Pharmaceutical Logistics: The African Journey

Time to Understand and Improve Your Pharma Distribution Footprint in Africa

-

(c) erichon/Shutterstock

(c) erichon/Shutterstock -

Andreas Gmür, Camelot Management Consultants

Andreas Gmür, Camelot Management Consultants -

Constantin Reuter, Camelot Management Consultants

Constantin Reuter, Camelot Management Consultants -

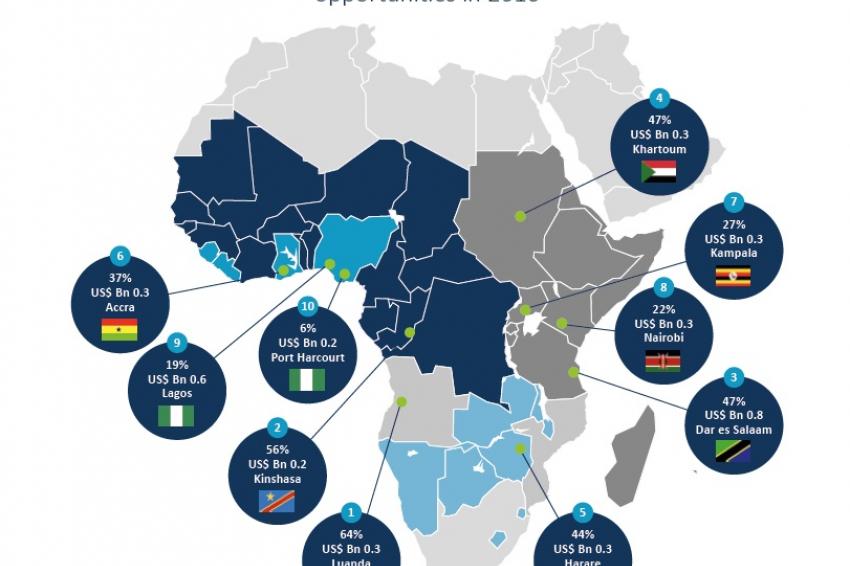

Figure 1

Figure 1 -

Figure 2

Figure 2

Africa is one of the most promising pharmerging markets. For a recent project, pharma supply-chain experts from Camelot Management Consultants visited more than a dozen countries in Africa to gain a detailed picture of current pharma distribution capabilities for 2-degree to 8-degree Celsius distribution. Their conclusion: Now is the time for pharma companies to reshape their African footprint and thus prepare themselves to secure future growth opportunities.

With a total population of 1.2 billion and increasing wealth among the middle class, the African pharma market is expected to reach a compound annual growth rate (CAGR) of 8%-11% resulting in an overall market opportunity worth $35 billion by 2020.

Opportunities and Challenges in Africa

By 2050 Africa is expected to exceed the population of China and India, with 60% of Africa’s population being urbanized by 2050 and the number of middle-class households amounting to 130 million as early as 2020. The traditional medicine-man culture is changing and with this, the domestic demand for high-quality, international-standard medicines, diagnostics and prevention is increasing. Millions of patients are not diagnosed and not receiving treatment yet, which represents a multimillion-dollar opportunity. The potential of new innovative medicines should not be underestimated either.

Despite these promising developments, pharma distribution on the African continent still faces some significant challenges and risks. Problems with security, unstable political situations, and the fact that 30% of the medicines sold are counterfeit are the key issues. It is definitely a challenge to find a well-established infrastructure and to be able to distribute pharma products within controlled environments and the required temperature ranges.

With distribution often managed by third-party distributors and several subcontractors, the actual processes and mechanisms of the markets are still not very transparent for a lot of pharma companies. In consulting projects with pharma producers, Camelot has found cases where — even to the surprise of the pharma producer — the price add-ons by various parties were at patient level adding 70% to 200% of the pharma company’s initial product price.

This is one of the reasons pharma companies increasingly demand enhanced transparency and stronger control over the distribution of their own products in the African market.

