BDO: The Pacemaker Stumbles

China Sets the Pace in the Global 1,4-Butanediol Market, but Who Will Win the Race for Customers and Markets?

-

BDO capacities by regions (in tons per year)

BDO capacities by regions (in tons per year) -

Novamont will use Genomatica’s process to produce 30,000 tons of renewable BDO per year in Adria, Italy, up from an original plan for 18,000 tons. © Novamont

Novamont will use Genomatica’s process to produce 30,000 tons of renewable BDO per year in Adria, Italy, up from an original plan for 18,000 tons. © Novamont -

Ashland’s 1,4-butanediol plant in Lima, Ohio, USA has an annual capacity of 65,000 metric tons of BDO. © Ashland

Ashland’s 1,4-butanediol plant in Lima, Ohio, USA has an annual capacity of 65,000 metric tons of BDO. © Ashland -

BioAmber can transform its bio-based succinic acid produced in a new plant in Sarnia, Ontario, Canada, into 1,4-Butanediol (BDO) and Tetrahydrofuran (THF) in a single catalytic step. © BioAmber

BioAmber can transform its bio-based succinic acid produced in a new plant in Sarnia, Ontario, Canada, into 1,4-Butanediol (BDO) and Tetrahydrofuran (THF) in a single catalytic step. © BioAmber -

Diversity of BDO production technologies

Diversity of BDO production technologies -

-

- -

BASF is planning to increase 1,4-butanediol (BDO) chemical intermediate production at its Geismar manufacturing facility in Louisiana, USA. © BASF

BASF is planning to increase 1,4-butanediol (BDO) chemical intermediate production at its Geismar manufacturing facility in Louisiana, USA. © BASF

1,4-Butanediol (BDO) is an important chemical intermediate product and raw material for plastics, solvents and synthetic fibers. The alcohol’s production capacities have been expanded further in recent years, triggered by the growth of its diverse applications. BDO has boomed almost explosively in China: In the past 12 months more capacity has been built in China than in the entire Western world in the last 70 years. A capacity of 1.7 million tons per year in China today compares with local demand of just 550,000 tons.

According to the “China Chemical Reporter,” this gap probably will broaden by 2018, when a total installed capacity of 2.8 million tons per year will exceed local consumption in China — about 700,000 tons per year — four-fold. This trend already has triggered a dramatic reduction in the price of BDO. During the last 12 months the price has fallen almost 50% in China. This price drop has affected non-Asian BDO producers in particular, who can barely export any BDO because of overcapacity in Asia, as supply by local manufacturers has continually exceeded demand in recent years.

Series Of Shutdowns

Reports published at regular intervals in May by industry journal ICIS Chemical News in Singapore have therefore attracted a lot of attention: Four important BDO production sites were closed down in China in a period of just two weeks. The chain of events was started by Tianye, in the northwestern province of Xinjiang, which announced the shutdown of three facilities, with total installed capacity of 150,000 tons per year. The official justification for this measure is the laying of a supply pipeline for production with acetylene, which represents an obstacle to the construction of a railway line.

On the same day Kaixiang Chemical, based in the central Henan province, reported the closure of two production units, each making 45,000 tons of BDO per year, for scheduled maintenance. Just a few hours later came news of the next shutdown: Ningxia Energy Chemical, a joint venture between Sinopec Great Wall Energy Chemical and Guodian Younglight Energy Chemical in the northwest province of Ningxia, unexpectedly closed down its plant, which produced 100,000 tons of BDO each year, due to technical problems, without giving details of when the facility is to start up again. Finally, this was followed by Markor Chemical, also in Xinjiang province, shutting down two units with a total production capacity of 160,000 tons BDO per year for maintenance in the beginning of June.

These measures mean that a quarter of existing Chinese capacities are going offline. As a result, manufacturers outside of Asia hope for an easing of pressure from China, both in terms of the available quantities as well as prices, which, according to data from ICIS in China, had fallen by 12% from the start of 2015 through May. BDO prices are particularly influenced by the relationship between supply and demand. The strong supply situation and the price difference between Asia and the other regions are the main reasons for prices — which are set quarterly — having dropped for the fourth consecutive time in Europe.

Fragile Price Trend

Sharply declining prices for crude oil since mid-2014 and lower costs of propylene and acetylene are also driving this trend. ICIS estimated that BDO prices in Europe finally settled at between €1,730 and €1,760 per ton in the third quarter of 2015. Since Chinese producers removed significant capacity from the market, prices should rise again in China, at least in the short term, and in turn this should relieve the pressure on European BDO prices.

