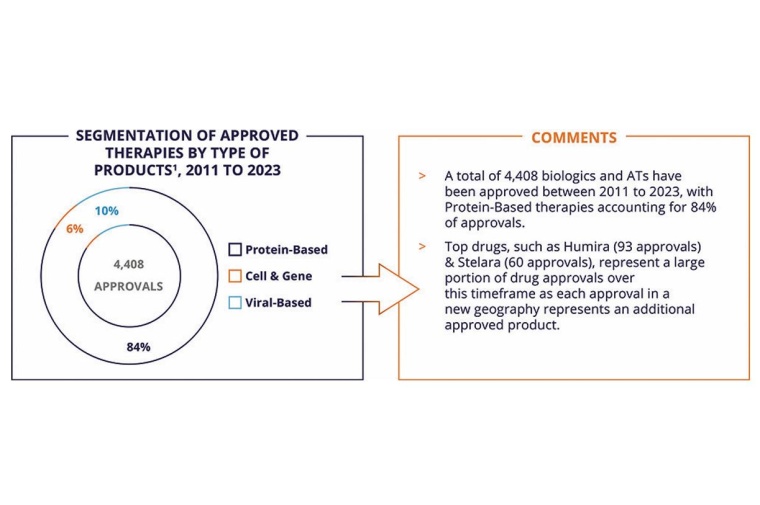

Oncology emerges as the dominant clinical indication, boasting an impressive 9,000 pipeline products dedicated to various facets of this crucial therapeutic area. From 2011 to 2023, a notable 4,408 biologics and ATs secured regulatory approval worldwide, with protein-based therapies comprising 84% of these approvals. Blockbuster monoclonal antibodies like Humira, with 93 approvals, and Stelara, with 60 approvals, significantly shape the landscape, with each approval in a new geographical region amplifying their significance and expanding the range of approved products.

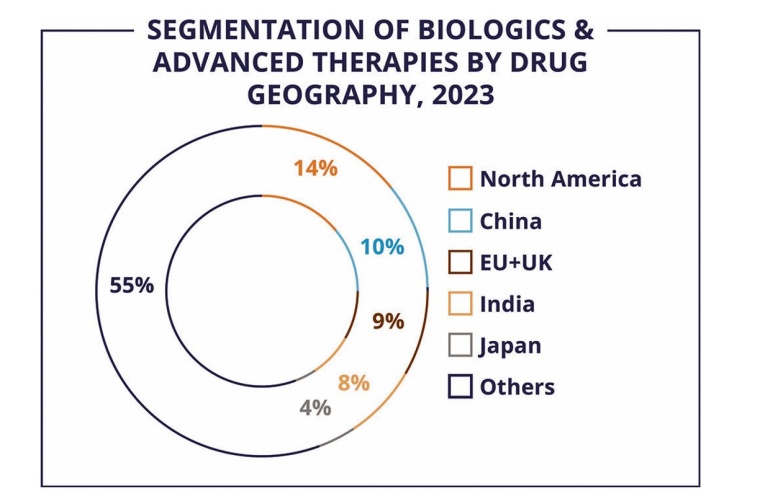

Considering key geographical regions in which biologics and ATs are developed, North America leads at 14%, followed closely by China at 10%. The EU+UK regions follow at 9%, with India at 8% and Japan at 4%. Collectively, these five regions contribute to a significant 45% share of the entire biologics and ATs market as of 2023.

CDMOs: Opportunities & Challenges

The increased funding in R&D activities and the growth outlook for the demand of biologics and ATs are formidable drivers for the CDMO industry.

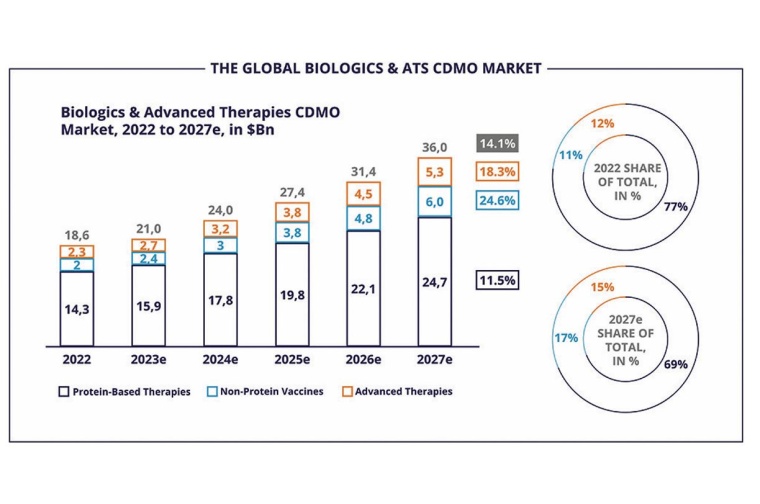

As of 2022, the estimated value of the biologics and ATs CDMO market is $18.6 billion. This value is anticipated to grow at a remarkable CAGR of 14.1%, reaching $36 billion by 2027. The surge is driven by increasing demand in all three segments (biologics, non-protein vaccines, and ATs). Specifically, the last two segments combined are on track to constitute 32% of the total market by 2027, up from 23% today.

The protein-based segment, holding the highest market share, is anticipated to grow at an 11.5% CAGR from 2022 to 2027, while the bulk of the expected market growth is propelled by non-protein vaccines and ATs, projected to grow at impressive rates of 24.6% and 18.3%, respectively.