Africa Does Not Equal Africa

Africa consists of 54 complex and diverse markets, which, as a result of European colonialism, are highly heterogeneous in their economic evolution, pharmaceutical growth, business ethics, languages and trading blocs. To build up a successful and sustainable pharma-distribution operation, the peculiarities and key characteristics per country and region need to be evaluated carefully.

The North African countries, which are often considered part of the Middle East business region, are where pharma distribution is best established today. Central and Southern Africa can be categorized into six subregions: French-West Africa, East Africa, Southern and South Africa, Niger Region, and Portuguese Africa. The differences among these regions, e.g., regarding import regulations, language, or air and sea connections, need to be considered when designing the distribution strategy for Africa.

Depending on the products and market situations, alternative distribution solutions might be established for prioritized countries, assuming a critical volume of product sales is reached. With the growing demand for medicines, new opportunities and new infrastructure developments are currently evolving rapidly in the African markets and are attracting a wide range of investors. Getting the distribution of pharma products under their own control will certainly help pharma companies to better control the flows, increase sales and also reduce the prices and improve quality for the patients — resulting in a more profitable and economically sustainable business in Africa.

Getting to Know the Market

Building relationships with the different pharmaceutical stakeholders (e.g., pharmacies, wholesalers, doctors, public officials, banks) is key to the success of pharmaceutical suppliers in Africa. Therefore, it is very important to have a strong local workforce, either provided by the pharmaceutical company directly or through its appointed distributor. It is very helpful to go to the “shop floor” in the market to get a feeling of how business is done and to collect special information, e.g., visit pharmacies to find out about “special” product prices or whether life-saving products are constantly available.

New Logistics Solutions on the Horizon

Logistics infrastructure for pharmaceutical products is generally acceptable at least in the big cities, and in some cases it meets high standards at the main distributor/wholesaler level. However, the infrastructure and storage conditions of secondary wholesalers are very poor. The reason is that compliance monitoring is generally not strongly enforced along the supply chain because of the limited margins the secondary wholesalers make.

In the past, road transportation was very insecure, so many pharma companies exported pharma directly into the countries via airfreight into the main cities. Because destination airports lack cold-storage capacity, distributors have to pick up the goods immediately to ensure proper cool-chain handling. However, in the last couple of years road corridors for secure land transportation have been developed. Therefore it has become more viable to enter the African market via a regional hub and have further distribution inland via road transportation.

Imperial and Bolloré are examples of logistics service providers investing heavily in their own infrastructure, such as ports and rail networks, to gain control of the transportation chain. This enables them to offer active temperature-controlled transportation services within and between some of Africa’s main countries and cities. This provides opportunities for the pharma industry to “open” regional distribution centers and replenish via sea instead of airfreight. In this way, 4 out of 5 euros on average can be saved just by switching the transportation mode.

Some countries and companies are already piloting drone solutions and have started building drone hubs for further distribution of the last mile in rural areas. While in Europe drone solutions encounter various legal hurdles, such new technologies could be an interesting spin on last-mile distribution in Africa, providing a fast fix for missing road and network infrastructures.

Taking The First Steps

In the sub-Sahara region, 2016 economic development showed a negative per capita income growth rate and was therefore not too promising. This is related to the post-Ebola recovery and the low oil price. The outlook for 2017 and 2018 is more promising with an expected gross domestic product growth of 2.9% and 3.6% per annum. The major risks for GDP development in the region are the slowdown of China’s economic growth, political uncertainty in Europe, and US policy uncertainty.

However, in the mid- and long-term, Africa and especially the sub-Sahara region are very promising markets. The sooner pharma companies sharpen their footprint the better their chances to be in pole position when the race starts.

As a starting point, it is important to gain transparency on market pricing of the products for the end customer and to track the origin and extent of the price markup through the whole distribution chain. Distribution costs and routes currently in use should be evaluated and compared against alternative distribution and regional distribution center models to enter Africa from the east, west and south coasts. It is advisable to get firsthand knowledge of local markets. If the market volume is big enough or sales forecast is promising, opening a local affiliate might be the right way to achieve a positive business case in the mid-term. See you in Africa!