Role Reversal

China Becomes Net Exporter for Growing Number of Chemicals

-

© gustavofrazao - Fotolia.com

© gustavofrazao - Fotolia.com -

Dr. Kai Pflug, Management Consulting — Chemicals

Dr. Kai Pflug, Management Consulting — Chemicals -

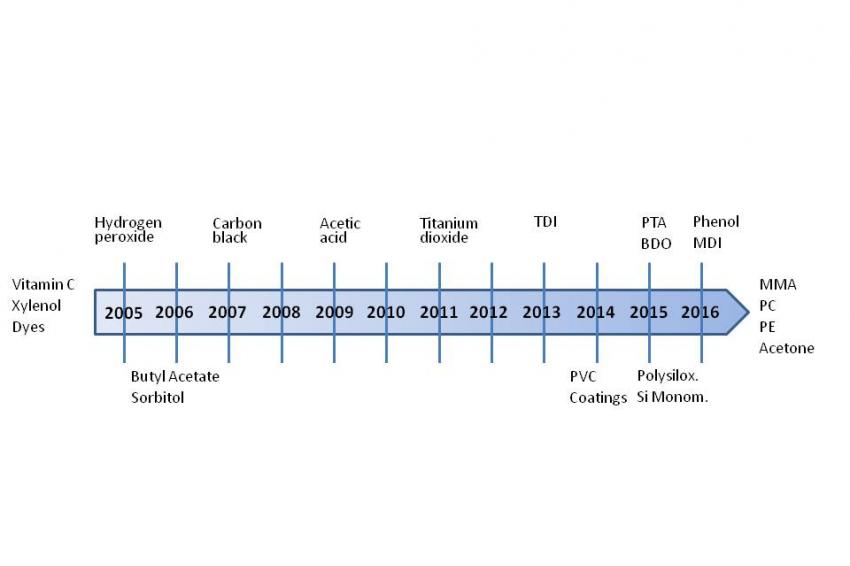

Figure 1: First year of China as net exporter of selected chemicals

Figure 1: First year of China as net exporter of selected chemicals -

Figure 2: Import and Export of PVC to/from China (Source: Tian Shengjiang, China National Chemical Economic and Technical Development Centre)

Figure 2: Import and Export of PVC to/from China (Source: Tian Shengjiang, China National Chemical Economic and Technical Development Centre)

China’s role within the global chemical industry has so far mostly been seen as an export market for global producers, not only for specialty chemicals but also for many basic organic chemicals and polymers. However, this situation has recently been reversing for some major products, thus fundamentally changing the global market situation. This paper will give some examples for these changes and discuss some of its reasons and implications.

In the early stages of China’s development, the country was a net importer for most chemicals — a natural situation given that chemical production requires a certain level of technology. However, China turned into a net exporter for some products such as vitamin C and xylenol more than 10 years ago, although this was mainly due to case-specific factors for each individual chemical (e.g., a new production route for vitamin C). Only in the last 10 years has China become a net exporter for a larger number of chemicals. Some of these are shown in figure 1. The year indicates the estimated year China became a net exporter.

Let us take a closer look at some of these chemicals, with a focus on those products for which the balance has only recently changed or is about to change.

For vitamin C, China is almost the only global producer except for one DSM plant in the UK. Consequently, China produces about 80%-90% of the global production and exports most of it. China has been in this position since about 2000, benefiting both from a domestically developed superior production technology and heavy fines imposed on Western vitamin producers accused of cartel formation.

TDI first became a net export product in 2013, with exports of about 69 kilotons (kt) versus imports of about 60 kt. This position was strengthened in 2014, with exports increasing to 74 kt while imports declined further to 37 kt. Interestingly, during this period overall domestic production grew primarily via increased capacity utilization rather than via expansion of capacity.

PVC represents perhaps the most interesting recent shift of China’s net market position as this is a high-volume polymer, which in the past was heavily exported to China (see figure 2).

While — as in the other examples mentioned in this article — it is not inevitable that China will in the future remain a net exporter of PVC, the trends regarding import and export volumes indicate that this is likely.

Also in 2014, China became a net exporter of coatings for the first time, if using a volume basis (import value was still higher than export value, reflecting the frequent lower quality of China’s exports of chemicals compared with the imported materials). Generally, coatings may be regarded as a somewhat less relevant example, as international trade accounts for only 1.2% of total output.

For PTA, it is not yet clear whether 2015 or possibly 2016 will be the year that China becomes a net exporter. In the first three quarters of 2015, China was still a net importer (554 kt of imports versus 499 kt of exports according to Chinese customs). However, the trend clearly points toward future net exports, with imports declining by 42% compared with the same period of the previous year and imports increasing by 48%.

China’s self-sufficiency rate for phenol was only 49% in 2009; however, this had already increased to 77% in 2013. As domestic phenol capacity will be strongly expanded in the next few years, market observers expect China to become a net phenol exporter in 2016, possibly closing an important export market for foreign players.

Finally, for some products such as polyethylene (PE), China’s self-sufficiency rate has not drastically changed in the last decade (from 49% in 2005 to 59% in 2014), and the current amount of material imported (about 9,100 kt in 2014) is still large compared with capacity expansions announced for the next two years (about 3,400 kt for 2015-2016). So it is unlikely China will turn into a net exporter for polyethylene soon, though one could argue that China already is a net exporter of polyethylene if finished goods made from PE were included in the statistics.