Against this background of a fragile price trend, plans for further development might falter. According to a report from the world’s largest market research company, Research and Markets, global BDO capacity was at around 3.35 million tons at the end of September 2014, roughly half of which originated from China. A further 38.5% of global supply is accounted for by BASF from Ludwigshafen, Germany; Dairen Chemical Corp. (DCC) based in Taipei, Taiwan; and LyondellBasell from Houston, Texas.

Regional Leaders

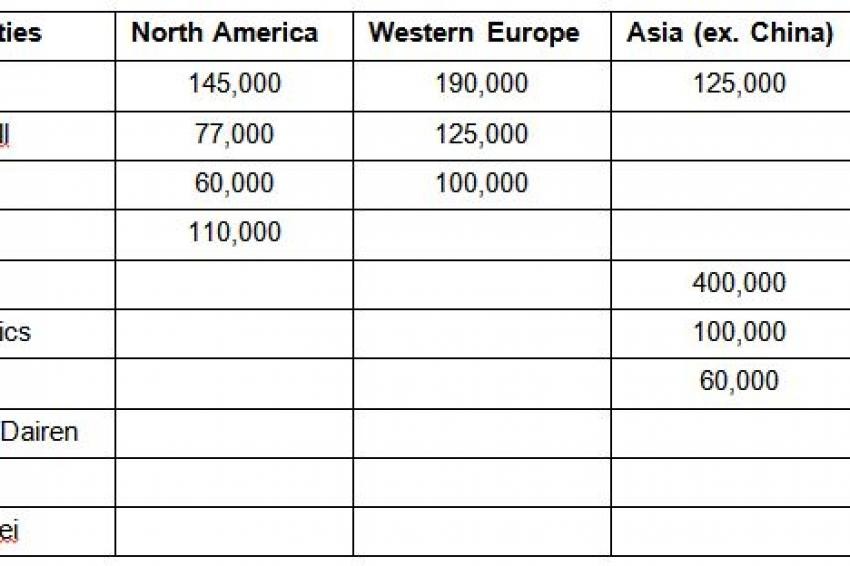

The largest manufacturer in North America is BASF, which makes 145,000 tons per year at its facility in Geismar, Louisiana; followed by Invista with 110,000 tons per year in La Porte, Texas; LyondellBasell, with 77,000 tons per year in Channelview, Texas; and Ashland at 60,000 tons per year in Lima, Ohio. At the beginning of 2015 BASF announced that the company would extend its production capacity at the Geismar site by 10%. As a result, BASF will be capable of producing 670,000 tons of BDO worldwide per year in the future, equivalent to roughly 20% of the currently available global quantity.

Once again the most important players in Western Europe are BASF, with 190,000 tons per year in Ludwigshafen, Germany; LyondellBasell in Botlek, Netherlands, 125,000 tons per year; and Ashland, with 100,000 tons per year in Marl Chemical Park, Germany.

Dairen Chemical Corporation (Taiwan) is the dominant player in Asia (excluding China), with approx. 400,000 tons per year, followed by BASF with 125,000 tons per year, Mitsubishi Chemical in Japan, with 60,000 tons per year, and Nan Ya Plastics from Taiwan, with approximately 100,000 tons per year.

Five other manufacturers have additional capacities in Korea, Taiwan and Japan of between 25,000 and 50,000 tons per year. For example, market leader BASF operates another facility in Japan, at an estimated capacity of 25,000 tons per year. Around 20 different manufacturers, among them also BASF, are operating in China, with facilities producing between 10,000 and 120,000 tons per year. Markor Chemicals, one of the largest BDO producers in China, has so far built two owned facilities in Xinjiang province with a total capacity of 160,000 tons a year. In addition, the company has agreed to a joint venture with BASF, which should start operating another facility for 100,000 tons per year at the Korla site.

With this, BASF is the only manufacturer to operate in all four submarkets. According to Research and Markets (September 2014), Markor Chem, Shanxi Sanwei and Chang Chun/Dairen Chemical are the three largest manufacturers in China, with capacities of 160,000, 150,000 and roughly 200,000 tons a year respectively. Markor, through its joint venture with BASF, will continue to become more important.

High Refinement Rates

In recent times, around 2 million tons of BDO have been produced in the entire BDO market, but only 20% of it is traded in the freely accessible market, while the other four-fifths are processed internally to derivatives by the manufacturers. As an intermediate product, BDO is an important raw material for the synthesis of other substances, in particular of tetrahydrofuran (THF), polybutylene terephthalate (PBT) and gamma-butyrolactone (GBL).