As a result of this impressive market growth, CDMOs aspiring to lead in biologics and ATs manufacturing are venturing into the integration of technologies capable of addressing the evolving landscape.

The landscape is rich in opportunities and challenges. For example, one of the critical drivers of the demand for contract services is the patent expiration of many biologics and ATs and the rise of biosimilars. Biosimilars enjoy global policy support in response to escalating healthcare costs, exemplified by the EU’s biosimilar approval pathway. As intellectual property protection for originator biologics and ATs diminishes, biosimilar manufacturers are enabled by the support of CDMOs, which can provide a rapid turnaround and lower manufacturing costs while ensuring supply chain flexibility.

The vibrant growth of the ATs sector, including cell and gene therapy products, is another major boost to CDMOs. ATs sponsors hold the potential to address previously untreatable diseases, drawing substantial research and investment focus. However, challenges persist, with burgeoning demand outstripping manufacturing capacities. Ensuring product stability and quality introduces complexity, raising concerns over automation and scalability. CDMOs provide ATs sponsors with the critical capacity and quality necessary to make them successful.

Finally, the complexity of manufacturing cell therapy products creates major opportunities for CDMOs. Sponsors may lack the internal capabilities to efficiently identify, validate, and deploy processes, particularly for autologous cell therapies. Scaling these operations requires deep expertise and robust process development capabilities, which CDMOs can supply to the industry.

In summary, sponsors of biologics and ATs products will increasingly seek CDMOs as external manufacturing partners to enhance production, optimize capacity, reduce costs, and create a secure supply chain. CDMOs must navigate the opportunities and challenges driving the biologics and ATs field, while supporting the entire spectrum of development, manufacturing, and therapy delivery.

The Biologics and ATs CDMO Landscape

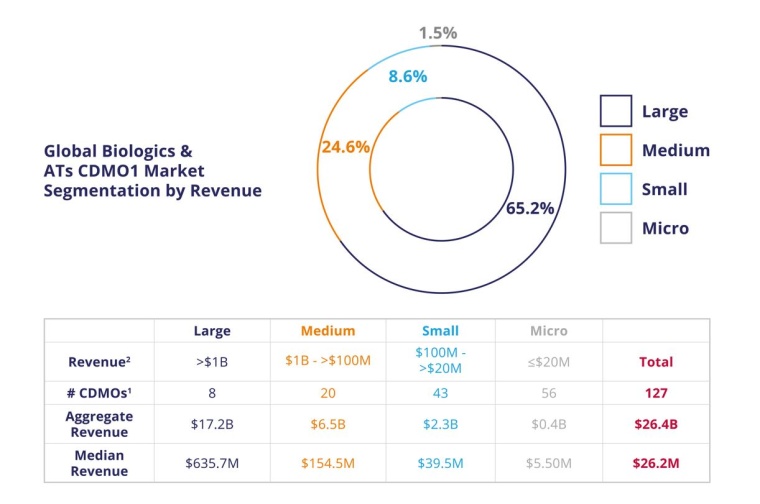

Large CDMOs currently command the majority share at 65.2% of the global market, but the rise of small and micro competitors is set to fuel innovation and consolidation within the sector. The competitive landscape is primarily shaped by eight large players, each generating revenues of $1 billion or more, who together constitute 65% of total revenue for the CDMO market. Medium players contribute an additional $6.5 billion, so that large and medium players combined represent nearly 90% of the total revenue.

Despite the prominence of small and micro manufacturers on the global biologics & ATs outsourcing scene, they together represent a modest 10% of total CDMO revenue due to capacity constraints. This fragmentation offers several attractive opportunities for industry consolidation in the coming years.

Pivotal Role for CDMOs in an Evolving Landscape

In conclusion, the evolving landscape of biologics and ATs is reshaping the treatment paradigm while introducing a spectrum of opportunities and challenges. Companies with novel therapies will increasingly look to CDMOs to bridge the gap between innovation and patient access. CDMOs must balance growth with adequately addressing the challenges posed by complex manufacturing processes. As the biotech sector propels forward, CDMOs will continue to play a pivotal role in enabling the realization of groundbreaking treatments.

Authors: Carlo Stimamiglio, Partner,

Transaction Advisory Practice,

Alira Health, San Francisco, USA

Alexandra Wollersheim, Partner,

Transaction Advisory Practice, Alira Health, Munich, Germany

Filippo Pendin, Principal,

Transaction Advisory Practice, Alira Health, Los Angeles, USA

most read

Relocation of Chemicals Production Footprint in Full Swing

A new Horváth study based on interviews with CxOs of Europe’s top chemical corporations reveals: The majority of board members expects no or only weak growth for the current year.

ISPE Good Practice Guide: Validation 4.0

The Validation 4.0 Guide provides a comprehensive approach to ensuring product quality and patient safety throughout a pharmaceutical product's lifecycle.

Lead or Lag: Europe’s AI Materials Race

How AI and Robotics are reshaping the race for materials discovery.

20 Years of CHEManager International

Incredible but true: CHEManager International is celebrating its 20th anniversary!

Q1 2025 Chemical Industry: Diverging Trends

The first quarter of 2025 highlights a continued divergence between the European and US chemical industries.