Most of the chemicals shown in figure 1, for which China is already an exporter, are chemicals for which commercial success depends on production know-how rather than on formulation or application expertise. Furthermore, these are chemicals for which China’s comparative disadvantage with regard to petrochemical raw materials either is irrelevant (e.g., vitamin C, polysiloxane) or can be compensated by alternative raw materials such as coal (e.g., PVC). In addition, the production process of many of the organic chemicals in the early part of this list is fairly straightforward and well-established, allowing new players to enter the market relatively quickly, though not always using the most up-to-date production technology. Only now China also turns into a net exporter of chemicals with higher technological entry barriers such as MDI.

Assuming that the examples above indeed demonstrate the broader and likely irreversible phenomenon of China turning more and more into an exporter of chemicals, this raises two issues. First, what are the reasons behind this development? Second, what does it imply particularly for foreign chemical companies?

Start With The Reasons

The simple explanation is that Chinese capacity of many chemicals has risen dramatically — far above the rate of local consumption. Of course, this explanation only changes the question into one about the reasons for the capacity expansions. Here, a combination of several aspects is the most convincing overall explanation, with the importance of each aspect varying depending on the specific chemical:

- In general, Chinese chemical companies have good access to investment capital. In some cases, this is due to their state ownership, but it also is the consequence of decent profits in the chemical market in the past 10 years. This gives these companies the funds to establish or expand production capacity in chemicals deemed attractive.

- When Chinese chemical companies are looking for attractive expansion areas, they frequently focus on those chemicals for which China is a net importer as an obvious starting point. Chinese companies generally base their strategic decisions primarily on market attractiveness rather than on a weighted evaluation of market attractiveness and company-internal capabilities. This leads to Chinese chemical companies frequently focusing on the same limited number of chemicals for which China is a net importer.

- An additional point is the fragmentation of many segments. For example, in PVC the market share of the biggest player is about 6%, and the total number of players is about 60. In such a fragmented market, individual players tend to assume that market prices are largely unaffected by their own expansion plans as their own share is small. They therefore feel free to expand without negative effects on their current results. While this is correct in principle, it of course no longer holds true if multiple players expand capacity at the same time.

- Chinese chemical companies generally assume that value chain integration and setup of substantial physical assets are the keys to success, rather than investment in immaterial capital (R&D) or a focus on core competencies (e.g., outsourcing of less attractive parts of the value chain). This thinking favors basic chemicals and investment in large plants.

- Needless to say, growth of many chemical markets has slowed down considerably, particularly in the last year or so. For example, domestic PVC consumption rose by an annual 10.9% from 2008 to 2013 but only by 2.7% from 2013 to 2014. Therefore any overall capacity planning of PVC producers inevitably led to the buildup of excess capacity. Chemicals with a large market in construction — such as PVC — were particularly hard hit due to the particularly abrupt economic slowdown in this area.

- For some products, Chinese producers may have cost advantages. For example, Wanhua has very advanced and large-scale MDI production while Chinese PVC producers may benefit from utilizing low-cost coal as a raw material. In addition, Chinese players may be more willing to sell at or near cash costs, particularly state-owned enterprises with a government mandate to provide employment.

- Finally, for some chemicals the entrance of foreign players also adds capacity. For example, domestic players dominated phenol production in China up to 2014. However, recently several foreign companies such as Ineos, CEPSA and Formosa have set up capacity, presumably in the somewhat late realization that there is a strategic need for local production in China.

The Second Big Question

What is the influence of China’s turn to become an exporter of more and more chemicals on the global market for chemicals, and on foreign chemical companies? Early examples are somewhat discouraging for the latter. In the global vitamin C market, China is hugely dominant, with just one foreign player (DSM) still producing. For glyphosate, the situation is similar, with Monsanto being the non-Chinese exception among the producers. However, these are likely to be the most extreme cases because of the comparatively high value of these products and the comparatively small global market (at least compared with materials such as PVC), which favor focusing the production in just a few global production sites, which then can fully benefit from economies of scale.

Nevertheless, the export of chemicals such as PVC, TDI and PTA from China will strongly influence the global market. This effect will be twofold. First, companies that have strongly depended on export of basic organic chemicals to China — in particular, companies in Korea, Taiwan, the Middle East and to some extent the US — will encounter much reduced opportunities for export to China. This will be particularly true for materials at the lower end of the quality spectrum, for which China so far served as a convenient outlet of excess production. In fact, the imposition of import duties on PVC imports from the United States, South Korea, Japan and Taiwan by China in September suggests that producers from these countries had already responded to the toughened market conditions by lowering their export prices to China.

Second, China’s exports will also compete with foreign companies in markets outside of China, depressing prices and profits and potentially leading to the longer-term exit of some foreign players, as in the vitamin C case. The anticipation of such developments is likely a key driver of global chemical companies moving more and more toward high-end, innovation and service-driven offerings rather than remaining straightforward producers of individual chemicals.

Contact

Managm. Consult. Chemicals

RM1302, 13/F CRE Bldg.

Wanchai, Hong Kong

China

+86 1368 1873992