Camelot’s Pharma Management Radar

Biosimilars Revolution and its Limits

-

Fig. 1

Fig. 1 -

Michael Jarosch, Head of Industry Segment Pharmaceuticals & Life Sciences at Camelot Management Consultants: “While the pharmaceutical industry is still suffering from the Eurozone crisis in various regions, some of the established markets outside Europe seem to be coming back: Demand expectations for North America - which may also be positively affected by re-elected President Obama’s healthcare reform - and for Japan are showing some considerable growth.”

Michael Jarosch, Head of Industry Segment Pharmaceuticals & Life Sciences at Camelot Management Consultants: “While the pharmaceutical industry is still suffering from the Eurozone crisis in various regions, some of the established markets outside Europe seem to be coming back: Demand expectations for North America - which may also be positively affected by re-elected President Obama’s healthcare reform - and for Japan are showing some considerable growth.” -

Dr. Axel Sinner, Head of Competence Center Pharmaceuticals & Life Sciences Commercial at Camelot Management Consultants: “It remains interesting to see how prescribers will handle the substitution of Originator-Biologicals and how payer organizations will play the price game in the competitive area between Originator-Biologicals and their Biosimilars, as well as in-between the Biosimilars segment itself. At any rate these two developments will considerably limit the value of the multi-billion USD market of Biologicals coming off-patent in the near future.”

Dr. Axel Sinner, Head of Competence Center Pharmaceuticals & Life Sciences Commercial at Camelot Management Consultants: “It remains interesting to see how prescribers will handle the substitution of Originator-Biologicals and how payer organizations will play the price game in the competitive area between Originator-Biologicals and their Biosimilars, as well as in-between the Biosimilars segment itself. At any rate these two developments will considerably limit the value of the multi-billion USD market of Biologicals coming off-patent in the near future.” -

Fig. 6

Fig. 6 -

Fig. 5

Fig. 5 -

Fig. 4

Fig. 4 -

Fig. 3

Fig. 3 -

Fig. 2

Fig. 2

End Of Patent Protection - The global pharmaceutical industry is steering toward the patent cliff: Some of the biggest blockbuster drugs in history - Lipitor, Plavix and Viagra - lost patent protection in the last two years, and many others are soon to follow. While the patent cliff has passed its peak in the small molecule segment, this especially applies to biologicals. Nine of the 10 top-selling biologicals will lose patent protection by 2020 either in Europe or the U.S.

For the comparably new segment of biosimilars, this means a potential market volume of more than $62 billion. Nevertheless, the market actors do not expect the upswing of biosimilars to fundamentally change the entire pharmaceutical industry. This is, among other things, due to the fact that biosimilars are not expected to be priced as high as the patent-protected originals. In addition, the necessary R&D - and the investments and risks combined with it - pose a difficult hurdle for many companies.

This is the picture that emerges from the second Camelot Management Consultants Pharma Management Radar survey, a biannual survey that serves to examine the general climate in the pharmaceutical industry and take an in-depth look at a varying current management topic. In a four-week period in August and September 2013, the Pharma Management Radar expert panel, consisting of more than 80 executives from globally active pharmaceutical companies based in 16 countries, was interviewed to analyze the influence of biosimilars.

After the surprisingly positive estimation of the current business climate registered in the first Management Radar survey published half a year ago, the experts generally remain satisfied. This particularly applies to the generics executives, all of whom rate the business climate as "mostly good."

Considering the business climate in the next 12 months, the overall estimation has brightened up slightly, especially among innovators who had been considerably more pessimistic at the beginning of this year. It seems as if at least some of the innovators had found a way to cope with the "additional benefit/outcome topic" and thus have developed a slightly more positive assessment in the course of the year.

The stabilization of the generics' positive assessment - more than 80% expect the climate to remain positive or even improve - might, among other factors, also be explained with the potential impact expected from the upcoming biosimilars business.

While the pharmaceutical industry is still suffering from the Eurozone crisis in various regions, some of the established markets outside Europe seem to be coming back: Demand expectations for Japan and North America - which may also be positively affected by re-elected President Obama's health-care reform - are showing some considerable growth.

A striking difference between generics' and innovators' demand expectations can be found in emerging regions such as China and Africa where the generics segments are much less optimistic. This clearly has to do with the fact that in these regions innovative products are available mainly for wealthy self-pay patients who can afford even higher prices than are paid by the health-care systems in developed countries.

However, the poor majorities of these emerging regions can't afford more than a minimum price, thus making the situation rather unattractive for the producers of generics compared to that in the established markets.

