Challenges Evolve In China

Domestic Chemical Market Changes as Country Seeks Wider Global Role

-

(c) Duncan Walkeri/Stockphoto

(c) Duncan Walkeri/Stockphoto -

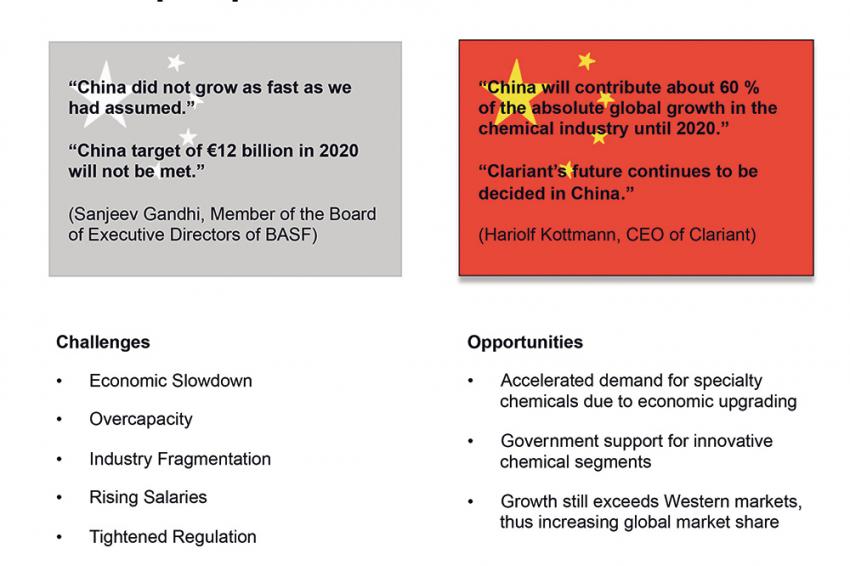

Fig. 1: Challenges and opportunities in China’s chemical market

Fig. 1: Challenges and opportunities in China’s chemical market -

Examples of environmental regulation in China

Examples of environmental regulation in China -

Dr. Kai Pflug, Management Consulting — Chemicals

Dr. Kai Pflug, Management Consulting — Chemicals

In the last 12 months, developments in China’s chemical industry have been somewhat contradictory, as illustrated by two different company statements made in September.

On the one hand, some multinationals still strongly emphasize the importance of China for global growth. Clariant’s CEO Hariolf Kottmann observed that China now accounts for 40% of the global chemical market and will contribute about 60% of the absolute global growth in the chemical industry until 2020, concluding that “Clariant’s future continues to be decided in China.”

On the other hand, companies encounter increasing difficulties to meet their targets. For example, BASF has recently confirmed that its earlier target of achieving €12 billion in sales in China by 2020 will not be met. “China did not grow as fast as we had assumed,” said Sanjeev Gandhi, BASF board member.

And Indian financial analysts are quite bullish about the prospects for India’s chemical companies, giving the rationale that “our analysis of leading Chinese (chemical) manufacturers indicates increasing cost pressure in China” (Emkay). Indeed, China’s chemical industry faces numerous challenges, which will be discussed below.

Economic Slowdown

While official figures still indicate a current gross domestic product growth of 6.7%, it needs to be kept in mind that by now services account for 54% of the Chinese economy. And these services grew at a faster rate of 7.5% in the first half of 2016, leaving a growth rate of only 5.8% for the non-service sectors of the economy (which are probably a better proxy for the chemical industry than overall GDP). Furthermore, forecasts for the next few years — depending on the source — predict a further slowdown. For example, the Economist Intelligence Unit forecasts GDP growth of only 4.3% for 2020, though admittedly this is among the most pessimistic forecasts published.

Overcapacity

While coal and steel are the most prominent examples of overcapacity in China, many commodity chemicals are also affected. This is not surprising given the huge investments that poured into the industry in the last decade. The European Chemical Industry Council (CEFIC) states that China capital investment in chemicals increased from €14.4 billion in 2005 to €95.6 billion in 2015 — a huge figure given that in 2015 chemical investment in Europe was only €20.7 billion while the US figure was €32.5 billion.

As a consequence of the capacity buildup and the economic slowdown, utilization rates are now quite low for many commodity chemicals. For example, BASF recently stated that Asian capacity utilization rates in acrylic acid and toluene diisocyanate average 60%, those of butanediol are at 65%, and caprolactam and methylene di-para-phenylene isocyanate (MDI) are each at 70%. And these rates are already higher than for even more commoditized products such as methanol, for which domestic capacity utilization is not much above 50%.