The direct application of the diol in plastics results in a variety of substance classes, such as esters, polyesters, carbamates and urethanes. Overall, they constitute around 39% of the total quantity. The most important area of operation (around 20%) is the production of polybutylene terephthalate (PBT), a thermoplastic polyester used in electrical engineering, vehicle construction and household products. An additional 13% is employed in the manufacture of polyurethanes, which are used as foams, molding compounds, casting resins, fibers, paints and adhesives. So far only low quantities have gone into the production of polybutyrate (PBAT), which is primarily used as a fully biodegradable alternative to low-density polyethylene.

Textile Trends

Overall, THF and THF-derivative applications account for almost 50% of the global BDO market. The largest sector here involves spandex and elastane fibers, which play an important role in a large number of textiles, such as in functional clothing, stretch jeans, underwear and stockings. In combination with polyamide, cotton or polyester fibers, highly elastic fibers are processed into materials. Spandex fibers, consisting of 80% polytetramethylene ether glycol (PTMEG or PolyTHF), can be stretched to between 500% and 700% of their original length and durably retain their shape. Growth rates for spandex, at between 9% and 10%, are much higher than growth rates for textiles — the trend toward comfortable clothing with high wearing comfort is driving demand in this area.

“Spandex fiber is increasingly becoming an integral part of modern textiles,” an industry expert recently said.

Solvent Share

Around 15% of BDO is used in other THF areas of operation, in particular solvents for a variety of plastics (PVC, polystyrene, polyurethane, cellulose nitrate), adhesives and paints. THF is used as an intermediate product for polyamide, polyester and polyurethane manufacturing. THF usage in pharmacies and life sciences represents a smaller share (5%).

The remaining 13% of global BDO demand is used in the production of GBL, a lactone for gamma-hydroxybutyrate, primarily employed as an industrial solvent and raw material for the manufacture of essential pharmaceuticals and chemicals. A part of GBL is converted into N-methyl-2-pyrrolidone (NMP), which is often used as a solvent for polymers, such as acrylates, epoxides, polyurethanes, polyvinyl chloride, polyimides and polyamides, due to its thermal stability and high polarity. GBL is also used in paint stripping and manufacturing of polyurethane foam.

Most BDO producers “refine” the diol themselves and manufacture derivatives such as GBL, THF, PTMEG, PBT or NMP.

“Only around 20% of the globally produced quantity of BDO is available on open sale,” an industry expert confirmed.

Capacity And Demand

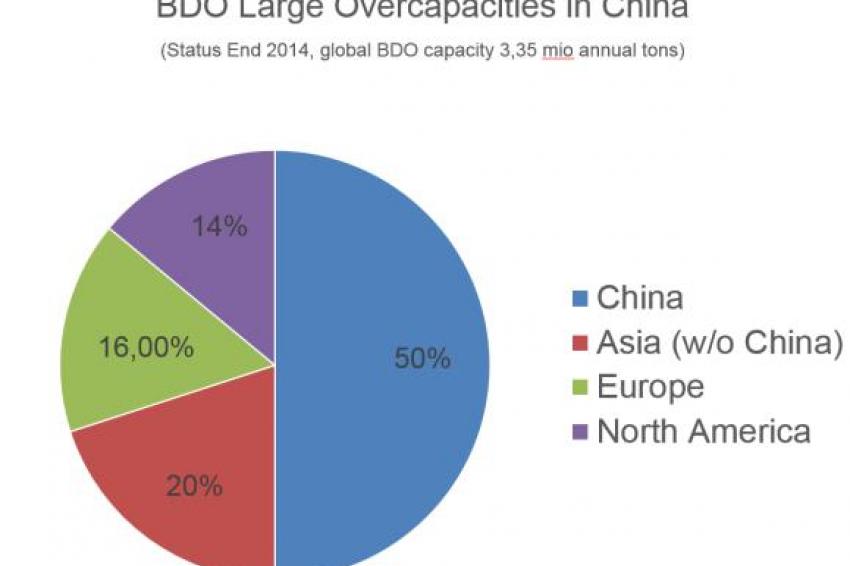

Regional capacity and demand are quite different in the four large manufacturing and buying markets of North America, Europe, China and the rest of Asia. The capacity of China alone exceeds the total production capabilities of North America, Europe and the rest of Asia combined. Whereas China has built up around half of all installed capacities, the other half is spread out between North America, with around 27%, Europe with 32% and Asia (excluding China) with 41% — the only region where demand exceeds capacity — while Europe has low, and North America and China significant overcapacities.

