Shale Booms into Plastics Export Market

How Much Margin Will US Producers Leave on the Table?

-

© StudioLaMagica - Fotolia.com

© StudioLaMagica - Fotolia.com -

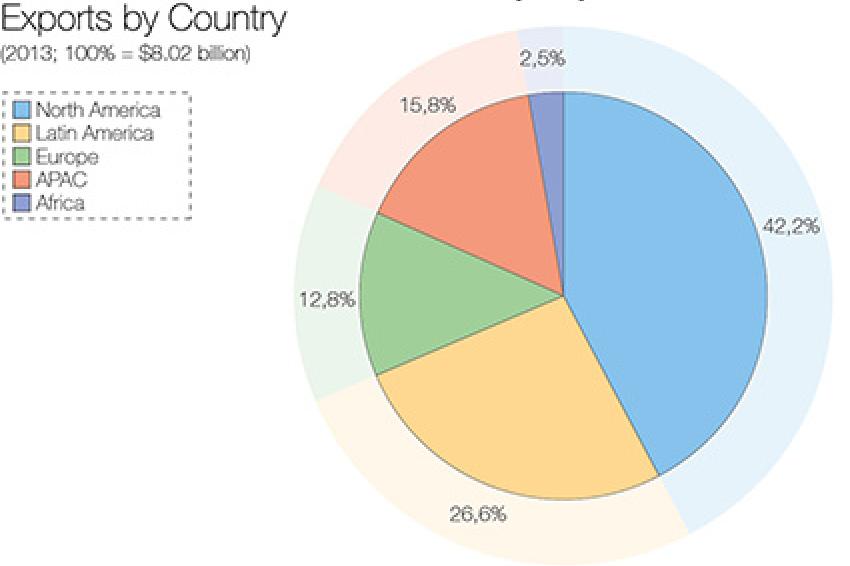

Value Share of North American Polyethylene Exports by Country (2013; 100% = $8.02 billion). Source: United States International Trade Commission

Value Share of North American Polyethylene Exports by Country (2013; 100% = $8.02 billion). Source: United States International Trade Commission -

Dr. Kai Pflug, CEO, Management Consulting - Chemicals

Dr. Kai Pflug, CEO, Management Consulting - Chemicals

The development of shale gas and the resulting low prices for natural gas in the United States have resulted in a major change in the production costs of plastics. According to the American Chemistry Council, in May 2014 a total of $113 billion of chemical industry investments related to shale gas had been announced.

According to ICIS, a provider of marketing intelligence on the global chemical industry, this includes 7.1 million tons of new polyethylene capacity that has been announced for the US through 2020, and the number is expected to rise as further derivative plants for previously announced US ethane cracker projects are revealed.

Though all these projects may not be executed, the added capacity is likely to be much higher than the estimated US polyethylene demand growth rate of an annual 3% in this period.

Expanding Exports

Polyethylene producers therefore will have to rely on exports to make their investments viable. The US is already an exporter of PE - in 2012, about 20% of production (or 3.6 million metric tons, according to American Chemistry Council data) was exported. Currently the largest export destination is the North American Free Trade Agreement (NAFTA) region followed by Latin America (see figure). Together, these two "near" markets account for almost 70% of US exports of PE.

However, demand for US exports within NAFTA exports is expected to contract significantly. Nova is constructing a 450 kt/a linear low-density polyethylene (LLDPE) plant at Joffre, Alberta, which is due to start up in 2015, and is debottlenecking existing LLDPE and high-density polyethylene (HDPE) plants at Moore, Ontario. In addition, the Braskem/Grupo Indesa Ethylene XXI project, which is due to start up at Veracruz, Mexico, in 2015, will include 750 kt/a of HDPE capacity and 300 kt/a of LDPE capacity.

Europe is another option for US polyethylene exports, but not a very promising one because of local competitors (though with a cost disadvantage) and very limited growth prospects. This leaves South America, Asia, and to some extent Africa, as the core target markets for increased PE exports from the US It is expected that by 2020, US polyethylene producers will need to export between 6 million and 7 million tons of polyethylene to South America, Asia and Africa, with at least half going to Asia.