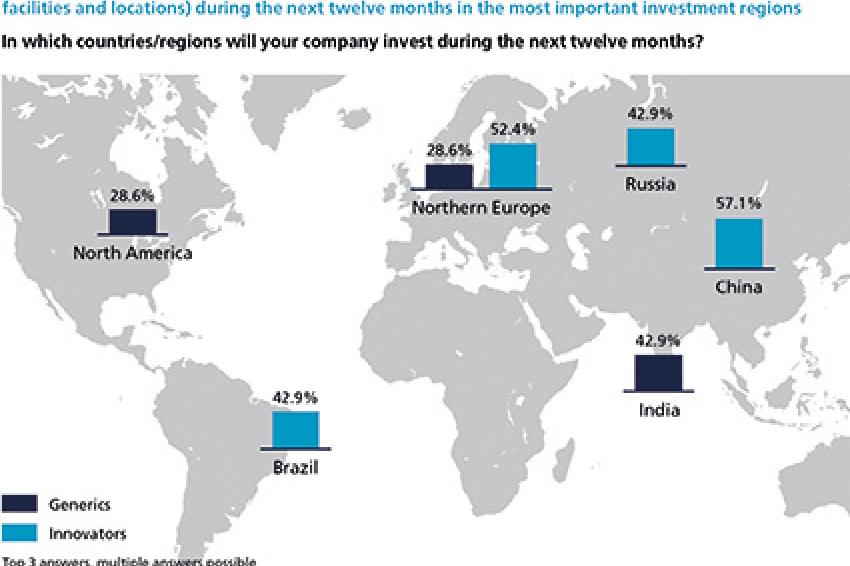

When it comes to regional investment plans for the next 12 months, the executives' answers differ considerably from their demand expectations. Eastern Europe, Russia and North America have lost some of their investment attractiveness. The top destinations for future investment are now China, Northern Europe and Brazil, when taking generics and innovators together. Looking at the two segments separately, India as a traditionally strong biotech environment is the most important investment region for generics, whereas innovators prefer China and Northern Europe. It shows that there is a slight shift back toward the established markets. The BRIC markets seem to have lost a bit of their former growth potential and attractiveness.

Asked for the most important industry trends in the pharmaceutical industry, two-thirds of the generics executives name the influence of biosimilars. Given that the biosimilars business requires far more R&D than the traditional generics business, it is logical that the R&D aspect is seen as an important trend by as many generics as innovators.

This trend is going hand-in-hand with the development of alternative business models, which also plays a major role for generics. The latter are driven by pricing pressure that makes vendors constantly look for new marketing and distribution methods in order to stabilize their business.

It may be surprising that innovators consider product innovation through research collaboration as the most relevant trend and thus as more important than fostering genuine product innovation through their own R&D. Raising doubt on their R&D productivity, they seem to be looking for a more efficient approach.

Biosimilars' Limited Effect

Although biosimilars are considered one of the most important industry trends, large parts of the industry do not feel affected. Biologicals play no big role for nearly three-fourths of generics and even half of the innovators. The figures are quite similar when it comes to the future development of biosimilars within the companies' product portfolios.

This reflects the mature phase of the decision-making process: Generics that are engaged in the biologicals/biosimilars business today will tend to keep up or even increase these activities. Innovators that are not yet in the biologicals business will most probably not enter the biosimilars market, either.

At the same time, some biologicals producers will stay away from biosimilars completely. The reason for this may be that some of the big biologicals innovators do not want to get in touch with biosimilars for image reasons - or just prefer to fully concentrate strategically on creating innovative and most profitable patent-protected drugs.

Generics and innovators more or less agree that biosimilars will have neither dramatic effects on shifts in therapeutic treatments nor on their respective product portfolios. When asked about the biggest limits that might affect the success of biosimilars, both generics and innovators name "high R&D and regulatory approval cost" as the top problem.

It is not too surprising, however, that this hurdle is considered much more challenging by generics as they are not as used to the more complicated development and approval processes that biosimilars require.

Moreover, the survey results show that the euphoria predicting much higher market prices for biosimilars than for generic drugs has cooled off. While more than half of the generics executives still expect quite high biosimilars prices at levels around 70%, the innovators' estimations are more pessimistic: More than 40% expect biosimilars prices to drop to only 15% of the prices of the originator or less.

All in all the market seems to be divided as far as the expectation of the influence of biosimilars is concerned: More than half of the companies don't feel affected at all, be it directly through their own activities in the biosimilars segment, or be it indirectly through the effect on their product portfolio.

Half of the panel members expect the prices of biosimilars to decline rapidly after launch compared with the patent-protected originator prices. Around half of those interviewed also expect the price levels between the biosimilars segment of the same originator to decline massively. It remains interesting to see how prescribers will handle the substitution of originator-biologicals and how payer organizations will play the price game in the competitive area between originator-biologicals and their biosimilars, as well as in the biosimilars segment itself. At any rate, these two developments will considerably limit the value of the multibillion-dollar market of biologicals coming off-patent in the near future.

________________________________________

- Register to participate in the bi-annual PHARMA Management Radar: www.pharmamanagementradar.com

- Order free copies of Camelot's studies on the global pharmaceutical industry at http://www.camelot-mc.com/insights.

Contact

Camelot Management Consultants AG

Theodor-Heuss-Anlage 12

68165 Mannheim

+49 621 86298 0

+49 621 86298 250