Based on current forecasts for 2020, overcapacities are set to rise even more sharply than demand as a result of additional construction in North America, whereas demand should slightly outstrip the available capacities in Europe by this date. In China, on the other hand, the growth in capacity is still rising more sharply than demand, while capacity in the rest of Asia is only growing slightly and demand will increase much more sharply. In global terms, in the event of increasing capacities and rising demand, the ratio between overcapacities and demand will remain roughly the same between 2015 and 2020.

Global overcapacities of over 40% already exist today. According to a forecast by ICIS and other sources, this ratio between production capacity and demand will remain virtually unchanged in 2020. Research and Markets even reports (“Global and Chinese BDO Industry Report,” 2014-2017) that new BDO capacities of 1.4 million tons per year are planned in China. However, some projects could be delayed or cancelled completely as a result of existing overcapacities and sluggish demand. This would bring about a significant slowdown in the extension of BDO capacities.

Diversity of BDO Production Technologies

Various technologies have been established, based on different raw material sources, for the production of BDO and its derivatives. One of the most important routes for BDO originates from acetylene, which can be extracted from coal, naphtha or natural gas. In the 1920s and 1930s, Dr. Walter Reppe, who had been a researcher at BASF since 1921 and head of BASF Research after the end of World War II, laid the foundations for “acetylene chemistry,” including the production of BDO from acetylene. Propylene is another raw material, which has two alternative synthesis routes: one leading through propylene oxide and allyl alcohol to BDO, as used by LyondellBasell, one of the biggest BDO producers in Europe.

The other route leads from propylene, directly through allyl alcohol, to BDO and was first implemented on a commercial scale by Dairen Chemical Corp., Taiwan, in 1998. The first production of this type had a capacity of 30,000 tons per year, and in 2002 Dairen built another plant in Taiwan, making 100,000 tons a year.

A third raw material is butane, which is converted into maleic anhydride and subsequently BDO. This “Davy process” was first put into practice in the 1990s, and relevant production facilities have primarily been constructed in China and the Middle East. Another procedure uses butadiene as a raw material and was developed by Mitsubishi Chemical Industries in the late 1970s.

Viewed historically, the Reppe process is the most prevalent method in the BDO industry, with around 40% of global capacities still based on this procedure. Global chemical companies in particular, such as BASF, Ashland and DuPont, work on the basis of the Reppe method, but the process is also dominant in China because it allows the giant empire to make use of its own raw materials to produce calcium carbide, as a result of large coal deposits. In light of the various options, barriers in the “BDO world” are low and all stages along the value chain can be licensed. In addition to the process selected, access to favorable raw materials is therefore the key factor.

Raw Materials Base is a Decisive Factor

Against this background, the highest possible level of commercial access to raw materials, such as coal or natural gas, propylene, butadiene and n-butane or maleic anhydride, is just as crucial as the most extensive value chain, in which BDO only represents an intermediate stage. The “PERP Report” (March 2012) compares procedure-related BDO production costs, modeled on a facility on the US Gulf Coast, with capacity of 60,000 tons a year. Costs per ton of BDO vary between less than $2,000 and over $3,000 US, whereby various factors are considered, for example, the variable costs of raw materials and energy, fixed costs, such as labor and maintenance costs, depreciation and return on capital employed (ROCE).

According to this summary, Davy process technology based on maleic anhydride, with an output of 80% BDO and 20% THF, has the lowest production costs, at around $1,900. At the other end of the scale is the Mitsubishi process based on butadiene, with costs of over $3,000, similar to the cost of the LyondellBasell procedure using the propylene oxide route. Nexant, which publishes the “PERP Report,” itemizes the statement of costs with a forecast for regional competitiveness in 2017, in which regional differences — in raw materials, for example — carry greater weight. The spread ranges from $2,100 to $4,500 per ton of BDO. The influence of raw material prices becomes apparent in the Reppe process, which is much more favorable in China (based on coal) at $2,100, than in the United States (based on natural gas) at $2,600, and Western Europe (based on naphtha) at $3,300.

Since 2012, commodity prices have, however, changed considerably. While the price of coal and naphtha has more than halved, the price of natural gas is now lagging on a similar level as in 2012, but with an interim high at the turn of 2013 and 2014, when it was more than twice as high as today.