As a consequence, overcapacity is given substantial attention in the parts of the current 13th Five-Year Plan that relate to chemicals. In particular, the plan describes the reduction of overcapacity via elimination of plants exceeding energy or emissions standards, the phasing out of capacity with below-average profitability, and the upgrading of portfolio toward higher-end and differentiated products. All these measures may incur additional costs at chemical companies, at least initially.

Industry Fragmentation

One of the drivers of overcapacity is the high degree of fragmentation for many chemical markets. For example, China has about 60 producers of polypropylene, 270 producers of carbon dioxide and 255 producers of calcium carbide. For methanol, the biggest 45 producers account for only 58% of total domestic capacity. This fragmentation depresses profitability and is an additional driver of overcapacity, as Chinese companies prefer expanding their capacity to gain economies of scale instead of merging with competitors.

Rising Salaries

Average Chinese monthly salaries approximately tripled between 2006 and 2015, a much faster increase than in Southeast Asian countries that may compete with China as investment locations. While it is true that labor cost matters somewhat less in chemicals than in many other industries, there is a strong indirect effect. Once labor-intensive industries such as textile lose competitiveness in China, this may also result in a loss of markets for the relevant chemicals (e.g., textile additives, dyes). The shift of the textile industry away from China has already started. For example, in December 2015 it was reported that major clothing producer TAL was to close a factory in Dongguan because of rising wages and had already begun transferring pants orders to its factory in Malaysia. And China’s output volume of dyed/printed cloth in larger enterprises dropped by 5.1% in 2015 compared with 2014.

Environmental Protection

In the past two years, China has been actively tightening its environmental regulation, both by enacting stricter laws and by implementing them more strictly. In particular, implementation got a boost from the Tianjin explosions (which were mainly caused by disregard of existing regulation) and the anti-corruption campaign of the government (which makes it far more dangerous for local government officials to ignore violations of regulations).

There are examples from individual sectors (e.g., certain types of dyes) for which this tighter regulation has led to factory closures and a shift of production to India. The 13th Five-Year Plan also strongly emphasizes control of, e.g., mercury pollution, air pollution, organic waste, VOC and hazardous waste disposal while encouraging waste gas recycling, recycling of other materials and clean production technologies.

Chemical parks are to become the mandatory future location of chemical production, requiring substantial investment from affected companies (though the government sometimes provides support). Generally, the government seems serious about improving environmental protection — for example, in September a guideline was published describing a pilot program to evaluate officials based on their performance in environmental protection.

The recently published China Position Paper of the European Chamber’s Petrochemicals, Chemicals and Refining Working Group also highlights the worries of European chemical companies related to environmental regulation. Out of six recommendations given in the paper, four are related to regulation of chemicals and the additional costs and complexity this adds to producing chemicals in China.

Any Upside?

On the positive side, the Chinese government strongly emphasizes the goal of achieving strong positions in innovative specialty chemicals segments such as engineering plastics, organosilicones, fluoroorganics and materials used in water treatment. As a consequence, specialty chemicals companies active in targeted segments can expect substantial support for establishing R&D and production. Therefore, the prospects for specialty chemicals in China still seem fairly bright, particularly in the more innovative segments, though some mature segments such as textile dyes or leather chemicals may indeed suffer. After all, specialty chemicals are strongly aligned with China’s overriding goal of moving from the world’s workshop to a key center of global innovation.

For commodities, the perspective is a bit more negative, though selected areas may still be promising, including p-xylene, polycarbonate and polypropylene. The differing prospects of commodities and specialties are also reflected in BASF’s announcement to shift emphasis in Asia “from commodity chemicals in the oversupplied markets to focus on specialties catering for industries that include transportation, consumer products, electronics, construction, packaging, and agriculture.”

In conclusion, while a growth rate of 5%-7% may seem low using China’s recent past as a benchmark, it is still very high compared with the growth rates in Western markets. As a consequence, CEFIC expects China’s global chemical market share to increase from 39.9% in 2015 to 44% in 2030 while Europe’s will drop to 12%. And even BASF expects growth in Asia to be about 2% higher than the global average (5.6% versus 3.7%). Despite the challenges described above, no global chemical player can afford to ignore China.

Contact

Managm. Consult. Chemicals

RM1302, 13/F CRE Bldg.

Wanchai, Hong Kong

China

+86 1368 1873992