Weighing Margins And Risk

Who will manage these exports? US producers will have two basic options. They can leave the export to third parties, such as traders and distributors. This is simple and straightforward, but also has huge disadvantages. It means accepting substantial losses in margin. It also prevents US producers from fully understanding the fast growing and developing markets of Asia, South America and Africa and their specific requirements. It therefore is certainly not an ideal solution, particularly if these exports keep increasing.

The other option is for US producers to manage these exports themselves - with the advantages of improved margins and better market understanding. However, currently US producers have only limited resources and capabilities to manage these exports, as markets outside NAFTA were not their particular target regions in the past. And even those of the bigger plastics producers with a substantial presence in Asia - e.g., via regional offices - frequently prefer to use US traders rather than managing the exports themselves.

This is partly due to the conservative attitude of these producers. Their core expertise is in production of plastics, not in price speculation. They are therefore highly averse to price risks. However, such risks are almost inevitable because of the long shipping times from the US to Asia. Customers will generally be willing to settle the price only upon arrival of the goods in Asia and, if forced to agree to prices prior to shipment, will demand a premium to compensate them for the price risk they are taking. Without such a premium, they prefer to delay the purchasing decision for some weeks and then buy from a regional producer with a much shorter supply chain.

If a US producer agrees to price settlement upon arrival of the cargo, any positive or negative change in plastics prices during the shipment period affects its profit. While overall these risks will even out over a longer period, they can still be quite worrying for an employee at a risk-averse plastics producer. Furthermore, the additional working capital tied up in unsold cargoes on the water between the US and Asia creates stress for the finance departments of the plastics producers.

Physical Barriers

Apart from the conservative attitude, another obstacle for managing exports is the lack of physical and administrative resources:

- Bagging: As the vast majority of domestic US plastics sales are sold in bulk rail cars, plastics producers do not have the equipment to package plastic resin in the 25-kilogram bags considered to be the standard packaging for plastics in the developing world. Producers are reluctant to invest in the capital for such equipment and the space to store the bagged resin.

- Logistics: US plastics producers are reluctant to establish the staff and contractor resources to handle logistics at both ends of the international trade, e.g., facilities to load 25 kg bags into 20- and 40-foot shipping containers as well as bonded warehouses in destination countries to provide local stock for customers.

- Credit: Traders are experienced in handling the financial aspects of international trade, which can involve a wide range of payment options - for example, letters of credit, documents against payment and open account - and requires dealings not only with customers but also with banks in the US and export countries. Plastics producers mostly focusing on domestic trade would need to develop the in-house expertise to manage the financial aspects of international trade and judgment to make decisions that balance risk and cost.

- Documentation: Documentation of international trade is much more complex than domestic trade. It needs to satisfy the exacting requirements of not only inbound customs officials, whose requirements vary from country to country, but also the banks of both parties. This is therefore another aspect of exports that US plastics producers want to avoid if possible.

- In-Customs Handling: Similarly, plastics producers have less experience in dealing with import regulation for their goods than experienced traders. Again, they are reluctant to develop such knowledge in-house, which is vital if a producer is to offer short lead-time supply to export customers. This would require setting up bonded warehouses or foreign-invested commercial enterprises, which enable foreign companies to sell products in the domestic China market in local currency.

Risks of Third-Party Model

Of course, many other US chemical companies do sell their products directly to overseas customers via their own channels. A large number of chemicals require technical service, which on a sufficient level can only be provided by the producers themselves. However, plastics producers primarily export commodity grades. These grades generally are exchangeable, and customers do not expect any particular service. Therefore these chemicals are in principle highly suitable for sale via third parties such as traders.

This also points to another limitation of the current, third-party driven export model apart from the loss in margin. Once plastics producers want to sell higher-value grades to export markets, the exclusive arrangement via traders becomes a severe obstacle. Clients of such materials require technical service from local staff. As their perceived risk in using such materials is also much higher than for commodity grades, they also expect direct contact with the producers as an indication of producer commitment to their products.

Conclusion

Overall, US plastics producers will therefore be well advised to expand their capabilities in directly managing their global plastics exports in the face of increasing dependency on such exports. This will bring both immediate benefits with regard to improved margins and longer-term advantages for the sale of higher-value grades. In our opinion, these points more than compensate for the extra resources established, and for the slightly higher risk.

Contact

Managm. Consult. Chemicals

RM1302, 13/F CRE Bldg.

Wanchai, Hong Kong

China

+86 1368 1873992