In addition, experts argue that the approach of the PERP reports is too generalized. Many other factors play an important role in the calculation of real costs. Starting with the size of the facility and ending with the specific integration of facilities at a location. One important point, for example, is the extent to which a facility with preliminary, secondary and derived products can be integrated with other facilities. This point is applicable, for example, to the use of acetylene waste gas, which is generated in the course of acetylene production and can be used to extract carbon monoxide (e.g., for isocyanate synthesis) and hydrogen for hydrogenations.

The process creates much higher added value than using acetylene waste gas as fuel only. BASF, which summarizes such integration under the term “composite,” benefits from the continuous forward and backward integration of its facilities. Against this background, experts assume that the fully integrated Reppe process is one of the most favorable options under such conditions, based on natural gas.

Long-Term Option of Renewable Raw Materials

One option for the future involves the use of renewable raw materials as a new basis for BDO production. Nexant Chemsystems sees potential for commercialization of this trend in the next five years. Initial technical approaches are already being examined by various manufacturers. In March 2011, Myriant and Davy Process Technology entered into a partnership to produce BDO based on bio-succinic acid. Since June 2011, Genomatica (San Diego, California) has made BDO based on dextrose, which is handled in a fermentation process, at a demonstration facility in Decatur, Illinois, belonging to and operated by food manufacturer Tate & Lyle. BASF and Genomatica entered into a license agreement in May 2013, which makes it possible for BASF to use the Californians’ patented fermentation procedure. The license agreement allows BASF to build a world-scale production facility for BDO from renewable raw materials. BASF is already providing customers with kilotons of BDO made from renewable raw materials. BioAmber (Minneapolis, Minnesota), an industrial biotechnology company, announced in May that it had acquired a license from Johnson Matthey Davy Technologies (London). This license allows BioAmber to construct a facility with a capacity of 100,000 tons per year for production of BDO (70,000 tons) and THF (30,000 tons), using bio-succinic acid as the raw material. The facility is set to start operating in 2018.

“The agreement with BioAmber is the first license we have awarded to North America and the first facility which will use bio-succinic acid,” said Mark Sutton of JM Davy.

In the long term at least, the investigation and practical testing of alternative raw material sources definitely constitutes a sensible plan. However, procedures based on renewable raw materials are still clearly more cost-intensive today. In May the EU Commission’s Energy Directorate submitted an up-to-date report titled “From the sugar platform to biofuels and biochemical.” The study demonstrates that at the present time there is only a very limited market for premium products, which score sustainability and for which customers are willing to pay a surcharge. Bio-BDO, with a current premium market of just 3,000 tons a year, about 1% of the total market, is no exception here.

In view of this assessment, which is shared by many experts, BioAmber’s plans appear all the more ambitious. On the one hand the North American market is already oversupplied, while on the other hand the starting point for production, destined for export to Europe, for example, and based on maize, is not exactly favorable. A location in the Midwest, the source of corn in the US, involves long-distance transport routes for the product, while a port location would be far away from the raw materials — both options imply additional costs on what is already a competitive market.

Exports to Europe face another obstacle: in contrast to the US, there might well be some discussion in Europe about whether raw materials, which can also be used in food production, should go into the production of chemical products. In the long term, so-called second-generation sugars, based on raw materials that are not suitable for food production, offer opportunities.

The Price Question

The price of BDO is set in China. Prices in other regions are based on the Chinese price for BDO, plus export costs (logistical costs, taxes and customs duties) in the region. How China deals with its significant overcapacities will be a key question in the future. Is the shutdown of significant installed capacities just an accident or a pointer? Planned new facilities are not only being delayed in the most highly populated country on earth because of the fragility of the market. Two criteria will primarily affect investment decisions: the availability of affordable raw materials on the one hand and receptive buying markets on the other. Export barriers are relatively high for Chinese manufacturers — export taxes are 8% on BDO and 12% on PTMEG.

Moreover, sites that rely on coal as a raw material are mostly far away from the coast, implying additional transport costs for exports. As a raw material coal is an additional “unknown factor” in the further development of BDO. Air and climate pollution caused by the exploitation of coal deposits is increasingly becoming a topic of discussion in China and carbon dioxide emissions might be restricted by the state in the future. Other raw materials, such as natural gas or crude oil, are not affordable in China.

No matter how the situation develops in China, the pacemaker in the BDO sector, one thing remains certain: Manufacturers with highly integrated production and a very long value chain could well be one step ahead in the long term.

Author:

Klaus Jopp,

freelance scientific journalist,

Hamburg, Germany

Email: klaus.jopp@wiwitech.de